Vertical-Specific and Packaged (VSP) Software - A Global Market Overview

- Published: Aug 2025

- Pages: 385 | Charts: 320

- Report Code: ITM083

SHARE THIS REPORT:

Global Vertical-Specific and Packaged (VSP) Software Market Trends and Outlook

The global Vertical-Specific and Packaged (VSP) Software market is expanding rapidly as organizations seek specialized solutions tailored to their operational, regulatory, and sector-specific needs. Valued at US$138 billion in 2024, the market is projected to reach US$277.4 billion by 2030, growing at a CAGR of 12.3%. As compliance pressures rise and digital transformation accelerates across industries, VSP solutions are shifting from optional investments to strategic necessities, particularly in highly regulated sectors like healthcare, finance, life sciences, and utilities.

A major growth driver is the widespread adoption of cloud-native architectures and platform business models, which enable scalable, modular deployment of sector-specific functionality. Vendors are increasingly delivering preconfigured SaaS applications with embedded compliance, analytics, and workflow automation, reducing time-to-value and ensuring regulatory alignment. At the same time, technologies like AI/ML, IoT, blockchain, and predictive analytics are fueling innovation in areas such as risk scoring, clinical support, supply chain traceability, and asset performance optimization, reshaping how industries derive value from data.

Vertical-Specific and Packaged (VSP) Software Regional Market Analysis

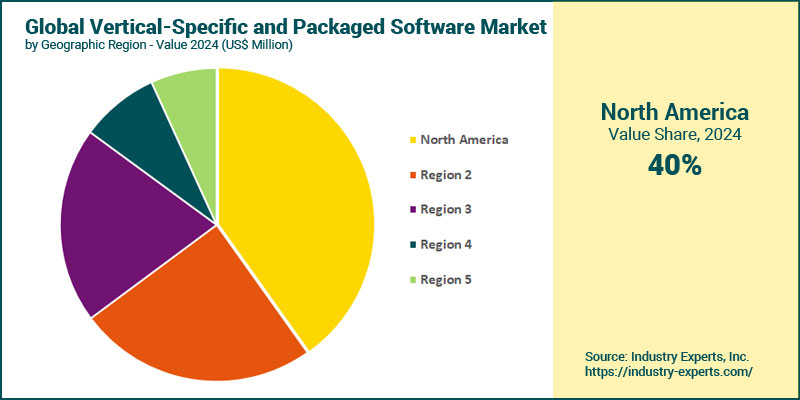

In 2024, North America was the largest regional market for vertical-specific and packaged software, accounting for 40.2% of global revenues. Its leadership is rooted in early enterprise adoption across highly regulated sectors such as healthcare, financial services, and retail, where demand for compliance-ready, domain-specific solutions remains strong. By 2030, the region is expected to reach nearly US$100 billion, driven by ongoing innovation in cloud-native architectures and sustained investment from large software vendors expanding their industry cloud portfolios. Meanwhile, Asia Pacific is poised to be the fastest-growing regional market, projected to expand at a 16.3% CAGR. Growth is being accelerated by rapid industrial digitization, increasing cloud adoption across SMEs and enterprises, and strong government support for smart infrastructure and digital transformation initiatives, particularly in China, India, and Southeast Asia.

Vertical-Specific and Packaged (VSP) Software Market Analysis by Deployment Type

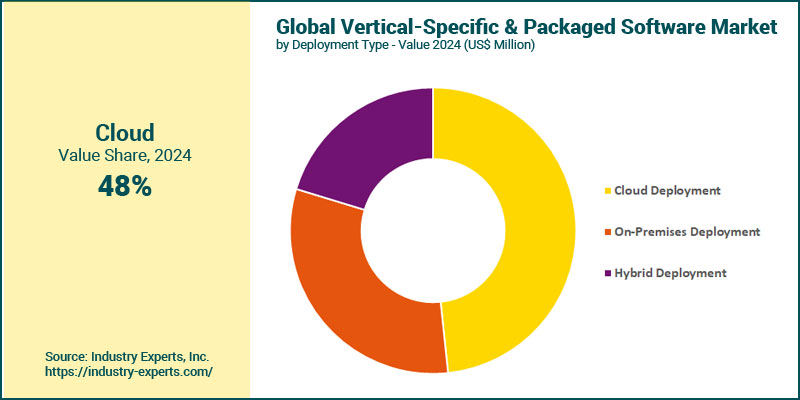

Cloud deployment was the dominant model in 2024, accounting for roughly 48.3% of the global market. This leadership is driven by sector-wide preference for SaaS delivery, allowing organizations to scale operations, simplify compliance, and ensure continuous innovation. Its traction is strongest among mid-market and regulated sectors adopting modular, cloud-native industry solutions. Hybrid deployment is expected to be the fastest-growing segment, expanding at a 14.5% CAGR. Demand is fueled by enterprises seeking flexibility, especially in industries like healthcare, manufacturing, and energy, where integration with legacy systems and data residency requirements necessitate hybrid architectures.

Vertical-Specific and Packaged (VSP) Software Market Analysis by Company Type

In 2024, large enterprises formed the largest customer segment in the VSP software market, which represented nearly 59.5% of global revenues. Their demand is driven by the need for deeply integrated, preconfigured vertical solutions that address complex compliance requirements, scalability, and global operations. However, small and medium-sized enterprises (SMEs) represent the fastest-growing segment, expanding at a 14.0% CAGR over the forecast period. This growth is being fueled by increasing adoption of cloud-based vertical SaaS platforms that offer cost-effective deployment, intuitive interfaces, and lower IT overhead, especially appealing to SMEs in sectors like manufacturing, retail, and field services.

Vertical-Specific and Packaged (VSP) Software Market Analysis Industry Sector

In 2024, healthcare was the largest Industry Sector in the VSP software market, which accounted for approximately 18.2% of total global market. The sector's dominance is driven by strong demand for compliance-focused, cloud-native platforms supporting electronic medical records (EMRs), clinical decision support, and regulatory mandates such as HIPAA and FDA 21 CFR Part 11. By 2030, healthcare-related VSP software spending is expected to rise to US$52.3 billion, underpinned by continued investments in AI-powered diagnostics, interoperability, and telemedicine. IT & telecom is projected to be the fastest-growing vertical, expanding at a 15.5% CAGR and more than doubling from 2024. Growth is being driven by rapid digitization of services, demand for customer-centric platforms, and the rollout of industry-specific solutions that streamline network operations, automate service provisioning, and enhance security and compliance for telco providers.

Vertical-Specific and Packaged (VSP) Software Market Report Scope

This global report on Vertical-Specific and Packaged (VSP) Software market analyzes the global and regional market based on Deployment Type, Company Type, and Industry Sector for the period 2021-2030 with projection from 2024 to 2030 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Historical Period: | 2021-2024 | |

| Base Year: | 2024 | |

| Forecast Period: | 2024-2030 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 20+ |

Vertical-Specific and Packaged (VSP) Software Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Vertical-Specific and Packaged (VSP) Software Market by Deployment Type

- Cloud

- On-Premise

Vertical-Specific and Packaged (VSP) Software Market by Company Type

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

Vertical-Specific and Packaged (VSP) Software Market Industry Sector

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

Vertical-Specific and Packaged (VSP) Software Market Frequently Asked Questions (FAQs)

The global Vertical-Specific and Packaged (VSP) Software market size is valued at approximately US$138 billion in 2024.

The global VSP Software market is projected to more than double by 2030, reaching US$277.4 billion at a robust CAGR of 12.3%.

North America was the largest regional market for vertical-specific and packaged software, accounting for 40.2% of global revenues.

Asia Pacific is poised to be the fastest-growing regional VSP software market, projected to expand at a 16.3% CAGR.

Large enterprises formed the largest customer segment in the VSP software market, representing nearly 59.5% of global revenues.

Healthcare was the largest Industry Sector in the VSP software market, contributing US$25.1 billion, which accounted for approximately 18.2% of total global revenues.

Top players in the Vertical-Specific and Packaged (VSP) Software industry include enterprise giants like SAP, Oracle, Microsoft, and Salesforce, which offer industry cloud platforms tailored for sectors such as healthcare, finance, and manufacturing. Specialized vendors such as Veeva Systems, Epicor, Guidewire, and Cerner also play a critical role by delivering deep domain expertise and preconfigured, compliance-ready workflows for regulated verticals.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Vertical-Specific and Packaged (VSP) Software

- Market Segmentation for Vertical-Specific and Packaged (VSP) Software

- Deployment Types

- Company Types

- Applications

- Key Trends in Vertical-Specific and Packaged (VSP) Software Market

2. INDUSTRY LANDSCAPE

- Global Vertical-Specific and Packaged (VSP) Software Market Outlook

- Comprehensive Vertical-Specific and Packaged (VSP) Software Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Vertical-Specific and Packaged (VSP) Software Industry

- Startup Strategies for Vertical-Specific and Packaged (VSP) Software Industry

- SWOT Analysis of Vertical-Specific and Packaged (VSP) Software Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Vertical-Specific and Packaged (VSP) Software Companies

- Market Share Analysis of Vertical-Specific and Packaged (VSP) Software Companies

- SWOT Analysis of Key Players in the Vertical-Specific and Packaged (VSP) Software Industry

- Key Market Players

- Adobe Inc.

- Autodesk Inc.

- Blackbaud

- Cerner Corporation

- Epic Systems Corporation

- Epicor

- Guidewire

- IBM Corporation

- Infor Inc.

- Intuit Inc.

- McKesson Corporation

- Microsoft Corporation

- Oracle Corporation

- Paychex Inc.

- Sage Group plc

- Salesforce

- SAP SE

- ServiceTitan

- Tyler Technologies Inc.

- Veeva Systems

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Vertical-Specific and Packaged (VSP) Software Deployment Type Market Overview by Global Region

- Cloud

- On-Premise

- Global Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Vertical-Specific and Packaged (VSP) Software Company Type Market Overview by Global Region

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

- Global Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- Vertical-Specific and Packaged (VSP) Software Application Market Overview by Global Region

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

PART B: REGIONAL MARKET PERSPECTIVE

- Global Vertical-Specific and Packaged (VSP) Software Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Vertical-Specific and Packaged (VSP) Software Market Overview by Geographic Region

- North American Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- North American Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- North American Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- Country-wise Analysis of North American Vertical-Specific and Packaged (VSP) Software Market

- THE UNITED STATES

- United States Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- United States Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- United States Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- CANADA

- Canadian Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Canadian Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Canadian Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- MEXICO

- Mexican Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Mexican Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Mexican Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

7. EUROPE

- European Vertical-Specific and Packaged (VSP) Software Market Overview by Geographic Region

- European Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- European Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- European Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- Country-wise Analysis of European Vertical-Specific and Packaged (VSP) Software Market

- GERMANY

- German Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- German Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- German Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- THE UNITED KINGDOM

- United Kingdom Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- United Kingdom Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- United Kingdom Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- FRANCE

- French Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- French Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- French Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- ITALY

- Italian Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Italian Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Italian Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- THE NETHERLANDS

- Dutch Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Dutch Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Dutch Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- SPAIN

- Spanish Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Spanish Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Spanish Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- RUSSIA

- Russian Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Russian Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Russian Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- SWITZERLAND

- Swiss Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Swiss Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Swiss Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- REST OF EUROPE

- Rest of Europe Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Rest of Europe Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Rest of Europe Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Vertical-Specific and Packaged (VSP) Software Market Overview by Geographic Region

- Asia-Pacific Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Asia-Pacific Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Asia-Pacific Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- Country-wise Analysis of Asia-Pacific Vertical-Specific and Packaged (VSP) Software Market

- CHINA

- Chinese Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Chinese Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Chinese Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- JAPAN

- Japanese Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Japanese Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Japanese Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- INDIA

- Indian Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Indian Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Indian Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- AUSTRALIA

- Australia Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Australia Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Australia Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- SINGAPORE

- Singaporean Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Singaporean Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Singaporean Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- SOUTH KOREA

- South Korean Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- South Korean Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- South Korean Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Rest of Asia-Pacific Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Rest of Asia-Pacific Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

9. SOUTH AMERICA

- South American Vertical-Specific and Packaged (VSP) Software Market Overview by Geographic Region

- South American Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- South American Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- South American Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- Country-wise Analysis of South American Vertical-Specific and Packaged (VSP) Software Market

- BRAZIL

- Brazilian Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Brazilian Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Brazilian Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- ARGENTINA

- Argentine Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Argentine Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Argentine Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- COLOMBIA

- Colombian Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Colombian Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Colombian Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- CHILE

- Chilean Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Chilean Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Chilean Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- PERU

- Peruvian Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Peruvian Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Peruvian Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Rest of South America Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Rest of South America Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Vertical-Specific and Packaged (VSP) Software Market Overview by Geographic Region

- Middle East & Africa Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Middle East & Africa Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Middle East & Africa Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- Country-wise Analysis of Middle East & Africa Vertical-Specific and Packaged (VSP) Software Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- United Arab Emirates Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- United Arab Emirates Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- SOUTH AFRICA

- South African Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- South African Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- South African Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- EGYPT

- Egyptian Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Egyptian Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Egyptian Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- SAUDI ARABIA

- Saudi Arabian Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Saudi Arabian Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Saudi Arabian Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- MOROCCO

- Moroccan Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Moroccan Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Moroccan Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- KUWAIT

- Kuwaiti Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Kuwaiti Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Kuwaiti Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- QATAR

- Qatari Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Qatari Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Qatari Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Vertical-Specific and Packaged (VSP) Software Market Overview by Deployment Type

- Rest of Middle East & Africa Vertical-Specific and Packaged (VSP) Software Market Overview by Company Type

- Rest of Middle East & Africa Vertical-Specific and Packaged (VSP) Software Market Overview Industry Sector

PART C: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

Adobe Inc.

Autodesk Inc.

Blackbaud

Cerner Corporation

Epic Systems Corporation

Epicor

Guidewire

IBM Corporation

Infor Inc.

Intuit Inc.

McKesson Corporation

Microsoft Corporation

Oracle Corporation

Paychex Inc.

Sage Group plc

Salesforce

SAP SE

ServiceTitan

Tyler Technologies Inc.

Veeva Systems

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |