Application Life-Cycle Management (ALM) Software - A Global Market Overview

- Published: Sep 2025

- Pages: 574 | Charts: 494

- Report Code: ITM045

SHARE THIS REPORT:

Global Application Life-Cycle Management (ALM) Software Market Trends and Outlook

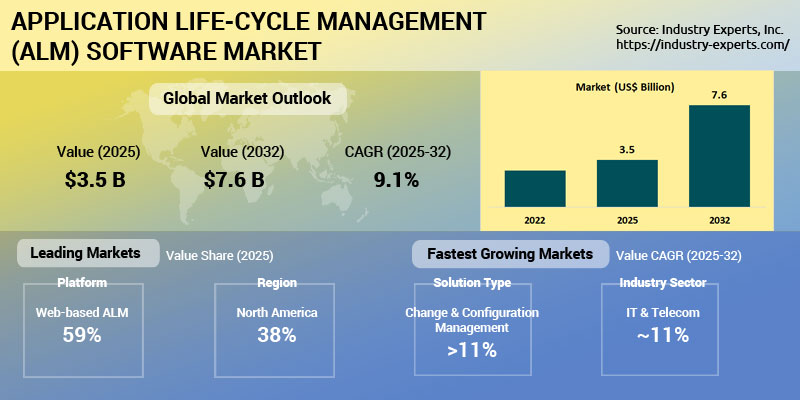

The global Application Life-Cycle Management (ALM) software market is set for steady expansion, rising from an estimated US$3.5 billion in 2025 to about US$7.6 billion by 2034, reflecting a CAGR of 9.1%. Growth is fueled by the increasing complexity of software development processes, where Agile, DevOps, and CI/CD practices have become mainstream. Organizations are turning to integrated ALM platforms to manage requirements, development, testing, deployment, and maintenance in a unified environment, reducing silos and accelerating delivery cycles.

Key market dynamics include the rise of cloud-based ALM, which enables scalability and supports hybrid and remote workforces, and the integration of AI and machine learning to enhance predictive analytics, automate testing, and improve defect detection. Security integration has become a critical imperative as enterprises face regulatory mandates like GDPR and HIPAA, while industry-specific customizations for BFSI, healthcare, manufacturing, and telecom add further traction. Challenges such as integration with legacy systems, high costs for SMEs, and skill shortages remain, yet opportunities abound in SaaS-based delivery, low-code/no-code capabilities, mobile workflows, and AI-driven lifecycle analytics. These drivers position ALM as a core enabler of digital transformation initiatives globally.

Major players in the ALM software market include IBM, Microsoft, Siemens, and PTC, alongside a dynamic mix of emerging vendors innovating with cloud-native and AI-integrated solutions. These companies compete on capabilities such as automation, compliance, integration, and scalability, shaping a vibrant and competitive landscape.

Application Life-Cycle Management (ALM) Software Regional Market Analysis

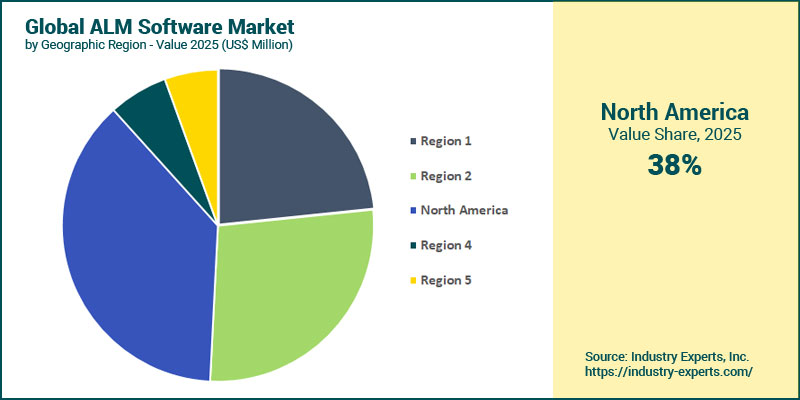

North America stands as the largest regional market in 2025, valued at roughly US$1.3 billion and accounting for 37.5% of global revenues, owing to its mature DevOps adoption, stringent compliance requirements, and early adoption of cloud-native and AI-driven ALM platforms. Europe follows closely, supported by regulatory mandates such as GDPR and a strong base of enterprise software vendors. Looking ahead, Asia-Pacific is projected to record the fastest growth at 11.6% CAGR, nearly doubling in size by 2034, driven by rapid digitization, escalating IT investments in China and India, and government-led digital transformation initiatives.

Application Life-Cycle Management (ALM) Software Market Analysis by Solution Type

Application Development is the leading segment in 2025, accounting for 31.4% of global demand, sustained by enterprises seeking integrated environments to streamline coding, version control, and collaboration across distributed teams. Application Testing follows closely, reflecting the increasing emphasis on automated testing, continuous quality assurance, and compliance-driven validation. Through the forecast period, Change and Configuration Management is set to be the fastest-growing segment, expanding at 11.4% CAGR, fueled by the rising complexity of software portfolios, demand for agile change tracking, and the integration of DevSecOps practices. Application Testing also demonstrates strong momentum, underpinned by the need for AI-driven test automation, continuous integration pipelines, and risk-based quality management.

Application Life-Cycle Management (ALM) Software Market Analysis by Platform

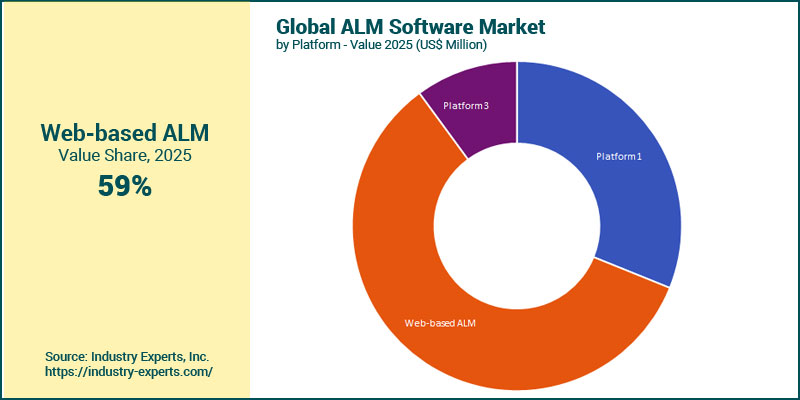

Web-based ALM dominates in 2025, generating US$2.0 billion and accounting for 58.8% of the market, thanks to its scalability, accessibility, and suitability for hybrid and distributed development teams. Mobile-based ALM follows, supported by the growing shift to mobile-first development, remote collaboration needs, and the demand for on-the-go access to lifecycle workflows. Over the forecast horizon, Mobile-based ALM is expected to grow the fastest at a CAGR of 10.7%, more than doubling by 2034, driven by mobile workforce expansion, rising mobile app development, and real-time collaboration requirements. In contrast, Other Platforms segment lags with a lower CAGR, reflecting the gradual decline of legacy and niche systems in favor of cloud and mobile-native ALM suites.

Application Life-Cycle Management (ALM) Software Market Analysis by Deployment Type

Cloud-based ALM dominates in 2025, representing 67% of the global market, driven by its scalability, cost efficiency, and ability to support remote and hybrid development teams. Over the forecast period, Cloud-based ALM is projected to be the fastest-growing segment at 9.3% CAGR, reaching US$5.2 billion by 2034, supported by SaaS adoption, cloud-native architectures, and integration with DevOps pipelines. On-Premises ALM will expand more modestly to US$2.4 billion, maintaining relevance where data sovereignty and legacy systems dictate slower transitions to cloud environments.

Application Life-Cycle Management (ALM) Software Market Analysis by Company Type

Large enterprises dominate in 2025, accounting for 71.7% of global revenues, supported by their need to manage complex application portfolios, ensure compliance, and integrate ALM into enterprise-scale DevOps pipelines. Over the forecast horizon, SMEs are expected to register the fastest growth at 12% CAGR, nearly tripling their market size by 2034. This acceleration is driven by the democratization of ALM tools through SaaS delivery, low-code/no-code integration, and AI-powered automation, which lower entry barriers and make lifecycle management accessible to smaller firms. Large enterprises will expand more moderately, maintaining their lead as digital transformation and compliance pressures remain strong.

Application Life-Cycle Management (ALM) Software Market Analysis by Industry Sector

IT & Telecom is the largest sector in 2025, representing 24% of the market, driven by the industry's continuous innovation cycles, complex application ecosystems, and heavy reliance on agile DevOps practices. BFSI closely follows, supported by stringent compliance needs, risk management, and the push for secure, scalable ALM solutions across digital banking and financial services. Over the forecast period, IT & Telecom is also projected to be the fastest-growing sector, expanding at 11.1% CAGR to surpass US$2.1 billion by 2034, propelled by 5G, IoT, and cloud-native services that demand agile and secure software lifecycles. BFSI also demonstrates strong growth momentum, underpinned by regulatory mandates, digital-first strategies, and the integration of AI-powered lifecycle analytics to ensure traceability and audit readiness.

ALM Software Market Report Scope

This global report on Application Life-Cycle Management (ALM) Software market analyzes the global and regional market based on Solution Type, Platform, Deployment Type, Company Type and Industry Sector for the period 2022-2034 with forecasts from 2025 to 2034 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Analysis Period: | 2022-2034 | |

| Base Year: | 2025 | |

| Forecast Period: | 2025-2034 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 25+ |

Application Life-Cycle Management (ALM) Software Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Application Life-Cycle Management (ALM) Software Market by Solution Type

- Application Development

- Application Testing

- Change and Configuration Management

- Project and Portfolio Management

- Other Supporting Functions

Application Life-Cycle Management (ALM) Software Market by Platform

- Web-based ALM

- Mobile-based ALM

- Other Platforms

Application Life-Cycle Management (ALM) Software Market by Deployment Type

- Cloud

- On-Premises

Application Life-Cycle Management (ALM) Software Market by Company Type

- Large Enterprises

- SMEs

Application Life-Cycle Management (ALM) Software Market by Industry Sector

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Healthcare & Life Sciences

- Government

- Retail & E-commerce

- Manufacturing

- Energy & Utilities

- Transportation & Logistics

- Media & Entertainment

- Education

- Other Industry Sectors

ALM Software Market Frequently Asked Questions (FAQs)

The market is valued at US$3.5 billion in 2025 and is projected to reach US$7.6 billion by 2034.

The market is forecast to grow at a CAGR of 9.1% between 2025 and 2034.

North America leads in 2025 with a 37.5% share, supported by a mature DevOps ecosystem, strong compliance demands, and advanced cloud-native adoption.

Asia-Pacific is expected to grow the fastest, recording 11.6% CAGR to exceed US$2.1 billion by 2034, fueled by rapid digitization and IT investments in China and India.

Application Development is the largest solution type in 2025, representing 31.4% of the market, as enterprises prioritize integrated environments for coding and collaboration.

SMEs are expected to grow the fastest at 12% CAGR, benefiting from SaaS-based delivery, low-code/no-code platforms, and AI-powered automation.

Key trends include the rise of cloud-native ALM, AI and ML integration for predictive insights, DevSecOps and embedded security, low-code/no-code adoption, mobile workflows, and industry-specific compliance solutions.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Application Life-Cycle Management (ALM) Software

- Market Segmentation for Application Life-Cycle Management (ALM) Software

- Solution Types

- Platforms

- Deployment Types

- Company Types

- Industry Sectors

- Key Trends in Application Life-Cycle Management (ALM) Software Market

2. INDUSTRY LANDSCAPE

- Global Application Life-Cycle Management (ALM) Software Market Outlook

- Comprehensive Application Life-Cycle Management (ALM) Software Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Application Life-Cycle Management (ALM) Software Industry

- Startup Strategies for Application Life-Cycle Management (ALM) Software Industry

- SWOT Analysis of Application Life-Cycle Management (ALM) Software Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Application Life-Cycle Management (ALM) Software Companies

- Market Share Analysis of Application Life-Cycle Management (ALM) Software Companies

- SWOT Analysis of Key Players in the Application Life-Cycle Management (ALM) Software Industry

- Key Market Players

- Atlassian Corporation Plc

- Broadcom (including CA Technologies)

- Dassault Syst�mes

- Digital.ai

- Enalean

- GitLab

- HCLTech

- HP Development Company, L.P.

- Inflectra Corporation

- International Business Machines Corporation (IBM)

- Jama Software

- Kovair Software

- Micro Focus International plc

- Microsoft

- Novalys

- OpenText

- Orcanos

- Original Software

- Parasoft Corporation

- Perforce

- Polarion Software GmbH

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Application Life-Cycle Management (ALM) Software Market Overview by Type

- Application Life-Cycle Management (ALM) Solution Type Market Overview by Global Region

- Application Development

- Application Testing

- Change and Configuration Management

- Project and Portfolio Management

- Other Supporting Functions

- Global Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Application Life-Cycle Management (ALM) Software Platform Market Overview by Global Region

- Web-based ALM

- Mobile-based ALM

- Other Platforms

- Global Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Application Life-Cycle Management (ALM) Software Deployment Type Market Overview by Global Region

- Cloud

- On-Premises

- Global Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Application Life-Cycle Management (ALM) Software Company Type Market Overview by Global Region

- Large Enterprises

- SMEs

- Global Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- Application Life-Cycle Management (ALM) Software Industry Sector Market Overview by Global Region

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Healthcare & Life Sciences

- Government

- Retail & E-commerce

- Manufacturing

- Energy & Utilities

- Transportation & Logistics

- Media & Entertainment

- Education

- Other Industry Sectors

PART B: REGIONAL MARKET PERSPECTIVE

- Global Application Life-Cycle Management (ALM) Software Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Application Life-Cycle Management (ALM) Software Market Overview by Geographic Region

- North American Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- North American Application Life-Cycle Management (ALM) Software Market Overview by Platform

- North American Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- North American Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- North American Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- Country-wise Analysis of North American Application Life-Cycle Management (ALM) Software Market

- THE UNITED STATES

- United States Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- United States Application Life-Cycle Management (ALM) Software Market Overview by Platform

- United States Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- United States Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- United States Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- CANADA

- Canadian Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Canadian Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Canadian Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Canadian Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Canadian Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- MEXICO

- Mexican Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Mexican Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Mexican Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Mexican Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Mexican Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

7. EUROPE

- European Application Life-Cycle Management (ALM) Software Market Overview by Geographic Region

- European Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- European Application Life-Cycle Management (ALM) Software Market Overview by Platform

- European Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- European Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- European Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- Country-wise Analysis of European Application Life-Cycle Management (ALM) Software Market

- GERMANY

- German Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- German Application Life-Cycle Management (ALM) Software Market Overview by Platform

- German Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- German Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- German Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- United Kingdom Application Life-Cycle Management (ALM) Software Market Overview by Platform

- United Kingdom Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- United Kingdom Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- United Kingdom Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- FRANCE

- French Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- French Application Life-Cycle Management (ALM) Software Market Overview by Platform

- French Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- French Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- French Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- ITALY

- Italian Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Italian Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Italian Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Italian Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Italian Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Dutch Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Dutch Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Dutch Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Dutch Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- SPAIN

- Spanish Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Spanish Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Spanish Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Spanish Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Spanish Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- RUSSIA

- Russian Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Russian Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Russian Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Russian Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Russian Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- SWITZERLAND

- Swiss Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Swiss Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Swiss Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Swiss Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Swiss Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Rest of Europe Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Rest of Europe Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Rest of Europe Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Rest of Europe Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Application Life-Cycle Management (ALM) Software Market Overview by Geographic Region

- Asia-Pacific Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Asia-Pacific Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Asia-Pacific Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Asia-Pacific Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Asia-Pacific Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Application Life-Cycle Management (ALM) Software Market

- CHINA

- Chinese Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Chinese Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Chinese Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Chinese Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Chinese Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- JAPAN

- Japanese Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Japanese Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Japanese Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Japanese Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Japanese Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- INDIA

- Indian Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Indian Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Indian Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Indian Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Indian Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- AUSTRALIA

- Australia Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Australia Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Australia Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Australia Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Australia Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- SINGAPORE

- Singaporean Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Singaporean Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Singaporean Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Singaporean Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Singaporean Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- South Korean Application Life-Cycle Management (ALM) Software Market Overview by Platform

- South Korean Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- South Korean Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- South Korean Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Rest of Asia-Pacific Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Rest of Asia-Pacific Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Rest of Asia-Pacific Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Rest of Asia-Pacific Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Application Life-Cycle Management (ALM) Software Market Overview by Geographic Region

- South American Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- South American Application Life-Cycle Management (ALM) Software Market Overview by Platform

- South American Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- South American Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- South American Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- Country-wise Analysis of South American Application Life-Cycle Management (ALM) Software Market

- BRAZIL

- Brazilian Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Brazilian Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Brazilian Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Brazilian Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Brazilian Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- ARGENTINA

- Argentine Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Argentine Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Argentine Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Argentine Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Argentine Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- COLOMBIA

- Colombian Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Colombian Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Colombian Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Colombian Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Colombian Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- CHILE

- Chilean Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Chilean Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Chilean Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Chilean Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Chilean Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- PERU

- Peruvian Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Peruvian Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Peruvian Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Peruvian Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Peruvian Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Rest of South America Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Rest of South America Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Rest of South America Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Rest of South America Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Application Life-Cycle Management (ALM) Software Market Overview by Geographic Region

- Middle East & Africa Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Middle East & Africa Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Middle East & Africa Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Middle East & Africa Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Middle East & Africa Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Application Life-Cycle Management (ALM) Software Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- United Arab Emirates Application Life-Cycle Management (ALM) Software Market Overview by Platform

- United Arab Emirates Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- United Arab Emirates Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- United Arab Emirates Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- SOUTH AFRICA

- South African Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- South African Application Life-Cycle Management (ALM) Software Market Overview by Platform

- South African Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- South African Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- South African Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- EGYPT

- Egyptian Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Egyptian Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Egyptian Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Egyptian Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Egyptian Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Saudi Arabian Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Saudi Arabian Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Saudi Arabian Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Saudi Arabian Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- MOROCCO

- Moroccan Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Moroccan Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Moroccan Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Moroccan Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Moroccan Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Kuwaiti Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Kuwaiti Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Kuwaiti Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Kuwaiti Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- QATAR

- Qatari Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Qatari Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Qatari Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Qatari Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Qatari Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Application Life-Cycle Management (ALM) Software Market Overview by Solution Type

- Rest of Middle East & Africa Application Life-Cycle Management (ALM) Software Market Overview by Platform

- Rest of Middle East & Africa Application Life-Cycle Management (ALM) Software Market Overview by Deployment Type

- Rest of Middle East & Africa Application Life-Cycle Management (ALM) Software Market Overview by Company Type

- Rest of Middle East & Africa Application Life-Cycle Management (ALM) Software Market Overview by Industry Sector

PART C: INDUSTRY GUIDE

PART D: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

Atlassian Corporation Plc

Broadcom (including CA Technologies)

Dassault Systemes

Digital.ai

Enalean

GitLab

HCLTech

HP Development Company, L.P.

Inflectra Corporation

International Business Machines Corporation (IBM)

Jama Software

Kovair Software

Micro Focus International plc

Microsoft

Novalys

OpenText

Orcanos

Original Software

Parasoft Corporation

Perforce

Polarion Software GmbH

Practitest

PTC

ReQtest

Rocket Software

SAP SE

Siemens

TestRail

Visure Solutions

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |

| Network Access Control (NAC) Hardware - A Global Market Overview | Aug 21, 2025 | $5490 |