Telecom Expense Management - A Global Market Overview

- Published: Aug 2025

- Pages: 568 | Charts: 492

- Report Code: ITM054

SHARE THIS REPORT:

Global Telecom Expense Management Market Trends and Outlook

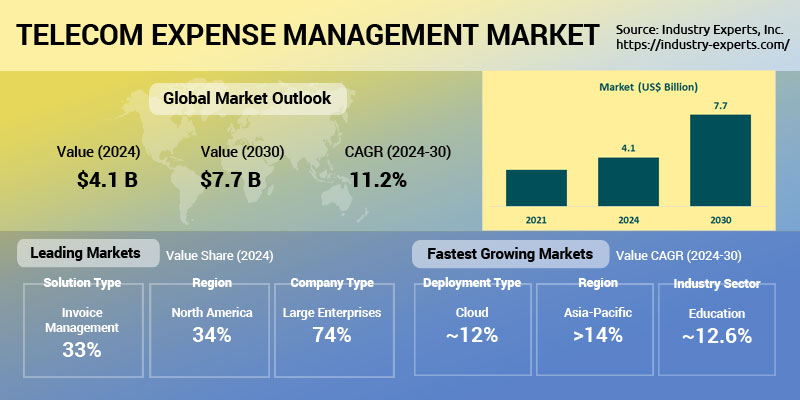

The global Telecom Expense Management (TEM) market reached a value of approximately US$4.1 billion in 2024 and is projected to expand at a robust CAGR of 11.2%, surpassing US$7.7 billion by 2030. This strong growth trajectory is underpinned by the mounting complexity of enterprise telecom environments, the proliferation of hybrid workforces, and the increasing adoption of cloud-based unified communications (UC) platforms. As enterprises contend with multi-carrier contracts, global roaming expenses, and decentralized telecom usage, TEM is evolving from a cost containment tool into a strategic enabler of visibility, compliance, and operational agility.

Several transformative trends are reshaping the TEM landscape. Cloud-native and SaaS-based delivery models now dominate, accounting for over 65% of implementations in 2024, driven by their scalability, faster deployment, and lower upfront costs. The integration of artificial intelligence and predictive analytics is also redefining value creation, with platforms now capable of automating invoice validation, detecting anomalies, and optimizing telecom spend in real time. Furthermore, the convergence of TEM with UC management, spanning tools like Microsoft Teams and Zoom, is providing enterprises with holistic control over their communications ecosystems. Sustained demand for managed services, growing SME adoption, and rising ESG-related use cases (such as e-waste tracking and device lifecycle optimization) are expected to further accelerate market expansion through 2030.

Leading players in the global Telecom Expense Management (TEM) market include Tangoe, Calero-MDSL, Sakon, and Cass Information Systems, all of which offer comprehensive platforms combining expense visibility, contract optimization, and compliance reporting. Emerging SaaS vendors and specialists like brightfin, Tellennium, and Upland Software (Cimpl) are also gaining traction by targeting SMEs with modular, subscription-based solutions.

Telecom Expense Management Regional Market Analysis

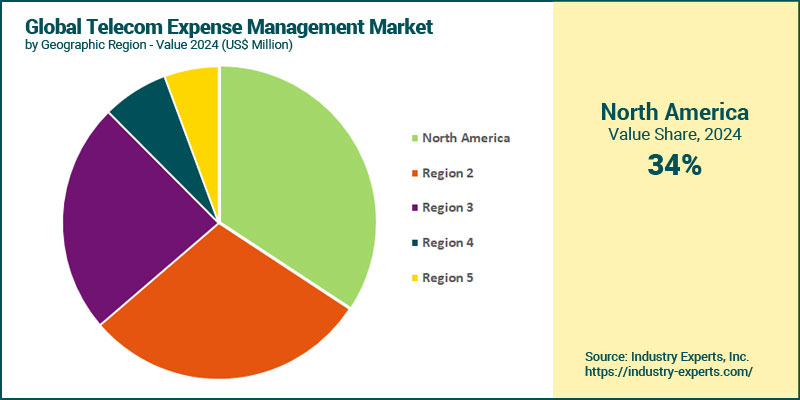

In 2024, North America led the global TEM market with a share of approximately 34.2% of global revenue. This dominance is fueled by mature enterprise adoption, regulatory mandates like SOX and PCI DSS, and widespread implementation of managed TEM services. Sustained demand from Fortune 1000 enterprises, particularly in finance, healthcare, and technology sectors, continues to anchor growth. Asia Pacific is experiencing the fastest expansion, projected to post a CAGR of 14.4% through 2030. This growth is driven by aggressive digital transformation in countries such as China, India, and Southeast Asia, where cloud-first strategies, SME adoption, and rising complexity in telecom environments are fueling demand for scalable, SaaS-based TEM platforms. The region's increasing prioritization of cost control across hybrid and multi-carrier ecosystems also supports sustained momentum.

Telecom Expense Management Market Analysis by Solution Type

Invoice Management remained the dominant solution type in 2024, accounting for 33.1% of the global TEM market. This segment's leadership stems from its foundational role in telecom cost reconciliation, error detection, and audit-readiness across large enterprises. The demand is further driven by AI-powered automation, which is transforming legacy invoice workflows. Usage Management is projected to register the fastest growth, expanding at a CAGR of 13%. This surge is attributed to rising demand for real-time visibility and control over communications usage across hybrid work environments and unified communication (UC) platforms. Enterprises are increasingly adopting solutions that integrate telecom and UC usage analytics, enabling more dynamic cost allocation and proactive policy enforcement.

Telecom Expense Management Market Analysis by Service Type

Hosted Services remained the dominant revenue contributor in 2024, representing 62.3% of total global TEM revenue. This stronghold is attributed to the widespread adoption of cloud-based platforms that offer rapid deployment, scalability, and lower upfront costs. Enterprises across regions are increasingly favoring SaaS-based TEM for cost transparency, remote accessibility, and seamless integration with UCaaS and cloud ERP systems. Managed Services is the fastest-growing segment, expanding at a CAGR of 12.2%. This momentum reflects a growing enterprise preference for outsourcing end-to-end telecom lifecycle functions, including procurement, contract negotiation, dispute resolution, and compliance reporting. The model is especially attractive to multinationals and mid-sized firms lacking in-house telecom governance capabilities.

Telecom Expense Management Market Analysis by Deployment Type

Cloud-based deployment leads the global TEM market, which represents 63.6% of the total market. By 2030, this segment is projected to surpass US$5 billion, expanding at a CAGR of 11.7%. The dominance and rapid growth of cloud deployment are driven by enterprise demand for scalable, cost-efficient, and rapidly deployable solutions. SaaS models are particularly favored for their ability to support multi-location telecom ecosystems, facilitate remote operations, and integrate AI-powered automation. This trend aligns with the broader shift toward cloud-first IT strategies across industries. On-premise deployment, while still significant, is growing at a slower pace. Despite the shift to cloud, this segment continues to serve sectors with strict data residency and compliance requirements, such as government, defense, and certain financial institutions. On-premise platforms are often favored where telecom infrastructure is deeply integrated into proprietary IT environments or where customization and internal control are paramount.

Telecom Expense Management Market Analysis by Company Type

Large enterprises continue to account for the majority of global TEM spending, representing 74.2% of the total market in 2024. By 2030, spending by large enterprises is expected to climb to approximately US$5.6 billion. The sustained dominance of this segment is driven by the complexity of managing multi-national telecom contracts, demand for fully managed services, and increasing reliance on AI-driven analytics for spend optimization, compliance, and risk mitigation. SMEs are emerging as the fastest-growing customer base, posting a 2024-2030 CAGR of 12.2%. This acceleration is supported by the increasing availability of modular, subscription-based TEM platforms designed specifically for mid-sized companies. SaaS-based deployments, simplified analytics, and cost transparency are key enablers making TEM more accessible to SMEs, especially in rapidly digitizing markets across Asia Pacific, Europe, and Latin America.

Telecom Expense Management Market Analysis by Industry Sector

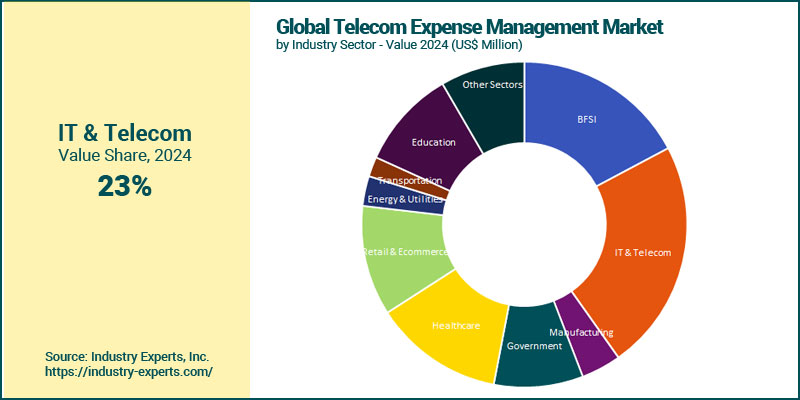

In 2024, the IT & Telecom sector led all industries with an estimated share of 23% of the global TEM revenue. This leadership is due to the inherently telecom-intensive operations of IT service providers and network operators, which demand granular cost visibility, multi-vendor optimization, and UCaaS integration. Strategic focus on AI-powered analytics, cloud-native communications, and global roaming optimization will continue to drive growth in this vertical. Education is the fastest-growing industry sector, projected to post at a CAGR of 12.6%. The rapid shift toward hybrid learning models, expanded digital infrastructure in universities and schools, and rising adoption of cloud-based collaboration tools are driving demand for telecom cost control and unified communication visibility across educational institutions. The Healthcare sector follows closely, registering a CAGR of 12.3%.

Telecom Expense Management Market Report Scope

This global report on Telecom Expense Management market analyzes the global and regional market based on Solution Type, Service Type, Deployment Type, Company Type and Industry Sector for the period 2021-2030 with forecasts from 2024 to 2030 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Historical Period: | 2021-2024 | |

| Base Year: | 2024 | |

| Forecast Period: | 2024-2030 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 25+ |

Telecom Expense Management Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Telecom Expense Management Market by Solution Type

- Invoice Management

- Ordering & Provisioning Management

- Dispute Management

- Sourcing Management

- Usage Management

- Other Solution Types

Telecom Expense Management Market by Service Type

- Hosted Services

- Managed Services

Telecom Expense Management Market by Deployment Type

- Cloud

- On-Premises

Telecom Expense Management Market by Company Type

- Large Enterprises

- SMEs

Telecom Expense Management Market by Industry Sector

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

Telecom Expense Management Market Frequently Asked Questions (FAQs)

Telecom Expense Management (TEM) refers to the systems and processes used by enterprises to manage, control, and optimize costs related to telecom and communication services. As telecom environments become more complex with hybrid work, multi-carrier contracts, and cloud-based UC tools, TEM is critical for ensuring cost transparency, regulatory compliance, and operational efficiency.

The global TEM market was valued at approximately US$4.1 billion in 2024 and is projected to exceed US$7.7 billion by 2030, growing at a CAGR of 11.2%, driven by cloud adoption, AI-powered analytics, and rising demand for managed services.

North America is the largest regional market due to mature enterprise adoption and regulatory mandates, while Asia Pacific is the fastest-growing region, fueled by digital transformation, SME demand, and cloud-first strategies in countries like India and China.

Major growth drivers include the expansion of hybrid and remote workforces, increasing telecom complexity, widespread adoption of cloud communications platforms, regulatory compliance needs, and the integration of AI and predictive analytics in TEM platforms.

AI and machine learning are enhancing TEM capabilities by automating invoice validation, identifying billing anomalies, benchmarking contracts, and generating predictive insights, reducing manual overhead and uncovering cost-saving opportunities.

Leading companies include Tangoe, Calero-MDSL, Sakon, and Cass Information Systems, while innovators like brightfin, Upland Software, and Tellennium are gaining traction with modular SaaS offerings, particularly among SMEs.

Hosted (cloud-based) and managed services dominate the market, with hosted solutions preferred for their scalability and cost-effectiveness, while managed services appeal to large enterprises seeking full lifecycle support, from procurement to compliance reporting.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Telecom Expense Management

- Market Segmentation for Telecom Expense Management

- Solution Types

- Service Types

- Deployment Types

- Company Types

- Industry Sectors

- Key Trends in Telecom Expense Management Market

2. INDUSTRY LANDSCAPE

- Global Telecom Expense Management Market Outlook

- Comprehensive Telecom Expense Management Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Telecom Expense Management Industry

- Startup Strategies for Telecom Expense Management Industry

- SWOT Analysis of Telecom Expense Management Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Telecom Expense Management Companies

- Market Share Analysis of Telecom Expense Management Companies

- SWOT Analysis of Key Players in the Telecom Expense Management Industry

- Key Market Players

- Accenture

- Anatole

- Avotus

- brightfin

- Calero-MDSL

- Cass Information Systems

- CGI Inc.

- Cimpl

- Comview

- Dimension Data (NTT Communications)

- Econocom

- Habble

- ICOMM

- Mindglobal

- NTT Limited

- One Source Communications

- RadiusPoint

- Sakon

- Tangoe

- TeleManagement Technologies, Inc.

- Telesoft

- Tellennium

- Upland Software (Cimpl)

- Valicom

- Vodafone Group Plc

- VoicePlus

- WidePoint

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Telecom Expense Management Market Overview by Type

- Telecom Expense Management Type Market Overview by Global Region

- Invoice Management

- Ordering & Provisioning Management

- Dispute Management

- Sourcing Management

- Usage Management

- Other Solution Types

- Global Telecom Expense Management Market Overview by Service Type

- Telecom Expense Management Service Type Market Overview by Global Region

- Hosted Services

- Managed Services

- Global Telecom Expense Management Market Overview by Deployment Type

- Telecom Expense Management Deployment Type Market Overview by Global Region

- Cloud

- On-Premises

- Global Telecom Expense Management Market Overview by Company Type

- Telecom Expense Management Company Type Market Overview by Global Region

- Large Enterprises

- SMEs

- Global Telecom Expense Management Market Overview by Industry Sector

- Telecom Expense Management Industry Sector Market Overview by Global Region

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

PART B: REGIONAL MARKET PERSPECTIVE

- Global Telecom Expense Management Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Telecom Expense Management Market Overview by Geographic Region

- North American Telecom Expense Management Market Overview by Solution Type

- North American Telecom Expense Management Market Overview by Service Type

- North American Telecom Expense Management Market Overview by Deployment Type

- North American Telecom Expense Management Market Overview by Company Type

- North American Telecom Expense Management Market Overview by Industry Sector

- Country-wise Analysis of North American Telecom Expense Management Market

- THE UNITED STATES

- United States Telecom Expense Management Market Overview by Solution Type

- United States Telecom Expense Management Market Overview by Service Type

- United States Telecom Expense Management Market Overview by Deployment Type

- United States Telecom Expense Management Market Overview by Company Type

- United States Telecom Expense Management Market Overview by Industry Sector

- CANADA

- Canadian Telecom Expense Management Market Overview by Solution Type

- Canadian Telecom Expense Management Market Overview by Service Type

- Canadian Telecom Expense Management Market Overview by Deployment Type

- Canadian Telecom Expense Management Market Overview by Company Type

- Canadian Telecom Expense Management Market Overview by Industry Sector

- MEXICO

- Mexican Telecom Expense Management Market Overview by Solution Type

- Mexican Telecom Expense Management Market Overview by Service Type

- Mexican Telecom Expense Management Market Overview by Deployment Type

- Mexican Telecom Expense Management Market Overview by Company Type

- Mexican Telecom Expense Management Market Overview by Industry Sector

7. EUROPE

- European Telecom Expense Management Market Overview by Geographic Region

- European Telecom Expense Management Market Overview by Solution Type

- European Telecom Expense Management Market Overview by Service Type

- European Telecom Expense Management Market Overview by Deployment Type

- European Telecom Expense Management Market Overview by Company Type

- European Telecom Expense Management Market Overview by Industry Sector

- Country-wise Analysis of European Telecom Expense Management Market

- GERMANY

- German Telecom Expense Management Market Overview by Solution Type

- German Telecom Expense Management Market Overview by Service Type

- German Telecom Expense Management Market Overview by Deployment Type

- German Telecom Expense Management Market Overview by Company Type

- German Telecom Expense Management Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Telecom Expense Management Market Overview by Solution Type

- United Kingdom Telecom Expense Management Market Overview by Service Type

- United Kingdom Telecom Expense Management Market Overview by Deployment Type

- United Kingdom Telecom Expense Management Market Overview by Company Type

- United Kingdom Telecom Expense Management Market Overview by Industry Sector

- FRANCE

- French Telecom Expense Management Market Overview by Solution Type

- French Telecom Expense Management Market Overview by Service Type

- French Telecom Expense Management Market Overview by Deployment Type

- French Telecom Expense Management Market Overview by Company Type

- French Telecom Expense Management Market Overview by Industry Sector

- ITALY

- Italian Telecom Expense Management Market Overview by Solution Type

- Italian Telecom Expense Management Market Overview by Service Type

- Italian Telecom Expense Management Market Overview by Deployment Type

- Italian Telecom Expense Management Market Overview by Company Type

- Italian Telecom Expense Management Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Telecom Expense Management Market Overview by Solution Type

- Dutch Telecom Expense Management Market Overview by Service Type

- Dutch Telecom Expense Management Market Overview by Deployment Type

- Dutch Telecom Expense Management Market Overview by Company Type

- Dutch Telecom Expense Management Market Overview by Industry Sector

- SPAIN

- Spanish Telecom Expense Management Market Overview by Solution Type

- Spanish Telecom Expense Management Market Overview by Service Type

- Spanish Telecom Expense Management Market Overview by Deployment Type

- Spanish Telecom Expense Management Market Overview by Company Type

- Spanish Telecom Expense Management Market Overview by Industry Sector

- RUSSIA

- Russian Telecom Expense Management Market Overview by Solution Type

- Russian Telecom Expense Management Market Overview by Service Type

- Russian Telecom Expense Management Market Overview by Deployment Type

- Russian Telecom Expense Management Market Overview by Company Type

- Russian Telecom Expense Management Market Overview by Industry Sector

- SWITZERLAND

- Swiss Telecom Expense Management Market Overview by Solution Type

- Swiss Telecom Expense Management Market Overview by Service Type

- Swiss Telecom Expense Management Market Overview by Deployment Type

- Swiss Telecom Expense Management Market Overview by Company Type

- Swiss Telecom Expense Management Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Telecom Expense Management Market Overview by Solution Type

- Rest of Europe Telecom Expense Management Market Overview by Service Type

- Rest of Europe Telecom Expense Management Market Overview by Deployment Type

- Rest of Europe Telecom Expense Management Market Overview by Company Type

- Rest of Europe Telecom Expense Management Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Telecom Expense Management Market Overview by Geographic Region

- Asia-Pacific Telecom Expense Management Market Overview by Solution Type

- Asia-Pacific Telecom Expense Management Market Overview by Service Type

- Asia-Pacific Telecom Expense Management Market Overview by Deployment Type

- Asia-Pacific Telecom Expense Management Market Overview by Company Type

- Asia-Pacific Telecom Expense Management Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Telecom Expense Management Market

- CHINA

- Chinese Telecom Expense Management Market Overview by Solution Type

- Chinese Telecom Expense Management Market Overview by Service Type

- Chinese Telecom Expense Management Market Overview by Deployment Type

- Chinese Telecom Expense Management Market Overview by Company Type

- Chinese Telecom Expense Management Market Overview by Industry Sector

- JAPAN

- Japanese Telecom Expense Management Market Overview by Solution Type

- Japanese Telecom Expense Management Market Overview by Service Type

- Japanese Telecom Expense Management Market Overview by Deployment Type

- Japanese Telecom Expense Management Market Overview by Company Type

- Japanese Telecom Expense Management Market Overview by Industry Sector

- INDIA

- Indian Telecom Expense Management Market Overview by Solution Type

- Indian Telecom Expense Management Market Overview by Service Type

- Indian Telecom Expense Management Market Overview by Deployment Type

- Indian Telecom Expense Management Market Overview by Company Type

- Indian Telecom Expense Management Market Overview by Industry Sector

- AUSTRALIA

- Australia Telecom Expense Management Market Overview by Solution Type

- Australia Telecom Expense Management Market Overview by Service Type

- Australia Telecom Expense Management Market Overview by Deployment Type

- Australia Telecom Expense Management Market Overview by Company Type

- Australia Telecom Expense Management Market Overview by Industry Sector

- SINGAPORE

- Singaporean Telecom Expense Management Market Overview by Solution Type

- Singaporean Telecom Expense Management Market Overview by Service Type

- Singaporean Telecom Expense Management Market Overview by Deployment Type

- Singaporean Telecom Expense Management Market Overview by Company Type

- Singaporean Telecom Expense Management Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Telecom Expense Management Market Overview by Solution Type

- South Korean Telecom Expense Management Market Overview by Service Type

- South Korean Telecom Expense Management Market Overview by Deployment Type

- South Korean Telecom Expense Management Market Overview by Company Type

- South Korean Telecom Expense Management Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Telecom Expense Management Market Overview by Solution Type

- Rest of Asia-Pacific Telecom Expense Management Market Overview by Service Type

- Rest of Asia-Pacific Telecom Expense Management Market Overview by Deployment Type

- Rest of Asia-Pacific Telecom Expense Management Market Overview by Company Type

- Rest of Asia-Pacific Telecom Expense Management Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Telecom Expense Management Market Overview by Geographic Region

- South American Telecom Expense Management Market Overview by Solution Type

- South American Telecom Expense Management Market Overview by Service Type

- South American Telecom Expense Management Market Overview by Deployment Type

- South American Telecom Expense Management Market Overview by Company Type

- South American Telecom Expense Management Market Overview by Industry Sector

- Country-wise Analysis of South American Telecom Expense Management Market

- BRAZIL

- Brazilian Telecom Expense Management Market Overview by Solution Type

- Brazilian Telecom Expense Management Market Overview by Service Type

- Brazilian Telecom Expense Management Market Overview by Deployment Type

- Brazilian Telecom Expense Management Market Overview by Company Type

- Brazilian Telecom Expense Management Market Overview by Industry Sector

- ARGENTINA

- Argentine Telecom Expense Management Market Overview by Solution Type

- Argentine Telecom Expense Management Market Overview by Service Type

- Argentine Telecom Expense Management Market Overview by Deployment Type

- Argentine Telecom Expense Management Market Overview by Company Type

- Argentine Telecom Expense Management Market Overview by Industry Sector

- COLOMBIA

- Colombian Telecom Expense Management Market Overview by Solution Type

- Colombian Telecom Expense Management Market Overview by Service Type

- Colombian Telecom Expense Management Market Overview by Deployment Type

- Colombian Telecom Expense Management Market Overview by Company Type

- Colombian Telecom Expense Management Market Overview by Industry Sector

- CHILE

- Chilean Telecom Expense Management Market Overview by Solution Type

- Chilean Telecom Expense Management Market Overview by Service Type

- Chilean Telecom Expense Management Market Overview by Deployment Type

- Chilean Telecom Expense Management Market Overview by Company Type

- Chilean Telecom Expense Management Market Overview by Industry Sector

- PERU

- Peruvian Telecom Expense Management Market Overview by Solution Type

- Peruvian Telecom Expense Management Market Overview by Service Type

- Peruvian Telecom Expense Management Market Overview by Deployment Type

- Peruvian Telecom Expense Management Market Overview by Company Type

- Peruvian Telecom Expense Management Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Telecom Expense Management Market Overview by Solution Type

- Rest of South America Telecom Expense Management Market Overview by Service Type

- Rest of South America Telecom Expense Management Market Overview by Deployment Type

- Rest of South America Telecom Expense Management Market Overview by Company Type

- Rest of South America Telecom Expense Management Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Telecom Expense Management Market Overview by Geographic Region

- Middle East & Africa Telecom Expense Management Market Overview by Solution Type

- Middle East & Africa Telecom Expense Management Market Overview by Service Type

- Middle East & Africa Telecom Expense Management Market Overview by Deployment Type

- Middle East & Africa Telecom Expense Management Market Overview by Company Type

- Middle East & Africa Telecom Expense Management Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Telecom Expense Management Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Telecom Expense Management Market Overview by Solution Type

- United Arab Emirates Telecom Expense Management Market Overview by Service Type

- United Arab Emirates Telecom Expense Management Market Overview by Deployment Type

- United Arab Emirates Telecom Expense Management Market Overview by Company Type

- United Arab Emirates Telecom Expense Management Market Overview by Industry Sector

- SOUTH AFRICA

- South African Telecom Expense Management Market Overview by Solution Type

- South African Telecom Expense Management Market Overview by Service Type

- South African Telecom Expense Management Market Overview by Deployment Type

- South African Telecom Expense Management Market Overview by Company Type

- South African Telecom Expense Management Market Overview by Industry Sector

- EGYPT

- Egyptian Telecom Expense Management Market Overview by Solution Type

- Egyptian Telecom Expense Management Market Overview by Service Type

- Egyptian Telecom Expense Management Market Overview by Deployment Type

- Egyptian Telecom Expense Management Market Overview by Company Type

- Egyptian Telecom Expense Management Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Telecom Expense Management Market Overview by Solution Type

- Saudi Arabian Telecom Expense Management Market Overview by Service Type

- Saudi Arabian Telecom Expense Management Market Overview by Deployment Type

- Saudi Arabian Telecom Expense Management Market Overview by Company Type

- Saudi Arabian Telecom Expense Management Market Overview by Industry Sector

- MOROCCO

- Moroccan Telecom Expense Management Market Overview by Solution Type

- Moroccan Telecom Expense Management Market Overview by Service Type

- Moroccan Telecom Expense Management Market Overview by Deployment Type

- Moroccan Telecom Expense Management Market Overview by Company Type

- Moroccan Telecom Expense Management Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Telecom Expense Management Market Overview by Solution Type

- Kuwaiti Telecom Expense Management Market Overview by Service Type

- Kuwaiti Telecom Expense Management Market Overview by Deployment Type

- Kuwaiti Telecom Expense Management Market Overview by Company Type

- Kuwaiti Telecom Expense Management Market Overview by Industry Sector

- QATAR

- Qatari Telecom Expense Management Market Overview by Solution Type

- Qatari Telecom Expense Management Market Overview by Service Type

- Qatari Telecom Expense Management Market Overview by Deployment Type

- Qatari Telecom Expense Management Market Overview by Company Type

- Qatari Telecom Expense Management Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Telecom Expense Management Market Overview by Solution Type

- Rest of Middle East & Africa Telecom Expense Management Market Overview by Service Type

- Rest of Middle East & Africa Telecom Expense Management Market Overview by Deployment Type

- Rest of Middle East & Africa Telecom Expense Management Market Overview by Company Type

- Rest of Middle East & Africa Telecom Expense Management Market Overview by Industry Sector

PART C: INDUSTRY GUIDE

PART D: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

Accenture

Anatole

Avotus

Brightfin

Calero-MDSL

Cass Information Systems

CGI Inc.

Cimpl

Comview

Dimension Data (NTT Communications)

Econocom

Habble

ICOMM

Mindglobal

NTT Limited

One Source Communications

RadiusPoint

Sakon

Tangoe

TeleManagement Technologies, Inc.

Telesoft

Tellennium

Upland Software (Cimpl)

Valicom

Vodafone Group Plc

VoicePlus

WidePoint

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |