Global Storage Area Network (SAN) Hardware Market - Technologies and Applications

- Published: Aug 2025

- Pages: 470 | Charts: 405

- Report Code: ITM102

SHARE THIS REPORT:

Global Storage Area Network (SAN) Hardware Market Trends and Outlook

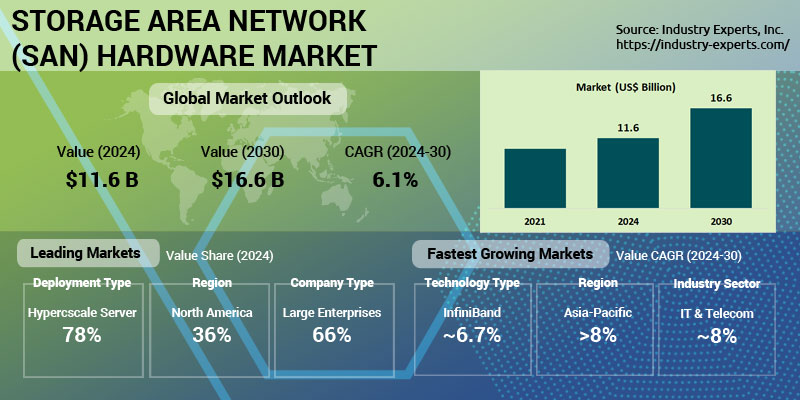

The global Storage Area Network (SAN) hardware market reached approximately US$11.6 billion in 2024 and is projected to exceed US$16.6 billion by 2030, expanding at a CAGR of 6.1%. Growth is being propelled by relentless enterprise data expansion, ultra-low-latency workload requirements, and the transition to flash-optimized and NVMe-over-Fabrics (NVMe-oF) architectures. As digital transformation and compliance pressures intensify across industries, SAN hardware remains essential infrastructure for mission-critical environments, especially in sectors like banking, telecom, and healthcare.

While traditional Fiber Channel-based systems still dominate, the market is rapidly evolving. Vendors are introducing NVMe-ready arrays, high-speed HBAs, and software-defined SAN components to address the increasing performance demands of AI, big data, and cloud-native workloads. Regional momentum is shifting as well, North America remains the largest market, supported by enterprise refresh cycles and hyperscale investments, while Asia-Pacific is the fastest-growing, fueled by cloud-first strategies, fintech expansion, and infrastructure modernization in China, India, and Southeast Asia.

Leading players in this market include Dell Technologies, Hewlett Packard Enterprise (HPE), IBM, NetApp, Cisco, Pure Storage, and Huawei. These vendors are expanding their SAN portfolios with software-defined overlays, NVMe support, and modular deployment models to remain competitive in a market shaped by hyperscale disaggregation and evolving enterprise demands.

Storage Area Network (SAN) Hardware Regional Market Analysis

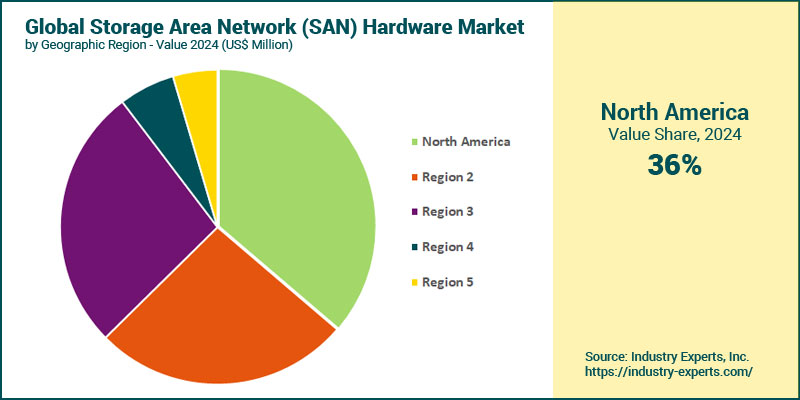

In 2024, North America is leading all regions at 36.3% of total global SAN hardware market. This dominance is driven by entrenched Fiber Channel infrastructure, hyperscale cloud deployments, and regulatory-heavy verticals such as financial services and healthcare. Europe followed, benefiting from ongoing refresh cycles and growing adoption of software-defined SAN overlays, particularly in the public and industrial sectors. The Asia-Pacific region is poised to be the fastest-growing market, expanding at a CAGR of 8.1% to exceed US$5 billion by 2030. This rapid growth is underpinned by increasing hyperscale investments, cloud-first enterprise strategies in China and India, and broader adoption of NVMe-over-Fabrics among fintech and digital-native organizations.

Storage Area Network (SAN) Hardware Market Analysis by Technology

As of 2024, Fiber Channel switches were the largest technology segment, cornering nearly 41.4% of global SAN hardware revenues. This dominance is anchored in mature markets such as North America and Europe, where enterprises, particularly in government, healthcare, and financial services, continue to favor Fiber Channel for its reliability, low-latency performance, and robust security. Fiber Channel Over Ethernet (FCoE) followed closely, reflecting steady upgrades from 16 Gbps to 64 Gbps as throughput demands intensify. Looking forward, InfiniBand is expected to be the fastest-growing technology, expanding at a CAGR of 6.7%. This growth is being driven by its increasing deployment in AI and high-performance computing (HPC) environments, where ultra-low-latency and high-bandwidth interconnects are critical. The second-fastest growing segment is Fiber Channel switches, sustained by refresh cycles and hybrid SAN adoption across regulated industries.

Storage Area Network (SAN) Hardware Market Analysis by Deployment Type

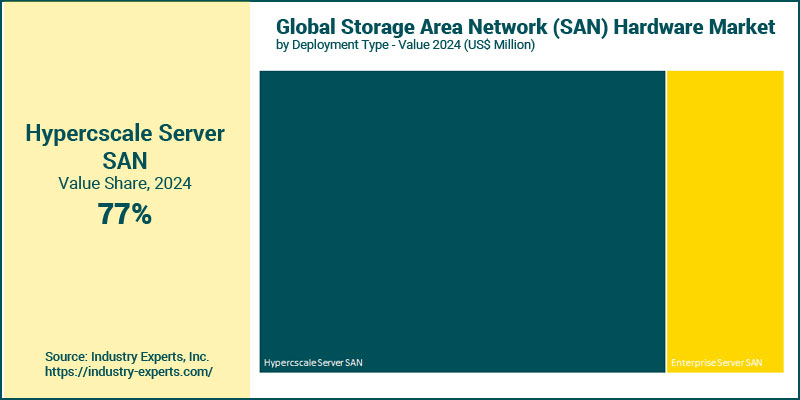

Hyperscale deployments dominated the global SAN hardware market, generating approximately 77.5% of total revenues in 2024. This overwhelming share is fueled by hyperscalers' relentless investments in disaggregated infrastructure, flash-optimized NVMe systems, and proprietary orchestration software. Large-scale cloud providers continue to prioritize modular, performance-optimized SAN hardware to support AI/ML workloads and petabyte-scale data pipelines. In contrast, the enterprise segment, though smaller in 2024, is projected to be the fastest-growing, expanding at a CAGR of 7.1%. Growth is being driven by digital transformation initiatives in sectors such as healthcare, banking, manufacturing, and government, where storage compliance, high availability, and operational continuity are critical. Enterprises are increasingly embracing hybrid SAN configurations, blending on-prem performance with cloud agility via software-defined overlays.

Storage Area Network (SAN) Hardware Market Analysis by Company Type

In 2024, large enterprises represented the largest end-user category, contributing around 66% of global SAN hardware revenues. These organizations, often operating across highly regulated and data-intensive verticals such as banking, telecom, and healthcare, continue to invest heavily in robust SAN infrastructure to support critical workloads, ensure compliance, and maintain operational resilience. Their requirements typically include deterministic performance, advanced Fiber Channel connectivity, and pre-validated hardware-software stacks. However, small and midsized enterprises (SMEs) are projected to be the fastest-growing customer segment, expanding at a CAGR of 7.1%. This growth reflects increasing SAN adoption by digitally maturing SMEs in Asia-Pacific, Latin America, and Eastern Europe, many of whom are turning to modular, cost-effective SAN setups that support cloud-native integration and remote scalability. As these companies modernize IT infrastructure, demand is rising for NVMe-powered arrays, Ethernet-based iSCSI SANs, and software-defined storage compatibility.

Storage Area Network (SAN) Hardware Market Analysis by Industry Sector

The banking, financial services, and insurance (BFSI) sector led global SAN hardware spending, generating 21.5% of total market revenue in 2024. This dominance is driven by the sector's stringent regulatory mandates, need for auditability, and demand for deterministic performance, especially for transaction-heavy systems and risk analytics workloads. Financial institutions are at the forefront of Fiber Channel upgrades and NVMe-over-Fabrics deployment to meet real-time data access needs. The IT & telecom sector was the second largest segment in 2024, reflecting high SAN hardware consumption by data center operators, managed service providers, and cloud infrastructure vendors. However, it is also poised to be the fastest-growing industry sector, expanding at a CAGR of 7.8%. This acceleration is fueled by edge expansion, 5G rollouts, and the increasing use of AI-native applications across telecom infrastructure, all of which require scalable, high-throughput storage systems.

Storage Area Network (SAN) Hardware Market Report Scope

This global report on Storage Area Network (SAN) Hardware market analyzes the global and regional market based on Technology, Deployment Type, Company Type and Industry Sector for the period 2021-2030 with forecasts from 2024 to 2030 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Historical Period: | 2021-2024 | |

| Base Year: | 2024 | |

| Forecast Period: | 2024-2030 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 20+ |

Storage Area Network (SAN) Hardware Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Storage Area Network (SAN) Hardware Market by Technology

- Fiber Channel (FC)

- Fiber Channel Over Ethernet (FCoE)

- InfiniBand

- iSCSI Protocol

Storage Area Network (SAN) Hardware Market by Deployment Type

- Hypercscale Server SAN

- Enterprise Server SAN

Storage Area Network (SAN) Hardware Market by Company Type

- Large Enterprises

- SMEs

Storage Area Network (SAN) Hardware Market by Industry Sector

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

Storage Area Network (SAN) Hardware Market Frequently Asked Questions (FAQs)

The market is valued at approximately US$11.6 billion in 2024, with strong demand from enterprise data centers and hyperscale environments.

North America leads with about 36.3% share in 2024, driven by financial services, healthcare, and hyperscale deployments.

Asia-Pacific is the fastest-growing region, with a CAGR of 8.1%, propelled by cloud-first initiatives and infrastructure modernization.

Fibre Channel switches are the largest technology segment, generating US$4.8 billion in 2024, favored for low-latency and secure performance.

InfiniBand is growing fastest at 6.7% CAGR, supported by HPC and AI workloads that require high throughput and low latency.

Key players include Dell Technologies, HPE, IBM, NetApp, Cisco, Pure Storage, and Huawei, each offering advanced, scalable SAN solutions.

Enterprises seek regulatory compliance, performance consistency, and hybrid configurations, while hyperscalers focus on disaggregated hardware and orchestration flexibility.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Storage Area Network (SAN) Hardware

- Market Segmentation for Storage Area Network (SAN) Hardware

- Technologies

- Deployment Types

- Company Types

- Industry Sectors

- Key Trends in Storage Area Network (SAN) Hardware Market

2. INDUSTRY LANDSCAPE

- Global Storage Area Network (SAN) Hardware Market Outlook

- Comprehensive Storage Area Network (SAN) Hardware Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Storage Area Network (SAN) Hardware Industry

- Startup Strategies for Storage Area Network (SAN) Hardware Industry

- SWOT Analysis of Storage Area Network (SAN) Hardware Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Storage Area Network (SAN) Hardware Companies

- Market Share Analysis of Storage Area Network (SAN) Hardware Companies

- SWOT Analysis of Key Players in the Storage Area Network (SAN) Hardware Industry

- Key Market Players

- Cisco

- Dell Technologies (Dell EMC)

- Dell VxRail

- Fujitsu

- Hewlett Packard Enterprise (HPE)

- Hitachi Vantara

- HPE SimpliVity

- Huawei

- IBM

- Infortrend

- Lenovo

- NEC

- NetApp

- Nutanix

- Oracle

- Pure Storage

- Quantum

- Seagate

- Tintri (DDN)

- Western Digital

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Storage Area Network (SAN) Hardware Market Overview by Technology

- Storage Area Network (SAN) Hardware Technology Market Overview by Global Region

- Fiber Channel (FC)

- Fiber Channel Over Ethernet (FCoE)

- InfiniBand

- iSCSI Protocol

- Global Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Storage Area Network (SAN) Hardware Deployment Type Market Overview by Global Region

- Hypercscale Server SAN

- Enterprise Server SAN

- Global Storage Area Network (SAN) Hardware Market Overview by Company Type

- Storage Area Network (SAN) Hardware Company Type Market Overview by Global Region

- Large Enterprises

- SMEs

- Global Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- Storage Area Network (SAN) Hardware Industry Sector Market Overview by Global Region

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

PART B: REGIONAL MARKET PERSPECTIVE

- Global Storage Area Network (SAN) Hardware Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Storage Area Network (SAN) Hardware Market Overview by Geographic Region

- North American Storage Area Network (SAN) Hardware Market Overview by Technology

- North American Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- North American Storage Area Network (SAN) Hardware Market Overview by Company Type

- North American Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- Country-wise Analysis of North American Storage Area Network (SAN) Hardware Market

- THE UNITED STATES

- United States Storage Area Network (SAN) Hardware Market Overview by Technology

- United States Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- United States Storage Area Network (SAN) Hardware Market Overview by Company Type

- United States Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- CANADA

- Canadian Storage Area Network (SAN) Hardware Market Overview by Technology

- Canadian Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Canadian Storage Area Network (SAN) Hardware Market Overview by Company Type

- Canadian Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- MEXICO

- Mexican Storage Area Network (SAN) Hardware Market Overview by Technology

- Mexican Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Mexican Storage Area Network (SAN) Hardware Market Overview by Company Type

- Mexican Storage Area Network (SAN) Hardware Market Overview by Industry Sector

7. EUROPE

- European Storage Area Network (SAN) Hardware Market Overview by Geographic Region

- European Storage Area Network (SAN) Hardware Market Overview by Technology

- European Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- European Storage Area Network (SAN) Hardware Market Overview by Company Type

- European Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- Country-wise Analysis of European Storage Area Network (SAN) Hardware Market

- GERMANY

- German Storage Area Network (SAN) Hardware Market Overview by Technology

- German Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- German Storage Area Network (SAN) Hardware Market Overview by Company Type

- German Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Storage Area Network (SAN) Hardware Market Overview by Technology

- United Kingdom Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- United Kingdom Storage Area Network (SAN) Hardware Market Overview by Company Type

- United Kingdom Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- FRANCE

- French Storage Area Network (SAN) Hardware Market Overview by Technology

- French Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- French Storage Area Network (SAN) Hardware Market Overview by Company Type

- French Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- ITALY

- Italian Storage Area Network (SAN) Hardware Market Overview by Technology

- Italian Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Italian Storage Area Network (SAN) Hardware Market Overview by Company Type

- Italian Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Storage Area Network (SAN) Hardware Market Overview by Technology

- Dutch Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Dutch Storage Area Network (SAN) Hardware Market Overview by Company Type

- Dutch Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- SPAIN

- Spanish Storage Area Network (SAN) Hardware Market Overview by Technology

- Spanish Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Spanish Storage Area Network (SAN) Hardware Market Overview by Company Type

- Spanish Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- RUSSIA

- Russian Storage Area Network (SAN) Hardware Market Overview by Technology

- Russian Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Russian Storage Area Network (SAN) Hardware Market Overview by Company Type

- Russian Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- SWITZERLAND

- Swiss Storage Area Network (SAN) Hardware Market Overview by Technology

- Swiss Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Swiss Storage Area Network (SAN) Hardware Market Overview by Company Type

- Swiss Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Storage Area Network (SAN) Hardware Market Overview by Technology

- Rest of Europe Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Rest of Europe Storage Area Network (SAN) Hardware Market Overview by Company Type

- Rest of Europe Storage Area Network (SAN) Hardware Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Storage Area Network (SAN) Hardware Market Overview by Geographic Region

- Asia-Pacific Storage Area Network (SAN) Hardware Market Overview by Technology

- Asia-Pacific Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Asia-Pacific Storage Area Network (SAN) Hardware Market Overview by Company Type

- Asia-Pacific Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Storage Area Network (SAN) Hardware Market

- CHINA

- Chinese Storage Area Network (SAN) Hardware Market Overview by Technology

- Chinese Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Chinese Storage Area Network (SAN) Hardware Market Overview by Company Type

- Chinese Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- JAPAN

- Japanese Storage Area Network (SAN) Hardware Market Overview by Technology

- Japanese Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Japanese Storage Area Network (SAN) Hardware Market Overview by Company Type

- Japanese Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- INDIA

- Indian Storage Area Network (SAN) Hardware Market Overview by Technology

- Indian Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Indian Storage Area Network (SAN) Hardware Market Overview by Company Type

- Indian Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- AUSTRALIA

- Australia Storage Area Network (SAN) Hardware Market Overview by Technology

- Australia Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Australia Storage Area Network (SAN) Hardware Market Overview by Company Type

- Australia Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- SINGAPORE

- Singaporean Storage Area Network (SAN) Hardware Market Overview by Technology

- Singaporean Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Singaporean Storage Area Network (SAN) Hardware Market Overview by Company Type

- Singaporean Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Storage Area Network (SAN) Hardware Market Overview by Technology

- South Korean Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- South Korean Storage Area Network (SAN) Hardware Market Overview by Company Type

- South Korean Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Storage Area Network (SAN) Hardware Market Overview by Technology

- Rest of Asia-Pacific Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Rest of Asia-Pacific Storage Area Network (SAN) Hardware Market Overview by Company Type

- Rest of Asia-Pacific Storage Area Network (SAN) Hardware Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Storage Area Network (SAN) Hardware Market Overview by Geographic Region

- South American Storage Area Network (SAN) Hardware Market Overview by Technology

- South American Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- South American Storage Area Network (SAN) Hardware Market Overview by Company Type

- South American Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- Country-wise Analysis of South American Storage Area Network (SAN) Hardware Market

- BRAZIL

- Brazilian Storage Area Network (SAN) Hardware Market Overview by Technology

- Brazilian Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Brazilian Storage Area Network (SAN) Hardware Market Overview by Company Type

- Brazilian Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- ARGENTINA

- Argentine Storage Area Network (SAN) Hardware Market Overview by Technology

- Argentine Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Argentine Storage Area Network (SAN) Hardware Market Overview by Company Type

- Argentine Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- COLOMBIA

- Colombian Storage Area Network (SAN) Hardware Market Overview by Technology

- Colombian Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Colombian Storage Area Network (SAN) Hardware Market Overview by Company Type

- Colombian Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- CHILE

- Chilean Storage Area Network (SAN) Hardware Market Overview by Technology

- Chilean Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Chilean Storage Area Network (SAN) Hardware Market Overview by Company Type

- Chilean Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- PERU

- Peruvian Storage Area Network (SAN) Hardware Market Overview by Technology

- Peruvian Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Peruvian Storage Area Network (SAN) Hardware Market Overview by Company Type

- Peruvian Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Storage Area Network (SAN) Hardware Market Overview by Technology

- Rest of South America Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Rest of South America Storage Area Network (SAN) Hardware Market Overview by Company Type

- Rest of South America Storage Area Network (SAN) Hardware Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Storage Area Network (SAN) Hardware Market Overview by Geographic Region

- Middle East & Africa Storage Area Network (SAN) Hardware Market Overview by Technology

- Middle East & Africa Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Middle East & Africa Storage Area Network (SAN) Hardware Market Overview by Company Type

- Middle East & Africa Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Storage Area Network (SAN) Hardware Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Storage Area Network (SAN) Hardware Market Overview by Technology

- United Arab Emirates Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- United Arab Emirates Storage Area Network (SAN) Hardware Market Overview by Company Type

- United Arab Emirates Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- SOUTH AFRICA

- South African Storage Area Network (SAN) Hardware Market Overview by Technology

- South African Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- South African Storage Area Network (SAN) Hardware Market Overview by Company Type

- South African Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- EGYPT

- Egyptian Storage Area Network (SAN) Hardware Market Overview by Technology

- Egyptian Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Egyptian Storage Area Network (SAN) Hardware Market Overview by Company Type

- Egyptian Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Storage Area Network (SAN) Hardware Market Overview by Technology

- Saudi Arabian Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Saudi Arabian Storage Area Network (SAN) Hardware Market Overview by Company Type

- Saudi Arabian Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- MOROCCO

- Moroccan Storage Area Network (SAN) Hardware Market Overview by Technology

- Moroccan Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Moroccan Storage Area Network (SAN) Hardware Market Overview by Company Type

- Moroccan Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Storage Area Network (SAN) Hardware Market Overview by Technology

- Kuwaiti Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Kuwaiti Storage Area Network (SAN) Hardware Market Overview by Company Type

- Kuwaiti Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- QATAR

- Qatari Storage Area Network (SAN) Hardware Market Overview by Technology

- Qatari Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Qatari Storage Area Network (SAN) Hardware Market Overview by Company Type

- Qatari Storage Area Network (SAN) Hardware Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Storage Area Network (SAN) Hardware Market Overview by Technology

- Rest of Middle East & Africa Storage Area Network (SAN) Hardware Market Overview by Deployment Type

- Rest of Middle East & Africa Storage Area Network (SAN) Hardware Market Overview by Company Type

- Rest of Middle East & Africa Storage Area Network (SAN) Hardware Market Overview by Industry Sector

PART C: INDUSTRY GUIDE

PART D: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

Cisco

Dell Technologies (Dell EMC)

Dell VxRail

Fujitsu

Hewlett Packard Enterprise (HPE)

Hitachi Vantara

HPE SimpliVity

Huawei

IBM

Infortrend

Lenovo

NEC

NetApp

Nutanix

Oracle

Pure Storage

Quantum

Seagate

Tintri (DDN)

Western Digital

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |