Software-as-a-Service (SaaS) - A Global Market Overview

- Published: Aug 2025

- Pages: 580 | Charts: 494

- Report Code: ITM026

SHARE THIS REPORT:

Global Software-as-a-Service (SaaS) Market Trends and Outlook

The global Software-as-a-Service (SaaS) market is experiencing explosive growth as enterprises accelerate digital transformation and shift toward flexible, subscription-based models. With a projected increase from US$281.8 billion in 2024 to US$774.3 billion by 2030 at a CAGR of 18.3%, SaaS is reshaping how businesses access and deploy software across verticals. Key factors fueling this surge include the migration of legacy workloads to the cloud, the proliferation of low-code/no-code tools, and the embedding of AI and analytics into business workflows. SaaS enables rapid scalability, seamless updates, and cost-efficiency, making it a core element of enterprise modernization strategies. Moreover, the rise of vertical SaaS and micro-SaaS offerings is providing highly targeted solutions tailored to industry-specific needs.

This momentum is further supported by robust ecosystem developments and evolving deployment models. Hybrid and private SaaS environments are gaining traction among enterprises with complex regulatory or security requirements, while public cloud remains popular for speed and scalability. Small and medium-sized enterprises (SMEs) are increasingly turning to SaaS to reduce IT overhead, supported by pay-as-you-go pricing and simplified onboarding. Integration with APIs, mobile apps, and digital collaboration tools is driving enterprise-wide adoption, particularly in industries such as BFSI, healthcare, and ecommerce. As SaaS platforms become more intelligent and interconnected, the market is poised for sustained growth, driven by innovation, efficiency, and demand for personalized, cloud-native solutions.

Software-as-a-Service (SaaS) Regional Market Analysis

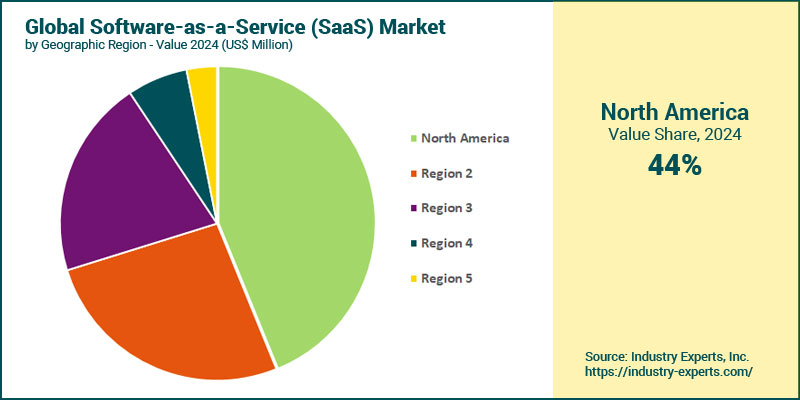

North America maintained its leadership in the global SaaS market, contributing 43.8% of total revenue in 2024, driven by mature cloud ecosystems, early enterprise adoption, and strong digital transformation investments across industries. Europe followed with 26.4%, supported by regulatory compliance needs like GDPR and growing public-sector cloud procurement. Asia Pacific is the fastest-growing region, projected to expand at around 20% CAGR and reach approximately US$176.2 billion by 2030. Growth in the region is fueled by widespread digitalization across SMEs, government-backed transformation initiatives, and increased access to high-speed internet and mobile technologies in emerging economies such as India, Southeast Asia, and China.

Software-as-a-Service (SaaS) Market Analysis by Component

In 2024, software subscriptions dominated the SaaS market, accounting for 83.6% of revenue as businesses rapidly adopted cloud-based CRM, ERP, and productivity platforms for agility and modernization. This component is expected to maintain a stronghold due to recurring license-based models and scalable offerings. Services, including implementation, customization, and managed operations, made up 16.4% but are forecast to grow faster-at a 20.9% CAGR-surpassing US$144 billion by 2030. This growth is attributed to rising demand for expert support around AI integration, data governance, and multi-cloud optimization, reflecting a shift toward holistic digital transformation strategies.

Software-as-a-Service (SaaS) Market Analysis by Deployment Type

Private SaaS deployments held the largest share in 2024 at 44.5%, favored by enterprises in regulated industries requiring strict control, data residency, and customized configurations. Public SaaS followed with a 34.6% share due to its low upfront cost and rapid deployment advantages. Hybrid SaaS accounted for 20.9% and is projected to grow at a 20.1% CAGR, topping US$176.6 billion by 2030. The rise in hybrid adoption is driven by its flexibility in managing workloads across public and private environments, meeting needs for security, performance, and compliance, particularly as edge computing and container orchestration gain traction.

Software-as-a-Service (SaaS) Market Analysis by Company Type

Large enterprises contributed 65.3% of SaaS revenues in 2024, propelled by complex application needs, multi-region deployments, and demand for enterprise-grade features, analytics, and automation. These companies often require private or hybrid deployments for compliance and scalability, thus generating higher per-client revenue. Meanwhile, small and medium-sized enterprises (SMEs) represented 34.7% but are expanding rapidly at a CAGR of 19.7%. Growth in this segment is driven by affordable subscription models, freemium offerings, and the appeal of scalable cloud-based tools for marketing, sales, and operations, especially in emerging markets and tech-forward startups.

Software-as-a-Service (SaaS) Market Analysis by Application

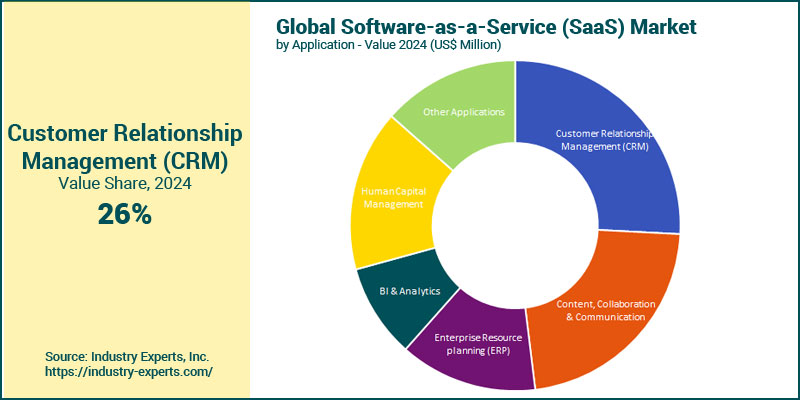

Customer Relationship Management (CRM) remained the largest SaaS application in 2024 with a 25.8% share, underscoring the critical role of customer engagement and sales automation in business growth. CRM adoption is reinforced by centralized access, ease of scaling, and AI-driven personalization. The fastest-growing category is Content, Collaboration & Communication (CCC), projected to grow at a 22.4% CAGR and exceed US$211 billion by 2030, spurred by hybrid work models and the need for real-time, integrated communication tools like Zoom, Slack, and Microsoft Teams. Other rapidly expanding areas include Human Capital Management and BI & Analytics, reflecting growing needs for workforce management and data-driven decision-making.

Software-as-a-Service (SaaS) Market Analysis by Industry Sector

The BFSI sector led the SaaS market in 2024 with a 21.8% share, adopting cloud solutions for digital banking, payments, compliance, and customer experience. Financial institutions rely on SaaS to manage security, scale operations, and comply with evolving regulations. Healthcare is the fastest-growing vertical, expected to register a 23.7% CAGR through 2030, driven by telehealth expansion, EHR modernization, and demand for AI-assisted diagnostics. Additionally, the retail and ecommerce sectors are increasing their SaaS investments to optimize omnichannel engagement, inventory management, and data-driven marketing, solidifying SaaS's role in industry-wide digital transformation.

Software-as-a-Service (SaaS) Market Report Scope

This global report on Software-as-a-Service (SaaS) analyzes the global and regional markets based on Component, Deployment Type, Company Type, Application and Industry Sector for the period 2021-2030 with forecasts from 2024 to 2030 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Historical Period: | 2021-2024 | |

| Base Year: | 2024 | |

| Forecast Period: | 2024-2030 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 30+ |

Software-as-a-Service (SaaS) Market by Geographic Region

- North America (United States, Canada and Mexico)

- Europe (Germany, United Kingdom, France, Italy, Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Software-as-a-Service (SaaS) Market by Component

- Software

- Services

Software-as-a-Service (SaaS) Market by Deployment Type

- Private

- Public

- Hybrid

Software-as-a-Service (SaaS) Market by Company Type

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

Software-as-a-Service (SaaS) Market by Application

- Customer Relationship Management (CRM)

- Content, Collaboration & Communication

- Enterprise Resource planning (ERP)

- BI & Analytics

- Human Capital Management

- Other Applications

Software-as-a-Service (SaaS) Market by Industry Sector

- BFSI

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industries

Software-as-a-Service (SaaS) Market Frequently Asked Questions (FAQs)

The global market for Software-as-a-Service (SaaS) is expected to register a CAGR of 18.3% over the 2024-2030 analysis period.

With an estimated share of 43.8% in 2024, North America forms the largest market for Software-as-a-Service (SaaS).

Asia-Pacific is expected to be the fastest growing region for Software-as-a-Service (SaaS), with a forecast CAGR of 20.5% between 2024 and 2030.

Software commands the largest share of the global Software-as-a-Service (SaaS) market, estimated at 83.6% in 2024.

Content, Collaboration & Communication is anticipated to be the fastest growing application for Software-as-a-Service (SaaS), with a projected 2024-2030 CAGR of 22.4%.

The demand for Software-as-a-Service (SaaS) is being driven by a number of factors, including cost-effectiveness & scalability, accessibility & convenience, focus on core business, rapid deployment & time-to-value, increased integration & ecosystems, innovation & specialization (such as Micro-SaaS & Vertical SaaS), data-driven insights, emergence of AI & machine learning and strong customer success focus.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Software-as-a-Service (SaaS)

- Software-as-a-Service (SaaS) Based on Component

- Software-as-a-Service (SaaS) Based on Deployment Type

- Software-as-a-Service (SaaS) Based on Company Type

- Software-as-a-Service (SaaS) Based on Application

- Software-as-a-Service (SaaS) Based on Industry Sector

2. INDUSTRY LANDSCAPE

- Global Software-as-a-Service (SaaS) Market Outlook

- Growth Drivers of Software-as-a-Service (SaaS) Market

- Challenges Inhibiting Software-as-a-Service (SaaS) Market Growth and Mitigating Strategies

- How Software-as-a-Service (SaaS) is Being Adopted by Industry

- Software-as-a-Service (SaaS) Industry � SWOT Analysis

- Strengths

- Weaknesses

- Opportunities

- Threats

- Strategic Software-as-a-Service (SaaS) Industry Analysis

- Porter's Five Forces Analysis

- PESTEL Analysis

- Market Entry & Startup Strategies for Software-as-a-Service (SaaS) Market

- Market Entry Strategies

- Startup Trends

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Software-as-a-Service (SaaS) Companies

- Market Share Analysis of Software-as-a-Service (SaaS)

- Pricing Analysis of Software-as-a-Service (SaaS)

- An Exhaustive Analysis of Software-as-a-Service (SaaS) in Untapped Markets

- Key Market Players

- Adobe Inc.

- Alibaba Cloud International

- Atlassian Corporation

- Babbel

- Box, Inc.

- Cisco Systems, Inc.

- Citrix Systems, Inc.

- Google LLC

- HPE

- HubSpot, Inc.

- IBM Corporation

- Infosys

- Intuit Inc.

- IONOS Cloud Inc.

- Microsoft Corporation

- NetSuite Inc.

- Oracle Corporation

- Rackspace Technology, Inc.

- Sage Group plc

- Salesforce, Inc.

- SAP SE

- ServiceNow

- Shopify Inc.

- Slack Technologies, LLC

- TCS

- Tecent Holdings

- Trend Micro

- VMware Inc.

- Workday, Inc.

- Workiva

- Zendesk, Inc.

- Zoho Corporation

- Zoom Video Communications, Inc.

4. KEY BUSINESS & PRODUCT TRENDS

- Important Recent Industry Activity

- Recent Major Product Launches by the Market Leaders

5. GLOBAL MARKET OVERVIEW

- Global Software-as-a-Service (SaaS) Market Overview by Component

- Software-as-a-Service (SaaS) Component Market Overview by Global Region

- Software

- Services

- Global Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Software-as-a-Service (SaaS) Deployment Type Market Overview by Global Region

- Private

- Public

- Hybrid

- Global Software-as-a-Service (SaaS) Market Overview by Company Type

- Software-as-a-Service (SaaS) Company Type Market Overview by Global Region

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

- Global Software-as-a-Service (SaaS) Market Overview by Application

- Software-as-a-Service (SaaS) Application Market Overview by Global Region

- Customer Relationship Management (CRM)

- Content, Collaboration & Communication

- Enterprise Resource planning (ERP)

- BI & Analytics

- Human Capital Management

- Other Applications

- Global Software-as-a-Service (SaaS) Market Overview by Industry Sector

- Software-as-a-Service (SaaS) Industry Sector Market Overview by Global Region

- BFSI (Banking, Financial Services, Insurance)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Others

PART B: REGIONAL MARKET PERSPECTIVE

- Global Software-as-a-Service (SaaS) Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Software-as-a-Service (SaaS) Market Overview by Geographic Region

- North American Software-as-a-Service (SaaS) Market Overview by Component

- North American Software-as-a-Service (SaaS) Market Overview by Deployment Type

- North American Software-as-a-Service (SaaS) Market Overview by Company Type

- North American Software-as-a-Service (SaaS) Market Overview by Application

- North American Software-as-a-Service (SaaS) Market Overview by Industry Sector

- Country-wise Analysis of North American Software-as-a-Service (SaaS) Market

- THE UNITED STATES

- United States Software-as-a-Service (SaaS) Market Overview by Component

- United States Software-as-a-Service (SaaS) Market Overview by Deployment

- United States Software-as-a-Service (SaaS) Market Overview by Company Type

- United States Software-as-a-Service (SaaS) Market Overview by Application

- United States Software-as-a-Service (SaaS) Market Overview by Industry Sector

- CANADA

- Canadian Software-as-a-Service (SaaS) Market Overview by Component

- Canadian Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Canadian Software-as-a-Service (SaaS) Market Overview by Company Type

- Canadian Software-as-a-Service (SaaS) Market Overview by Application

- Canadian Software-as-a-Service (SaaS) Market Overview by Industry Sector

- MEXICO

- Mexican Software-as-a-Service (SaaS) Market Overview by Component

- Mexican Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Mexican Software-as-a-Service (SaaS) Market Overview by Company Type

- Mexican Software-as-a-Service (SaaS) Market Overview by Application

- Mexican Software-as-a-Service (SaaS) Market Overview by Industry Sector

7. EUROPE

- European Software-as-a-Service (SaaS) Market Overview by Geographic Region

- European Software-as-a-Service (SaaS) Market Overview by Component

- Europea Software-as-a-Service (SaaS) Market Overview by Deployment Type

- European Software-as-a-Service (SaaS) Market Overview by Company Type

- European Software-as-a-Service (SaaS) Market Overview by Application

- European Software-as-a-Service (SaaS) Market Overview by Industry Sector

- Country-wise Analysis of European Software-as-a-Service (SaaS) Market

- GERMANY

- German Software-as-a-Service (SaaS) Market Overview by Component

- German Software-as-a-Service (SaaS) Market Overview by Deployment Type

- German Software-as-a-Service (SaaS) Market Overview by Company Type

- German Software-as-a-Service (SaaS) Market Overview by Application

- German Software-as-a-Service (SaaS) Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Software-as-a-Service (SaaS) Market Overview by Component

- United Kingdom Software-as-a-Service (SaaS) Market Overview by Deployment Type

- United Kingdom Software-as-a-Service (SaaS) Market Overview by Company Type

- United Kingdom Software-as-a-Service (SaaS) Market Overview by Application

- United Kingdom Software-as-a-Service (SaaS) Market Overview by Industry Sector

- FRANCE

- French Software-as-a-Service (SaaS) Market Overview by Component

- French Software-as-a-Service (SaaS) Market Overview by Deployment Type

- French Software-as-a-Service (SaaS) Market Overview by Company Type

- French Software-as-a-Service (SaaS) Market Overview by Application

- French Software-as-a-Service (SaaS) Market Overview by Industry Sector

- ITALY

- Italian Software-as-a-Service (SaaS) Market Overview by Component

- Italian Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Italian Software-as-a-Service (SaaS) Market Overview by Company Type

- Italian Software-as-a-Service (SaaS) Market Overview by Application

- Italian Software-as-a-Service (SaaS) Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Software-as-a-Service (SaaS) Market Overview by Component

- Dutch Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Dutch Software-as-a-Service (SaaS) Market Overview by Company Type

- Dutch Software-as-a-Service (SaaS) Market Overview by Application

- Dutch Software-as-a-Service (SaaS) Market Overview by Industry Sector

- SPAIN

- Spanish Software-as-a-Service (SaaS) Market Overview by Component

- Spanish Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Spanish Software-as-a-Service (SaaS) Market Overview by Company Type

- Spanish Software-as-a-Service (SaaS) Market Overview by Application

- Spanish Software-as-a-Service (SaaS) Market Overview by Industry Sector

- RUSSIA

- Russian Software-as-a-Service (SaaS) Market Overview by Component

- Russian Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Russian Software-as-a-Service (SaaS) Market Overview by Company Type

- Russian Software-as-a-Service (SaaS) Market Overview by Application

- Russian Software-as-a-Service (SaaS) Market Overview by Industry Sector

- SWITZERLAND

- Swiss Software-as-a-Service (SaaS) Market Overview by Component

- Swiss Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Swiss Software-as-a-Service (SaaS) Market Overview by Company Type

- Swiss Software-as-a-Service (SaaS) Market Overview by Application

- Swiss Software-as-a-Service (SaaS) Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Software-as-a-Service (SaaS) Market Overview by Component

- Rest of Europe Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Rest of Europe Software-as-a-Service (SaaS) Market Overview by Company Type

- Rest of Europe Software-as-a-Service (SaaS) Market Overview by Application

- Rest of Europe Software-as-a-Service (SaaS) Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Software-as-a-Service (SaaS) Market Overview by Geographic Region

- Asia-Pacific Software-as-a-Service (SaaS) Market Overview by Component

- Asia-Pacific Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Asia-Pacific Software-as-a-Service (SaaS) Market Overview by Company Type

- Asia-Pacific Software-as-a-Service (SaaS) Market Overview by Application

- Asia-Pacific Software-as-a-Service (SaaS) Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Software-as-a-Service (SaaS) Market

- CHINA

- Chinese Software-as-a-Service (SaaS) Market Overview by Component

- Chinese Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Chinese Software-as-a-Service (SaaS) Market Overview by Company Type

- Chinese Software-as-a-Service (SaaS) Market Overview by Application

- Chinese Software-as-a-Service (SaaS) Market Overview by Industry Sector

- JAPAN

- Japanese Software-as-a-Service (SaaS) Market Overview by Component

- Japanese Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Japanese Software-as-a-Service (SaaS) Market Overview by Company Type

- Japanese Software-as-a-Service (SaaS) Market Overview by Application

- Japanese Software-as-a-Service (SaaS) Market Overview by Industry Sector

- INDIA

- Indian Software-as-a-Service (SaaS) Market Overview by Component

- Indian Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Indian Software-as-a-Service (SaaS) Market Overview by Company Type

- Indian Software-as-a-Service (SaaS) Market Overview by Application

- Indian Software-as-a-Service (SaaS) Market Overview by Industry Sector

- AUSTRALIA

- Australian Software-as-a-Service (SaaS) Market Overview by Component

- Australian Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Australian Software-as-a-Service (SaaS) Market Overview by Company Type

- Australian Software-as-a-Service (SaaS) Market Overview by Application

- Australian Software-as-a-Service (SaaS) Market Overview by Industry Sector

- SINGAPORE

- Singaporean Software-as-a-Service (SaaS) Market Overview by Component

- Singaporean Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Singaporean Software-as-a-Service (SaaS) Market Overview by Company Type

- Singaporean Software-as-a-Service (SaaS) Market Overview by Application

- Singaporean Software-as-a-Service (SaaS) Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Software-as-a-Service (SaaS) Market Overview by Component

- South Korean Software-as-a-Service (SaaS) Market Overview by Deployment Type

- South Korean Software-as-a-Service (SaaS) Market Overview by Company Type

- South Korean Software-as-a-Service (SaaS) Market Overview by Application

- South Korean Software-as-a-Service (SaaS) Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Software-as-a-Service (SaaS) Market Overview by Component

- Rest of Asia-Pacific Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Rest of Asia-Pacific Software-as-a-Service (SaaS) Market Overview by Company Type

- Rest of Asia-Pacific Software-as-a-Service (SaaS) Market Overview by Application

- Rest of Asia-Pacific Software-as-a-Service (SaaS) Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Software-as-a-Service (SaaS) Market Overview by Geographic Region

- South American Software-as-a-Service (SaaS) Market Overview by Component

- South American Software-as-a-Service (SaaS) Market Overview by Deployment Type

- South American Software-as-a-Service (SaaS) Market Overview by Company Type

- South American Software-as-a-Service (SaaS) Market Overview by Application

- South American Software-as-a-Service (SaaS) Market Overview by Industry Sector

- Country-wise Analysis of South American Software-as-a-Service (SaaS) Market

- BRAZIL

- Brazilian Software-as-a-Service (SaaS) Market Overview by Component

- Brazilian Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Brazilian Software-as-a-Service (SaaS) Market Overview by Company Type

- Brazilian Software-as-a-Service (SaaS) Market Overview by Application

- Brazilian Software-as-a-Service (SaaS) Market Overview by Industry Sector

- ARGENTINA

- Argentine Software-as-a-Service (SaaS) Market Overview by Component

- Argentine Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Argentine Software-as-a-Service (SaaS) Market Overview by Company Type

- Argentine Software-as-a-Service (SaaS) Market Overview by Application

- Argentine Software-as-a-Service (SaaS) Market Overview by Industry Sector

- COLOMBIA

- Colombian Software-as-a-Service (SaaS) Market Overview by Component

- Colombian Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Colombian Software-as-a-Service (SaaS) Market Overview by Company Type

- Colombian Software-as-a-Service (SaaS) Market Overview by Application

- Colombian Software-as-a-Service (SaaS) Market Overview by Industry Sector

- CHILE

- Chilean Software-as-a-Service (SaaS) Market Overview by Component

- Chilean Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Chilean Software-as-a-Service (SaaS) Market Overview by Company Type

- Chilean Software-as-a-Service (SaaS) Market Overview by Application

- Chilean Software-as-a-Service (SaaS) Market Overview by Industry Sector

- PERU

- Peruvian Software-as-a-Service (SaaS) Market Overview by Component

- Peruvian Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Peruvian Software-as-a-Service (SaaS) Market Overview by Company Type

- Peruvian Software-as-a-Service (SaaS) Market Overview by Application

- Peruvian Software-as-a-Service (SaaS) Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Software-as-a-Service (SaaS) Market Overview by Component

- Rest of South America Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Rest of South America Software-as-a-Service (SaaS) Market Overview by Company Type

- Rest of South America Software-as-a-Service (SaaS) Market Overview by Application

- Rest of South America Software-as-a-Service (SaaS) Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Software-as-a-Service (SaaS) Market Overview by Geographic Region

- Middle East & Africa Software-as-a-Service (SaaS) Market Overview by Component

- Middle East & Africa Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Middle East & Africa Software-as-a-Service (SaaS) Market Overview by Company Type

- Middle East & Africa Software-as-a-Service (SaaS) Market Overview by Application

- Middle East & Africa Software-as-a-Service (SaaS) Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Software-as-a-Service (SaaS) Market

- UNITED ARAB EMIRATES

- United Arab Emirates Software-as-a-Service (SaaS) Market Overview by Component

- United Arab Emirates Software-as-a-Service (SaaS) Market Overview by Deployment Type

- United Arab Emirates Software-as-a-Service (SaaS) Market Overview by Company Type

- United Arab Emirates Software-as-a-Service (SaaS) Market Overview by Application

- United Arab Emirates Software-as-a-Service (SaaS) Market Overview by Industry Sector

- SOUTH AFRICA

- South African Software-as-a-Service (SaaS) Market Overview by Component

- South African Software-as-a-Service (SaaS) Market Overview by Deployment Type

- South African Software-as-a-Service (SaaS) Market Overview by Company Type

- South African Software-as-a-Service (SaaS) Market Overview by Application

- South African Software-as-a-Service (SaaS) Market Overview by Industry Sector

- EGYPT

- Egyptian Software-as-a-Service (SaaS) Market Overview by Component

- Egyptian Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Egyptian Software-as-a-Service (SaaS) Market Overview by Company Type

- Egyptian Software-as-a-Service (SaaS) Market Overview by Application

- Egyptian Software-as-a-Service (SaaS) Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Software-as-a-Service (SaaS) Market Overview by Component

- Saudi Arabian Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Saudi Arabian Software-as-a-Service (SaaS) Market Overview by Company Type

- Saudi Arabian Software-as-a-Service (SaaS) Market Overview by Application

- Saudi Arabian Software-as-a-Service (SaaS) Market Overview by Industry Sector

- MOROCCO

- Moroccan Software-as-a-Service (SaaS) Market Overview by Component

- Moroccan Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Moroccan Software-as-a-Service (SaaS) Market Overview by Company Type

- Moroccan Software-as-a-Service (SaaS) Market Overview by Application

- Moroccan Software-as-a-Service (SaaS) Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Software-as-a-Service (SaaS) Market Overview by Component

- Kuwaiti Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Kuwaiti Software-as-a-Service (SaaS) Market Overview by Company Type

- Kuwaiti Software-as-a-Service (SaaS) Market Overview by Application

- Kuwaiti Software-as-a-Service (SaaS) Market Overview by Industry Sector

- QATAR

- Qatari Software-as-a-Service (SaaS) Market Overview by Component

- Qatari Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Qatari Software-as-a-Service (SaaS) Market Overview by Company Type

- Qatari Software-as-a-Service (SaaS) Market Overview by Application

- Qatari Software-as-a-Service (SaaS) Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Software-as-a-Service (SaaS) Market Overview by Component

- Rest of Middle East & Africa Software-as-a-Service (SaaS) Market Overview by Deployment Type

- Rest of Middle East & Africa Software-as-a-Service (SaaS) Market Overview by Company Type

- Rest of Middle East & Africa Software-as-a-Service (SaaS) Market Overview by Application

- Rest of Middle East & Africa Software-as-a-Service (SaaS) Market Overview by Industry Sector

PART C: GUIDE TO THE INDUSTRY

- NORTH AMERICA

- EUROPE

- ASIA-PACIFIC

- REST OF WORLD

PART D: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

Adobe Inc.

Alibaba Cloud International

Atlassian Corporation

Babbel

Box, Inc.

Cisco Systems, Inc.

Citrix Systems, Inc.

Google LLC

HPE

HubSpot, Inc.

IBM Corporation

Infosys

Intuit Inc.

IONOS Cloud Inc.

Microsoft Corporation

NetSuite Inc.

Oracle Corporation

Rackspace Technology, Inc.

Sage Group plc

Salesforce, Inc.

SAP SE

ServiceNow

Shopify Inc.

Slack Technologies, LLC

TCS

Tecent Holdings

Trend Micro

VMware Inc.

Workday, Inc.

Workiva

Zendesk, Inc.

Zoho Corporation

Zoom Video Communications, Inc.

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |