Global Product Life Cycle Management (PLM) Software Market - Applications, Deployment Types, Company Types, and Industry Sectors

- Published: Jul 2025

- Pages: 457 | Charts: 399

- Report Code: ITM050

SHARE THIS REPORT:

Global Product Life Cycle Management (PLM) Software Market Trends and Outlook

The global Product Lifecycle Management (PLM) software market is undergoing a significant transformation, projected to more than double from US$28 billion in 2024 to over US$43.5 billion by 2030 at a CAGR of 7.7%, reflecting accelerating digitalization across design, engineering, and manufacturing workflows. This expansion is underpinned by the urgent need for agile, data-driven processes in industries such as automotive, aerospace, and industrial equipment, where complexity and compliance burdens are intensifying. North America continues to lead in adoption due to its mature industrial base and regulatory rigor, while Asia Pacific is emerging as the fastest-growing market, driven by ambitious modernization programs across China, India, and Japan.

Cloud-native platforms and software-as-a-service (SaaS) delivery models are reshaping how PLM is consumed, offering faster deployment, lower upfront costs, and elastic scalability. Leading providers such as Siemens Digital Industries Software, PTC, Dassault Syst�mes, and Autodesk are doubling down on AI-driven capabilities, enabling predictive design, smarter simulation, and real-time collaboration. This has not only reduced product development timelines but also made enterprise-grade PLM accessible to mid-market firms, widening the addressable market.

Product Life Cycle Management (PLM) Software Regional Market Analysis

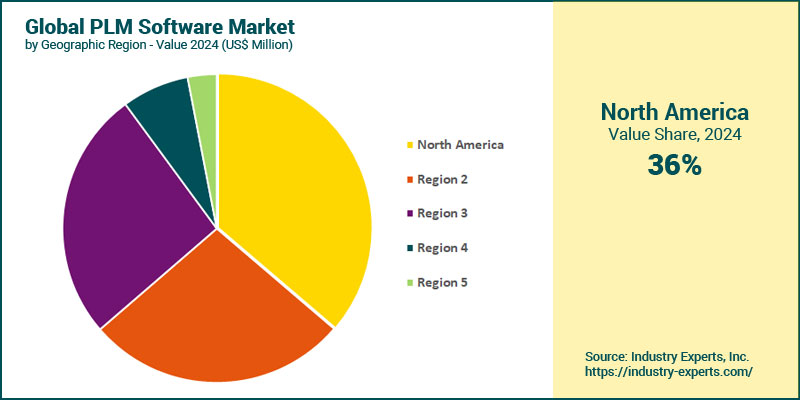

Between 2024 and 2030, the global Product Lifecycle Management (PLM) software market is projected to expand from US$28 billion to approximately US$43.5 billion, growing at a CAGR of 7.7%. North America held the largest regional share in 2024, accounting for 36.3% of global market value. Its dominance stems from sustained investments in digital twin technologies, early cloud adoption, and stringent regulatory compliance in sectors like aerospace, automotive, and defense. However, Asia-Pacific is poised to outpace all other regions with the fastest CAGR of 10% over the same period. By 2030, the region's market size is expected to reach nearly US$13 billion, driven by government-led manufacturing upgrades in China, Japan, and India, alongside rising demand for SaaS-based PLM solutions among mid-tier manufacturers. South America also shows strong momentum, reflecting broader regional digitization efforts and cloud-native PLM adoption in Brazil and Argentina.

Product Life Cycle Management (PLM) Software Market Analysis by Deployment Type

Cloud-based deployments will continue to dominate and accelerate, growing at a CAGR of 8.5%, the fastest among all segments. In 2024, the cloud segment accounted for nearly 71% of the total market, a lead driven by the rising demand for agile, scalable, and cost-effective PLM platforms across all company sizes. On-premise solutions, while still relevant, particularly in industries with strict data residency or security needs, are expected to grow more modestly. The slower growth reflects a broader industry shift toward cloud-native architectures and SaaS platforms, which offer lower upfront costs, faster deployment, and better interoperability. As PLM increasingly converges with IoT, digital twins, and simulation technologies, cloud models will remain the cornerstone of future-ready deployments.

Product Life Cycle Management (PLM) Software Market Analysis by Company Type

Large enterprises will remain the dominant customer base, contributing US$18.5 billion in 2024, roughly 66.5% of total spend, driven by continued investment in digital twin integration, regulatory compliance, and enterprise-wide product innovation platforms. However, small and medium-sized enterprises (SMEs) are projected to be the fastest-growing segment, expanding at a CAGR of 9%. This acceleration is fueled by the growing availability of modular, cloud-based PLM tools tailored to mid-market needs, offering subscription pricing, faster deployments, and simplified configurations that reduce IT burden. As PLM vendors increasingly shift toward SaaS delivery and vertical-specific solutions, adoption among SMEs is likely to accelerate further.

Product Life Cycle Management (PLM) Software Market Analysis by Software Type

Collaborative Product Definition Management (cPDm) remains the largest segment, accounting for 36.1% of total market value. Its strength stems from its foundational role in data governance, configuration management, and cross-functional collaboration in complex engineering environments. However, the fastest growth is anticipated in the "Other PLM-related Tools" category, which includes emerging solutions for sustainability analytics, PLM-integrated compliance, and connected supply chain management. This segment is projected to grow at a CAGR of 11.4%, driven by evolving ESG mandates and the demand for end-to-end traceability. Simulation & Analysis tools are the second-fastest growing segment. The rise is fueled by increased adoption of digital twins, real-time physics modeling, and AI-driven design validation, especially in automotive and aerospace industries. Meanwhile, Mechanical CAD, though still significant, is forecast to grow more modestly at just 4.5%, as the segment matures and faces commoditization pressures from integrated and low-code platforms.

Product Life Cycle Management (PLM) Software Market Analysis by Industry Sector

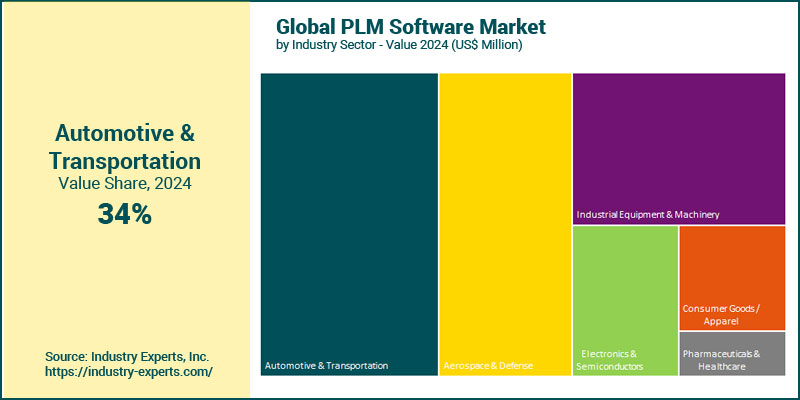

The automotive & transportation sector remains the largest market with a share of 34% of total PLM spend in 2024. Its continued leadership is underpinned by deep investments in digital twins, regulatory traceability, and electrification-led innovation cycles that require tightly integrated engineering workflows. However, the electronics & semiconductors segment is expected to be the fastest-growing vertical, registering a CAGR of 11%. This rapid rise is fueled by the increasing product complexity, shorter design cycles, and the need to integrate PLM with embedded software, simulation, and chip manufacturing processes. Consumer goods and apparel is the second-fastest-growing sector, being driven by sustainability pressures, design personalization, and faster time-to-market for fashion and lifestyle brands, factors that are pushing companies toward SaaS-based PLM tools with strong support for material traceability and supplier collaboration.

Product Life Cycle Management (PLM) Software Market Report Scope

This global report on Product Life Cycle Management (PLM) Software market analyzes the global and regional market based on Deployment Type, Company Type, Software Type, and Industry Sector for the period 2021-2030 with projection from 2024 to 2030 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Historical Period: | 2021-2024 | |

| Base Year: | 2024 | |

| Forecast Period: | 2024-2030 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 15+ |

Product Life Cycle Management (PLM) Software Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Product Life Cycle Management (PLM) Software Market by Deployment Type

- Cloud

- On-Premise

Product Life Cycle Management (PLM) Software Market by Company Type

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

Product Life Cycle Management (PLM) Software Market by Software Type

- Collaborative Product Definition Management (cPDm)

- Mechanical CAD

- Simulation & Analysis

- Digital Manufacturing

- Other PLM-related Tools

Product Life Cycle Management (PLM) Software Market by Industry Sector

- Automotive & Transportation

- Aerospace & Defense

- Industrial Equipment & Machinery

- Electronics & Semiconductors

- Consumer Goods / Apparel

- Pharmaceuticals & Healthcare

Product Life Cycle Management (PLM) Software Market Frequently Asked Questions (FAQs)

Global PLM software market size is estimated at US$28 billion in 2024.

The global PLM software market is expected to expand to US$43.5 billion by 2030, registering a CAGR of 7.7% during 2024-2030.

North America held the largest regional share in 2024, accounting for 36.3% of global Product Life Cycle Management (PLM) software market value.

Asia-Pacific is poised to outpace all other regions with the fastest CAGR of 10% over the outlook period.

Cloud-based deployments will continue to dominate and accelerate, accounted for US$19.8 billion, or nearly 71% of the total market in 2024.

Other PLM-related Tools category, which includes emerging solutions for sustainability analytics, PLM-integrated compliance, and connected supply chain management, is projected to grow at a faster 2024-2030 CAGR of 11.4%.

The top PLM software providers globally are Siemens Digital Industries Software, Dassault Systemes, and PTC, each offering comprehensive platforms that span CAD, simulation, digital twins, and enterprise-grade lifecycle management. Other notable players include Autodesk, SAP, Oracle, and Arena (a PTC business), each targeting specific niches.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Product Life Cycle Management (PLM) Software Applications

- Market Segmentation for Product Life Cycle Management (PLM) Software

- Deployment Types

- Company Types based on Size

- PLM Software Types

- Industry Sectors

- Key Trends in Product Life Cycle Management (PLM) Software Market

2. INDUSTRY LANDSCAPE

- Global Product Life Cycle Management (PLM) Software Market Outlook

- Comprehensive Product Life Cycle Management (PLM) Software Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Product Life Cycle Management (PLM) Software Industry

- Startup Strategies for Product Life Cycle Management (PLM) Software Industry

- SWOT Analysis of Product Life Cycle Management (PLM) Software Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Product Life Cycle Management (PLM) Software Companies

- Market Share Analysis of Product Life Cycle Management (PLM) Software Companies

- SWOT Analysis of Key Players in the Product Life Cycle Management (PLM) Software Industry

- Key Market Players

- ANSYS Inc.

- Aras Corporation

- Arena Solutions

- Autodesk Inc.

- Coats Digital

- Dassault Systemes SE (Dassault Group)

- Hexagon AB

- IBM Corporation

- Infor (Koch Industries Inc.)

- Oracle Corporation

- PROCAD GmbH & Co. KG

- PTC Inc.

- Pulse Technology Systems Ltd.

- SAP SE

- Siemens AG

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Product Life Cycle Management (PLM) Software Deployment Type Market Overview by Global Region

- Cloud

- On-Premise

- Global Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Product Life Cycle Management (PLM) Software Company Type Market Overview by Global Region

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

- Global Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Product Life Cycle Management (PLM) Software Type Market Overview by Global Region

- cPDm

- Mechanical CAD

- Simulation & Analysis

- Digital Manufacturing

- Other PLM-related Tools

- Global Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- Product Life Cycle Management (PLM) Software Industry Sector Market Overview by Global Region

- Automotive & Transportation

- Aerospace & Defense

- Industrial Equipment & Machinery

- Electronics & Semiconductors

- Consumer Goods / Apparel

- Pharmaceuticals & Healthcare

PART B: REGIONAL MARKET PERSPECTIVE

- Global Product Life Cycle Management (PLM) Software Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Product Life Cycle Management (PLM) Software Market Overview by Geographic Region

- North American Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- North American Product Life Cycle Management (PLM) Software Market Overview by Company Type

- North American Product Life Cycle Management (PLM) Software Market Overview by Software Type

- North American Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- Country-wise Analysis of North American Product Life Cycle Management (PLM) Software Market

- THE UNITED STATES

- United States Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- United States Product Life Cycle Management (PLM) Software Market Overview by Company Type

- United States Product Life Cycle Management (PLM) Software Market Overview by Software Type

- United States Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- CANADA

- Canadian Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Canadian Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Canadian Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Canadian Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- MEXICO

- Mexican Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Mexican Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Mexican Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Mexican Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

7. EUROPE

- European Product Life Cycle Management (PLM) Software Market Overview by Geographic Region

- European Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- European Product Life Cycle Management (PLM) Software Market Overview by Company Type

- European Product Life Cycle Management (PLM) Software Market Overview by Software Type

- European Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- Country-wise Analysis of European Product Life Cycle Management (PLM) Software Market

- GERMANY

- German Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- German Product Life Cycle Management (PLM) Software Market Overview by Company Type

- German Product Life Cycle Management (PLM) Software Market Overview by Software Type

- German Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- United Kingdom Product Life Cycle Management (PLM) Software Market Overview by Company Type

- United Kingdom Product Life Cycle Management (PLM) Software Market Overview by Software Type

- United Kingdom Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- FRANCE

- French Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- French Product Life Cycle Management (PLM) Software Market Overview by Company Type

- French Product Life Cycle Management (PLM) Software Market Overview by Software Type

- French Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- ITALY

- Italian Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Italian Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Italian Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Italian Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Dutch Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Dutch Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Dutch Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- SPAIN

- Spanish Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Spanish Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Spanish Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Spanish Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- RUSSIA

- Russian Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Russian Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Russian Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Russian Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- SWITZERLAND

- Swiss Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Swiss Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Swiss Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Swiss Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Rest of Europe Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Rest of Europe Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Rest of Europe Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Product Life Cycle Management (PLM) Software Market Overview by Geographic Region

- Asia-Pacific Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Asia-Pacific Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Asia-Pacific Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Asia-Pacific Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Product Life Cycle Management (PLM) Software Market

- CHINA

- Chinese Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Chinese Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Chinese Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Chinese Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- JAPAN

- Japanese Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Japanese Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Japanese Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Japanese Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- INDIA

- Indian Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Indian Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Indian Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Indian Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- AUSTRALIA

- Australia Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Australia Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Australia Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Australia Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- SINGAPORE

- Singaporean Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Singaporean Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Singaporean Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Singaporean Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- South Korean Product Life Cycle Management (PLM) Software Market Overview by Company Type

- South Korean Product Life Cycle Management (PLM) Software Market Overview by Software Type

- South Korean Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Rest of Asia-Pacific Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Rest of Asia-Pacific Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Rest of Asia-Pacific Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Product Life Cycle Management (PLM) Software Market Overview by Geographic Region

- South American Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- South American Product Life Cycle Management (PLM) Software Market Overview by Company Type

- South American Product Life Cycle Management (PLM) Software Market Overview by Software Type

- South American Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- Country-wise Analysis of South American Product Life Cycle Management (PLM) Software Market

- BRAZIL

- Brazilian Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Brazilian Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Brazilian Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Brazilian Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- ARGENTINA

- Argentine Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Argentine Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Argentine Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Argentine Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- COLOMBIA

- Colombian Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Colombian Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Colombian Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Colombian Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- CHILE

- Chilean Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Chilean Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Chilean Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Chilean Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- PERU

- Peruvian Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Peruvian Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Peruvian Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Peruvian Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Rest of South America Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Rest of South America Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Rest of South America Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Product Life Cycle Management (PLM) Software Market Overview by Geographic Region

- Middle East & Africa Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Middle East & Africa Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Middle East & Africa Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Middle East & Africa Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Product Life Cycle Management (PLM) Software Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- United Arab Emirates Product Life Cycle Management (PLM) Software Market Overview by Company Type

- United Arab Emirates Product Life Cycle Management (PLM) Software Market Overview by Software Type

- United Arab Emirates Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- SOUTH AFRICA

- South African Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- South African Product Life Cycle Management (PLM) Software Market Overview by Company Type

- South African Product Life Cycle Management (PLM) Software Market Overview by Software Type

- South African Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- EGYPT

- Egyptian Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Egyptian Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Egyptian Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Egyptian Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Saudi Arabian Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Saudi Arabian Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Saudi Arabian Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- MOROCCO

- Moroccan Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Moroccan Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Moroccan Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Moroccan Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Kuwaiti Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Kuwaiti Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Kuwaiti Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- QATAR

- Qatari Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Qatari Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Qatari Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Qatari Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Product Life Cycle Management (PLM) Software Market Overview by Deployment Type

- Rest of Middle East & Africa Product Life Cycle Management (PLM) Software Market Overview by Company Type

- Rest of Middle East & Africa Product Life Cycle Management (PLM) Software Market Overview by Software Type

- Rest of Middle East & Africa Product Life Cycle Management (PLM) Software Market Overview by Industry Sector

PART C: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

ANSYS Inc.

Aras Corporation

Arena Solutions

Autodesk Inc.

Coats Digital

Dassault Systemes SE (Dassault Group)

Hexagon AB

IBM Corporation

Infor (Koch Industries Inc.)

Oracle Corporation

PROCAD GmbH & Co. KG

PTC Inc.

Pulse Technology Systems Ltd.

SAP SE

Siemens AG

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |