Global Network Monitoring Hardware Market - Technologies, Bandwidths and Industry Sectors

- Published: Aug 2025

- Pages: 468 | Charts: 407

- Report Code: ITM033

SHARE THIS REPORT:

Global Network Monitoring Hardware Market Trends and Outlook

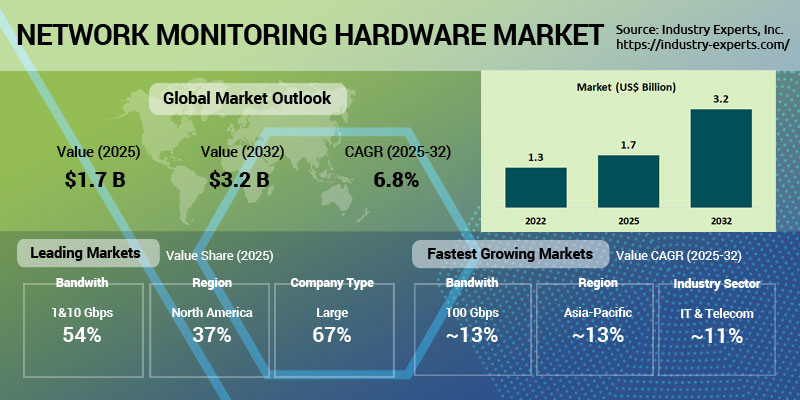

The global network monitoring hardware market is on track to nearly double in size between 2025 and 2032, growing from US$1.7 billion to approximately US$3.2 billion at a CAGR of 9.8%. Growth is being driven by the accelerating adoption of ultra-high-speed networks, rapid 5G rollouts, multi-gigabit enterprise architectures, and increasing complexity from hybrid and multi-cloud environments. Across industries such as IT & Telecom, BFSI, healthcare, and manufacturing, organizations are prioritizing deterministic visibility and real-time packet capture to ensure performance, security, and compliance in the face of surging data volumes and evolving cyber threats.

Technological innovation is reshaping the market, with vendors introducing FPGA-accelerated probes, SmartNIC-powered capture systems, and time-synchronized recording appliances capable of processing terabits of traffic with nanosecond precision. The shift toward disaggregated, open monitoring fabrics is creating opportunities for specialized modular hardware, while integration with AI analytics platforms is enabling real-time anomaly detection and automated policy enforcement. Regionally, North America remains the largest market due to early adoption of 100G/400G packet brokers and strong compliance drivers, while Asia-Pacific is the fastest-growing region, led by telecom, hyperscale cloud expansion, and high-throughput data center deployments.

Leading vendors include APCON, Arista Networks, Cisco Systems, cPacket Networks, Endace, Garland Technology, Gigamon, Ixia (Keysight), Keysight Technologies, Napatech, NETSCOUT Systems, Plixer, Profitap, Riverbed Technology, Silicom, and Viavi Solutions, all competing on performance, integration, and ecosystem interoperability.

Network Monitoring Hardware Regional Market Analysis

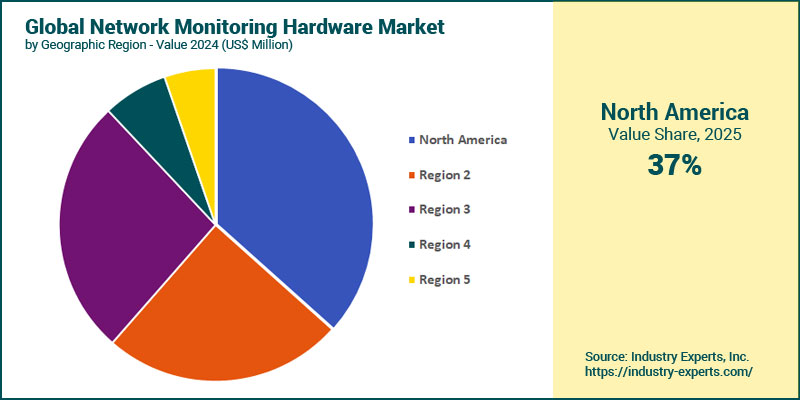

North America will remain the largest regional market throughout the forecast period, accounting for the highest share in 2025 at 36.6%. Its leadership is driven by early and widespread adoption of 100G/400G packet broker infrastructure, strong investment from hyperscalers, and compliance with stringent regulatory frameworks like HIPAA, GLBA, and sector-specific mandates in finance and healthcare. Asia-Pacific is forecast to be the fastest-growing region, registering a CAGR of 12.7% to reach US$1 billion by 2032. Growth is spurred by rapid network buildouts among telecom operators and cloud service providers in China, India, and Southeast Asia, alongside widespread 5G rollouts and the transition to high-density, ultra-fast data center fabrics.

Network Monitoring Hardware Market Analysis by Technology Type

Ethernet is the largest technology segment in 2025, supported by its widespread deployment in enterprise networks, compatibility with multi-gigabit architectures, and cost efficiency for core and edge monitoring applications. Fiber Optic technology holds the second-largest share, benefiting from high-speed backbone upgrades, long-distance data transmission needs, and increasing adoption in data center interconnects. InfiniBand will be the fastest-growing technology, registering an 11.3% CAGR. Its momentum is fueled by its ultra-low latency, high throughput, and suitability for high-performance computing (HPC), AI clusters, and advanced analytics workloads. The technology's growth is also reinforced by hyperscaler investments and the need for lossless packet delivery in environments running 400G and emerging 800G interconnects.

Network Monitoring Hardware Market Analysis by Bandwidth

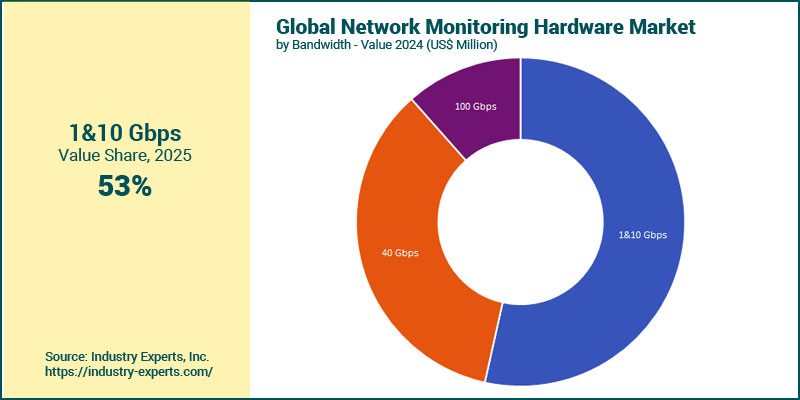

The 1 & 10 Gbps category will remain the largest segment and projected to reach about US$1.6 billion by 2032. Its dominance is supported by its entrenched role in enterprise LANs, campus networks, and branch deployments where cost-effective visibility remains a priority. The fastest-growing category will be 100 Gbps, advancing at a 12.9% CAGR. This segment is benefiting from hyperscaler deployments, HPC and AI workloads, and the growing need for packet brokers and capture appliances capable of handling ultra-high throughput without packet loss. The rising shift toward 400G and 800G backbone links in telecom and cloud environments will further accelerate demand for monitoring hardware optimized for 100 Gbps aggregation and traffic inspection, particularly in data center fabrics and regulated industries requiring deterministic visibility.

Network Monitoring Hardware Market Analysis by Company Type

Large enterprises will continue to hold the largest share, accounting for 67.4%. Their dominance stems from expansive network infrastructures, multi-gigabit and hybrid cloud environments, and strict compliance obligations in sectors like finance, healthcare, and manufacturing, which demand advanced packet brokers, FPGA-accelerated capture systems, and high-density forensic recording appliances. SMEs, though smaller in absolute value, will be the fastest-growing segment, registering an 11.1% CAGR. Growth in this segment is driven by rising cyber threats, increased reliance on cloud and SaaS applications, and the availability of more affordable, plug-and-play monitoring appliances with simplified management interfaces. Vendors catering to SMEs are also benefiting from demand for compact, ruggedized probes and subscription-based hardware models, enabling smaller organizations to achieve enterprise-grade visibility without prohibitive capital costs.

Network Monitoring Hardware Market Analysis by Industry Sector

IT & Telecom is the largest sector, generating US$590 million in 2025 and reaching about US$1.2 billion by 2032. Its leadership is underpinned by rapid 5G deployments, hyperscale data center expansions, and the need for ultra-high-speed packet brokers and forensic capture appliances to support large-scale, low-latency networks. BFSI is the second-largest sector in 2025, supported by stringent compliance mandates such as PCI DSS 4.0 and GLBA, as well as the sector's reliance on real-time transaction monitoring and security visibility. The fastest-growing sector will be IT & Telecom, with a CAGR of 10.9%, driven by escalating bandwidth demands, the rollout of 400G/800G network backbones, and rising adoption of SmartNIC-enabled monitoring in carrier and enterprise environments.

Network Monitoring Hardware Market Report Scope

This global report on Network Monitoring Hardware market analyzes the global and regional market based on Technology Type, Bandwidth, Company Type and Industry Sector for the period 2022-2032 with forecasts from 2025 to 2032 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Analysis Period: | 2022-2032 | |

| Base Year: | 2025 | |

| Forecast Period: | 2025-2032 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 15+ |

Network Monitoring Hardware Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Network Monitoring Hardware Market by Technology Type

- Ethernet

- Fiber Optics

- InfiniBand

Network Monitoring Hardware Market by Bandwidth

- 1&10 Gbps

- 40 Gbps

- 100 Gbps

Network Monitoring Hardware Market by Company Type

- Large Enterprises

- SMEs

Network Monitoring Hardware Market by Industry Sector

- IT & Telecom

- Banking, Financial Services, and Insurance (BFSI)

- Government & Defense

- Healthcare

- Manufacturing

- Energy & Utilities

- Retail & E-commerce

- Education

- Media & Entertainment

- Transportation & Logistics

- Other Industry Sectors

Network Monitoring Hardware Market Frequently Asked Questions (FAQs)

The market is valued at US$1.67 billion in 2025 and is expected to reach US$3.22 billion by 2032, growing at a CAGR of 9.8%.

North America is the largest regional market, driven by early 100G/400G adoption, hyperscale investments, and strong compliance frameworks such as HIPAA and GLBA.

Asia-Pacific is the fastest-growing region, expanding at a CAGR of 12.7%, fueled by telecom and cloud provider network buildouts, 5G rollouts, and ultra-high-speed data center fabrics.

Ethernet holds the largest share, while InfiniBand is the fastest-growing technology due to its ultra-low latency and suitability for HPC, AI, and 400G+ interconnects.

IT & Telecom leads in revenue share, supported by large-scale network infrastructure, bandwidth growth, and the need for deterministic visibility in 5G and cloud environments.

The need to support hyperscaler deployments, AI workloads, and high-throughput traffic inspection without packet loss is boosting demand for 100 Gbps appliances, making it the fastest-growing bandwidth category.

Key vendors include APCON, Arista Networks, Cisco, Gigamon, Keysight, Napatech, NETSCOUT, Viavi Solutions, and others innovating in FPGA acceleration, SmartNIC capture, and AI integration.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Network Monitoring Hardware

- Market Segmentation for Network Monitoring Hardware

- Technology Types

- Bandwidths

- Company Types

- Industry Sectors

- Key Trends in Network Monitoring Hardware Market

2. INDUSTRY LANDSCAPE

- Global Network Monitoring Hardware Market Outlook

- Comprehensive Network Monitoring Hardware Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Network Monitoring Hardware Industry

- Startup Strategies for Network Monitoring Hardware Industry

- SWOT Analysis of Network Monitoring Hardware Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Network Monitoring Hardware Companies

- Market Share Analysis of Network Monitoring Hardware Companies

- SWOT Analysis of Key Players in the Network Monitoring Hardware Industry

- Key Market Players

- APCON

- Arista Networks

- Cisco Systems

- cPacket Networks

- Endace

- Garland Technology

- Gigamon

- Ixia (Keysight)

- Keysight Technologies

- Napatech

- NETSCOUT Systems

- Plixer

- Profitap

- Riverbed Technology

- Silicom

- Viavi Solutions

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Network Monitoring Hardware Market Overview by Technology Type

- Network Monitoring Hardware Technology Type Market Overview by Global Region

- Ethernet

- Fiber Optics

- InfiniBand

- Global Network Monitoring Hardware Market Overview by Bandwidth

- Network Monitoring Hardware Bandwidth Market Overview by Global Region

- 1&10 Gbps

- 40 Gbps

- 100 Gbps

- Global Network Monitoring Hardware Market Overview by Company Type

- Network Monitoring Hardware Company Type Market Overview by Global Region

- Large Enterprises

- SMEs

- Global Network Monitoring Hardware Market Overview by Industry Sector

- Network Monitoring Hardware Industry Sector Market Overview by Global Region

- IT & Telecom

- Banking, Financial Services, and Insurance (BFSI)

- Government & Defense

- Healthcare

- Manufacturing

- Energy & Utilities

- Retail & E-commerce

- Education

- Media & Entertainment

- Transportation & Logistics

- Other Industry Sectors

PART B: REGIONAL MARKET PERSPECTIVE

- Global Network Monitoring Hardware Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Network Monitoring Hardware Market Overview by Geographic Region

- North American Network Monitoring Hardware Market Overview by Technology Type

- North American Network Monitoring Hardware Market Overview by Bandwidth

- North American Network Monitoring Hardware Market Overview by Company Type

- North American Network Monitoring Hardware Market Overview by Industry Sector

- Country-wise Analysis of North American Network Monitoring Hardware Market

- THE UNITED STATES

- United States Network Monitoring Hardware Market Overview by Technology Type

- United States Network Monitoring Hardware Market Overview by Bandwidth

- United States Network Monitoring Hardware Market Overview by Company Type

- United States Network Monitoring Hardware Market Overview by Industry Sector

- CANADA

- Canadian Network Monitoring Hardware Market Overview by Technology Type

- Canadian Network Monitoring Hardware Market Overview by Bandwidth

- Canadian Network Monitoring Hardware Market Overview by Company Type

- Canadian Network Monitoring Hardware Market Overview by Industry Sector

- MEXICO

- Mexican Network Monitoring Hardware Market Overview by Technology Type

- Mexican Network Monitoring Hardware Market Overview by Bandwidth

- Mexican Network Monitoring Hardware Market Overview by Company Type

- Mexican Network Monitoring Hardware Market Overview by Industry Sector

7. EUROPE

- European Network Monitoring Hardware Market Overview by Geographic Region

- European Network Monitoring Hardware Market Overview by Technology Type

- European Network Monitoring Hardware Market Overview by Bandwidth

- European Network Monitoring Hardware Market Overview by Company Type

- European Network Monitoring Hardware Market Overview by Industry Sector

- Country-wise Analysis of European Network Monitoring Hardware Market

- GERMANY

- German Network Monitoring Hardware Market Overview by Technology Type

- German Network Monitoring Hardware Market Overview by Bandwidth

- German Network Monitoring Hardware Market Overview by Company Type

- German Network Monitoring Hardware Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Network Monitoring Hardware Market Overview by Technology Type

- United Kingdom Network Monitoring Hardware Market Overview by Bandwidth

- United Kingdom Network Monitoring Hardware Market Overview by Company Type

- United Kingdom Network Monitoring Hardware Market Overview by Industry Sector

- FRANCE

- French Network Monitoring Hardware Market Overview by Technology Type

- French Network Monitoring Hardware Market Overview by Bandwidth

- French Network Monitoring Hardware Market Overview by Company Type

- French Network Monitoring Hardware Market Overview by Industry Sector

- ITALY

- Italian Network Monitoring Hardware Market Overview by Technology Type

- Italian Network Monitoring Hardware Market Overview by Bandwidth

- Italian Network Monitoring Hardware Market Overview by Company Type

- Italian Network Monitoring Hardware Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Network Monitoring Hardware Market Overview by Technology Type

- Dutch Network Monitoring Hardware Market Overview by Bandwidth

- Dutch Network Monitoring Hardware Market Overview by Company Type

- Dutch Network Monitoring Hardware Market Overview by Industry Sector

- SPAIN

- Spanish Network Monitoring Hardware Market Overview by Technology Type

- Spanish Network Monitoring Hardware Market Overview by Bandwidth

- Spanish Network Monitoring Hardware Market Overview by Company Type

- Spanish Network Monitoring Hardware Market Overview by Industry Sector

- RUSSIA

- Russian Network Monitoring Hardware Market Overview by Technology Type

- Russian Network Monitoring Hardware Market Overview by Bandwidth

- Russian Network Monitoring Hardware Market Overview by Company Type

- Russian Network Monitoring Hardware Market Overview by Industry Sector

- SWITZERLAND

- Swiss Network Monitoring Hardware Market Overview by Technology Type

- Swiss Network Monitoring Hardware Market Overview by Bandwidth

- Swiss Network Monitoring Hardware Market Overview by Company Type

- Swiss Network Monitoring Hardware Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Network Monitoring Hardware Market Overview by Technology Type

- Rest of Europe Network Monitoring Hardware Market Overview by Bandwidth

- Rest of Europe Network Monitoring Hardware Market Overview by Company Type

- Rest of Europe Network Monitoring Hardware Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Network Monitoring Hardware Market Overview by Geographic Region

- Asia-Pacific Network Monitoring Hardware Market Overview by Technology Type

- Asia-Pacific Network Monitoring Hardware Market Overview by Bandwidth

- Asia-Pacific Network Monitoring Hardware Market Overview by Company Type

- Asia-Pacific Network Monitoring Hardware Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Network Monitoring Hardware Market

- CHINA

- Chinese Network Monitoring Hardware Market Overview by Technology Type

- Chinese Network Monitoring Hardware Market Overview by Bandwidth

- Chinese Network Monitoring Hardware Market Overview by Company Type

- Chinese Network Monitoring Hardware Market Overview by Industry Sector

- JAPAN

- Japanese Network Monitoring Hardware Market Overview by Technology Type

- Japanese Network Monitoring Hardware Market Overview by Bandwidth

- Japanese Network Monitoring Hardware Market Overview by Company Type

- Japanese Network Monitoring Hardware Market Overview by Industry Sector

- INDIA

- Indian Network Monitoring Hardware Market Overview by Technology Type

- Indian Network Monitoring Hardware Market Overview by Bandwidth

- Indian Network Monitoring Hardware Market Overview by Company Type

- Indian Network Monitoring Hardware Market Overview by Industry Sector

- AUSTRALIA

- Australia Network Monitoring Hardware Market Overview by Technology Type

- Australia Network Monitoring Hardware Market Overview by Bandwidth

- Australia Network Monitoring Hardware Market Overview by Company Type

- Australia Network Monitoring Hardware Market Overview by Industry Sector

- SINGAPORE

- Singaporean Network Monitoring Hardware Market Overview by Technology Type

- Singaporean Network Monitoring Hardware Market Overview by Bandwidth

- Singaporean Network Monitoring Hardware Market Overview by Company Type

- Singaporean Network Monitoring Hardware Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Network Monitoring Hardware Market Overview by Technology Type

- South Korean Network Monitoring Hardware Market Overview by Bandwidth

- South Korean Network Monitoring Hardware Market Overview by Company Type

- South Korean Network Monitoring Hardware Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Network Monitoring Hardware Market Overview by Technology Type

- Rest of Asia-Pacific Network Monitoring Hardware Market Overview by Bandwidth

- Rest of Asia-Pacific Network Monitoring Hardware Market Overview by Company Type

- Rest of Asia-Pacific Network Monitoring Hardware Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Network Monitoring Hardware Market Overview by Geographic Region

- South American Network Monitoring Hardware Market Overview by Technology Type

- South American Network Monitoring Hardware Market Overview by Bandwidth

- South American Network Monitoring Hardware Market Overview by Company Type

- South American Network Monitoring Hardware Market Overview by Industry Sector

- Country-wise Analysis of South American Network Monitoring Hardware Market

- BRAZIL

- Brazilian Network Monitoring Hardware Market Overview by Technology Type

- Brazilian Network Monitoring Hardware Market Overview by Bandwidth

- Brazilian Network Monitoring Hardware Market Overview by Company Type

- Brazilian Network Monitoring Hardware Market Overview by Industry Sector

- ARGENTINA

- Argentine Network Monitoring Hardware Market Overview by Technology Type

- Argentine Network Monitoring Hardware Market Overview by Bandwidth

- Argentine Network Monitoring Hardware Market Overview by Company Type

- Argentine Network Monitoring Hardware Market Overview by Industry Sector

- COLOMBIA

- Colombian Network Monitoring Hardware Market Overview by Technology Type

- Colombian Network Monitoring Hardware Market Overview by Bandwidth

- Colombian Network Monitoring Hardware Market Overview by Company Type

- Colombian Network Monitoring Hardware Market Overview by Industry Sector

- CHILE

- Chilean Network Monitoring Hardware Market Overview by Technology Type

- Chilean Network Monitoring Hardware Market Overview by Bandwidth

- Chilean Network Monitoring Hardware Market Overview by Company Type

- Chilean Network Monitoring Hardware Market Overview by Industry Sector

- PERU

- Peruvian Network Monitoring Hardware Market Overview by Technology Type

- Peruvian Network Monitoring Hardware Market Overview by Bandwidth

- Peruvian Network Monitoring Hardware Market Overview by Company Type

- Peruvian Network Monitoring Hardware Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Network Monitoring Hardware Market Overview by Technology Type

- Rest of South America Network Monitoring Hardware Market Overview by Bandwidth

- Rest of South America Network Monitoring Hardware Market Overview by Company Type

- Rest of South America Network Monitoring Hardware Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Network Monitoring Hardware Market Overview by Geographic Region

- Middle East & Africa Network Monitoring Hardware Market Overview by Technology Type

- Middle East & Africa Network Monitoring Hardware Market Overview by Bandwidth

- Middle East & Africa Network Monitoring Hardware Market Overview by Company Type

- Middle East & Africa Network Monitoring Hardware Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Network Monitoring Hardware Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Network Monitoring Hardware Market Overview by Technology Type

- United Arab Emirates Network Monitoring Hardware Market Overview by Bandwidth

- United Arab Emirates Network Monitoring Hardware Market Overview by Company Type

- United Arab Emirates Network Monitoring Hardware Market Overview by Industry Sector

- SOUTH AFRICA

- South African Network Monitoring Hardware Market Overview by Technology Type

- South African Network Monitoring Hardware Market Overview by Bandwidth

- South African Network Monitoring Hardware Market Overview by Company Type

- South African Network Monitoring Hardware Market Overview by Industry Sector

- EGYPT

- Egyptian Network Monitoring Hardware Market Overview by Technology Type

- Egyptian Network Monitoring Hardware Market Overview by Bandwidth

- Egyptian Network Monitoring Hardware Market Overview by Company Type

- Egyptian Network Monitoring Hardware Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Network Monitoring Hardware Market Overview by Technology Type

- Saudi Arabian Network Monitoring Hardware Market Overview by Bandwidth

- Saudi Arabian Network Monitoring Hardware Market Overview by Company Type

- Saudi Arabian Network Monitoring Hardware Market Overview by Industry Sector

- MOROCCO

- Moroccan Network Monitoring Hardware Market Overview by Technology Type

- Moroccan Network Monitoring Hardware Market Overview by Bandwidth

- Moroccan Network Monitoring Hardware Market Overview by Company Type

- Moroccan Network Monitoring Hardware Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Network Monitoring Hardware Market Overview by Technology Type

- Kuwaiti Network Monitoring Hardware Market Overview by Bandwidth

- Kuwaiti Network Monitoring Hardware Market Overview by Company Type

- Kuwaiti Network Monitoring Hardware Market Overview by Industry Sector

- QATAR

- Qatari Network Monitoring Hardware Market Overview by Technology Type

- Qatari Network Monitoring Hardware Market Overview by Bandwidth

- Qatari Network Monitoring Hardware Market Overview by Company Type

- Qatari Network Monitoring Hardware Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Network Monitoring Hardware Market Overview by Technology Type

- Rest of Middle East & Africa Network Monitoring Hardware Market Overview by Bandwidth

- Rest of Middle East & Africa Network Monitoring Hardware Market Overview by Company Type

- Rest of Middle East & Africa Network Monitoring Hardware Market Overview by Industry Sector

PART C: INDUSTRY GUIDE

PART D: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

APCON

Arista Networks

Cisco Systems

cPacket Networks

Endace

Garland Technology

Gigamon

Ixia (Keysight)

Keysight Technologies

Napatech

NETSCOUT Systems

Plixer

Profitap

Riverbed Technology

Silicom

Viavi Solutions

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |