Global Network Attached Storage (NAS) Market - Drive Bay Capacities, Deployment Types and Industry Sectors

- Published: Aug 2025

- Pages: 489 | Charts: 407

- Report Code: ITM072

SHARE THIS REPORT:

Global Network Attached Storage (NAS) Market Trends and Outlook

The global Network Attached Storage (NAS) market is witnessing a significant transformation, evolving from a niche solution to a strategic cornerstone of enterprise IT infrastructure. Valued at US$33.2 billion in 2024, the market is projected to exceed US$62.2 billion by 2030, registering a CAGR of 11%. This growth is largely fueled by the explosion of unstructured data, with enterprises across sectors capturing video, sensor, document, and AI-generated workloads that demand scalable and cost-efficient storage systems. As hybrid and multi-cloud strategies become mainstream, NAS solutions are gaining momentum for their ability to seamlessly integrate on-premise and cloud environments, simplify data management, and deliver high-performance file sharing.

Several key trends are shaping the competitive and technology landscape. The adoption of NVMe-based flash arrays is enhancing throughput for latency-sensitive applications, while AI and ML integration into NAS platforms is driving intelligent automation, predictive maintenance, and real-time optimization. Scale-out NAS architectures are on the rise, enabling enterprises to scale horizontally without disruption-particularly vital for industries managing dynamic, data-heavy workloads. Deployment models are rapidly shifting as well, with hybrid and remote NAS solutions outpacing traditional on-premise setups. Meanwhile, cybersecurity, regulatory compliance, and workload-specific performance are becoming central to procurement decisions, leading to innovation across both hardware and software-defined NAS offerings.

Leading players in the global NAS market include NetApp, Dell Technologies, Hewlett Packard Enterprise (HPE), Synology, QNAP, Qumulo, and Nasuni, each offering differentiated solutions across enterprise, SME, and hybrid cloud deployments. These vendors are continuously innovating with AI-integrated, scale-out, and cloud-native NAS platforms to meet the evolving demands of distributed and data-centric organizations.

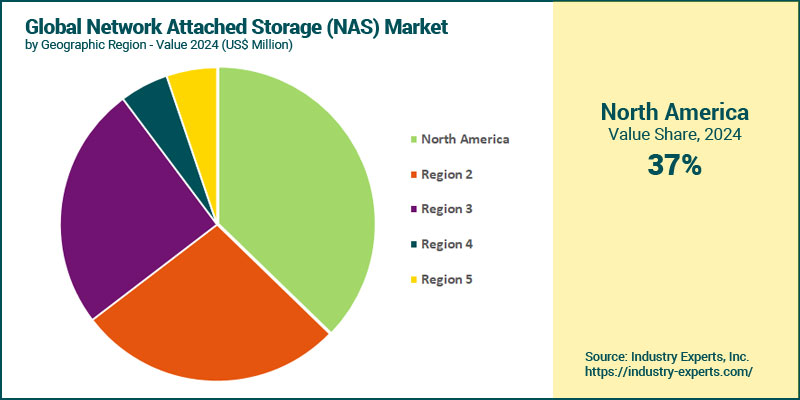

Network Attached Storage (NAS) Regional Market Analysis

In 2024, North America accounted for the largest share, contributing approximately 37.3% of global revenues. This dominant position is driven by widespread hybrid cloud adoption, modernization of legacy infrastructure, and strong demand from regulated sectors like finance and healthcare. The Asia-Pacific region is expected to emerge as the fastest-growing market, expanding at a CAGR of 14.1% and reaching US$18.5 billion by 2030. This exceptional growth is underpinned by rapid digitization across China, India, and Southeast Asia, where enterprises are investing in cloud-integrated and AI-powered NAS solutions to support surging volumes of unstructured data.

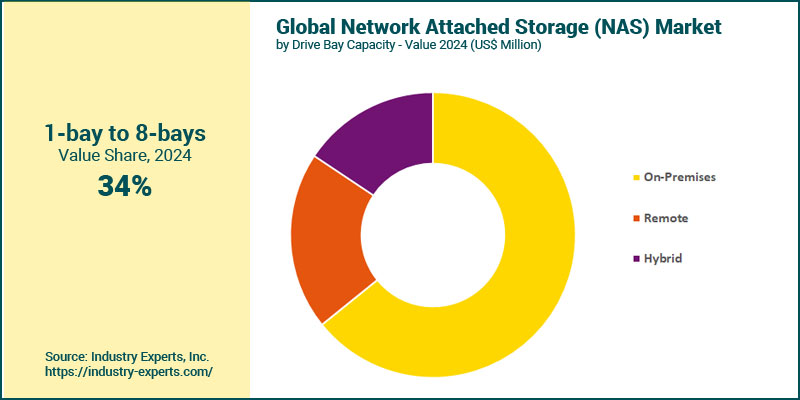

Network Attached Storage (NAS) Market Analysis by Drive Bay Capacity

The total market value for Network Attached Storage (NAS) solutions is estimated at US$33.2 billion in 2024, with systems featuring 1-bay to 8-bay drive capacity forming the largest segment, accounting for 34% of the global market. This dominance is primarily due to strong demand from small and midsize enterprises (SMEs), prosumers, and departmental use cases where cost-efficient, midrange storage with advanced functionality is prioritized. Looking ahead, NAS systems with more than 20-bays are projected to witness the fastest growth, expanding at a CAGR of 13.2% between 2024 and 2030. This surge reflects growing enterprise investment in high-capacity, scale-out NAS for data-intensive workloads such as video production, genomic research, and IoT analytics. These deployments often leverage NVMe-based architectures, advanced tiering, and AI-driven automation to deliver performance at scale. The 12-bay to 20-bay segment is also poised for strong growth, driven by larger midmarket enterprises adopting flexible NAS systems to support growing hybrid workloads.

Network Attached Storage (NAS) Market Analysis by Deployment Type

In 2024, on-premise NAS deployments remain the dominant model with 64.1% of the global market. This leading position is sustained by enterprise demand for full control over storage infrastructure, particularly in regulated industries such as healthcare, finance, and government. High-performance requirements, data sovereignty concerns, and the integration of NAS within private data centers continue to anchor demand in this segment. Meanwhile, hybrid deployments (which combine local NAS with public cloud backends) are emerging as the fastest-growing segment, projected to grow at a CAGR of 12.6% between 2024 and 2030. This rapid growth is being driven by the widespread adoption of hybrid cloud strategies, the need for cloud scalability without sacrificing local performance, and increasing reliance on NAS gateways for seamless data movement across environments. NAS solutions integrated with intelligent caching, cloud-tiering, and ransomware protection are accelerating hybrid uptake across enterprise and midmarket users.

Network Attached Storage (NAS) Market Analysis by Company Type

Large enterprises account for the majority share at 65.5% of total revenues in 2024. This leadership reflects sustained investment in high-performance, scalable storage infrastructure to support complex IT environments, petabyte-scale data volumes, and regulatory-driven compliance. Large enterprises are also increasingly adopting hybrid and software-defined NAS to enhance flexibility across geographically distributed operations. However, the SME segment is expanding at a faster pace, registering a CAGR of 12.1% during 2024-2030. The accelerated growth is driven by increasing awareness of NAS as a cost-effective alternative to traditional storage systems, coupled with the availability of entry-level and midrange appliances from vendors such as Synology, QNAP, and Asustor. SMEs are particularly drawn to NAS solutions that combine backup, file sharing, virtualization, and disaster recovery in a single platform.

Network Attached Storage (NAS) Market Analysis by Industry Sector

IT & Telecom sector emerges as the largest industry segment, generating about 19% of total market revenue in 2024. This dominant share is driven by high-performance storage requirements in data centers, cloud infrastructure management, and telecom network operations. The continuous shift to 5G, edge computing, and AI-powered services is further amplifying demand for scalable, high-throughput NAS solutions in this sector. The BFSI sector ranks second, supported by growing investments in data protection, risk analytics, and digital banking infrastructure. With compliance mandates such as PCI DSS and regional data sovereignty laws, financial institutions are turning to NAS platforms that provide encryption, immutable backups, and multi-site replication. Looking ahead, IT & Telecom is projected to remain the largest and fastest-growing vertical at a CAGR of 13.3%, while healthcare will follow, driven by rising volumes of patient data and secure archiving needs.

Network Attached Storage (NAS) Market Report Scope

This global report on Network Attached Storage (NAS) market analyzes the global and regional market based on Drive Bay Capacity, Deployment Type, Company Type and Industry Sector for the period 2021-2030 with forecasts from 2024 to 2030 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Historical Period: | 2021-2024 | |

| Base Year: | 2024 | |

| Forecast Period: | 2024-2030 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 30+ |

Network Attached Storage (NAS) Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Network Attached Storage (NAS) Market by Drive Bay Capacity

- 1-bay to 8-bays

- 8-bay to 12-bays

- 12-bay to 20-bays

- More than 20 bays

Network Attached Storage (NAS) Market by Deployment Type

- On-Premises

- Remote

- Hybrid

Network Attached Storage (NAS) Market by Company Type

- Large Enterprises

- SMEs

Network Attached Storage (NAS) Market by Industry Sector

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Media & Entertainment

- Other Industry Sectors

Network Attached Storage (NAS) Market Frequently Asked Questions (FAQs)

The NAS market is forecast to reach over US$62.2 billion by 2030, growing from US$33.2 billion in 2024 at an 11% CAGR.

North America leads the market with over US$12.4 billion in 2024, driven by hybrid cloud adoption and modernization of legacy storage.

Asia-Pacific is the fastest-growing region, expanding at a 14.1% CAGR, fueled by digital transformation in China, India, and Southeast Asia.

Key drivers include exponential unstructured data growth, hybrid IT strategies, NVMe performance, and regulatory compliance demands.

Hybrid deployments are growing the fastest at 12.6% CAGR, blending on-premise performance with cloud scalability.

SMEs are adopting NAS rapidly (12.1% CAGR), thanks to affordable, feature-rich appliances and subscription-based models from vendors like Synology and QNAP.

Trends include NVMe flash arrays, AI-integrated automation, software-defined NAS, and cloud-enabled NAS gateways for hybrid workflows.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Network Attached Storage (NAS)

- Market Segmentation for Network Attached Storage (NAS)

- Drive Bay Capacities

- Deployment Types

- Company Types

- Industry Sectors

- Key Trends in Network Attached Storage (NAS) Market

2. INDUSTRY LANDSCAPE

- Global Network Attached Storage (NAS) Market Outlook

- Comprehensive Network Attached Storage (NAS) Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Network Attached Storage (NAS) Industry

- Startup Strategies for Network Attached Storage (NAS) Industry

- SWOT Analysis of Network Attached Storage (NAS) Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Network Attached Storage (NAS) Companies

- Market Share Analysis of Network Attached Storage (NAS) Companies

- SWOT Analysis of Key Players in the Network Attached Storage (NAS) Industry

- Key Market Players

- Asustor Inc.

- Buffalo Inc.

- Ciphertex

- Cloudian

- Dell Technologies

- Drobo Inc.

- Fujitsu Ltd.

- Hewlett Packard Enterprise

- Hitachi Vantara

- Huawei Technologies Co. Ltd.

- IBM Corporation

- Infortrend Technology Inc.

- iXsystems

- LaCie

- Lenovo Group Ltd.

- Nasuni

- NEC Corp.

- NetApp Inc.

- Netgear Inc.

- Promise Technology

- Pure Storage

- QNAP Systems Inc.

- Qumulo

- Seagate Technology PLC

- Supermicro Computer Inc.

- Synology Inc.

- TerraMaster

- Thecus Technology Corp.

- TrueNAS (iXsystems)

- Western Digital Corp.

- Zyxel Communications Corp.

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Network Attached Storage (NAS) Drive Bay Capacity Market Overview by Global Region

- 1-bay to 8-bays

- 8-bay to 12-bays

- 12-bay to 20-bays

- More than 20 bays

- Global Network Attached Storage (NAS) Market Overview by Deployment Type

- Network Attached Storage (NAS) Deployment Type Market Overview by Global Region

- On-Premises

- Remote

- Hybrid

- Global Network Attached Storage (NAS) Market Overview by Company Type

- Network Attached Storage (NAS) Company Type Market Overview by Global Region

- Large Enterprises

- SMEs

- Global Network Attached Storage (NAS) Market Overview by Industry Sector

- Network Attached Storage (NAS) Industry Sector Market Overview by Global Region

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Media & Entertainment

- Other Industry Sectors

PART B: REGIONAL MARKET PERSPECTIVE

- Global Network Attached Storage (NAS) Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Network Attached Storage (NAS) Market Overview by Geographic Region

- North American Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- North American Network Attached Storage (NAS) Market Overview by Deployment Type

- North American Network Attached Storage (NAS) Market Overview by Company Type

- North American Network Attached Storage (NAS) Market Overview by Industry Sector

- Country-wise Analysis of North American Network Attached Storage (NAS) Market

- THE UNITED STATES

- United States Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- United States Network Attached Storage (NAS) Market Overview by Deployment Type

- United States Network Attached Storage (NAS) Market Overview by Company Type

- United States Network Attached Storage (NAS) Market Overview by Industry Sector

- CANADA

- Canadian Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Canadian Network Attached Storage (NAS) Market Overview by Deployment Type

- Canadian Network Attached Storage (NAS) Market Overview by Company Type

- Canadian Network Attached Storage (NAS) Market Overview by Industry Sector

- MEXICO

- Mexican Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Mexican Network Attached Storage (NAS) Market Overview by Deployment Type

- Mexican Network Attached Storage (NAS) Market Overview by Company Type

- Mexican Network Attached Storage (NAS) Market Overview by Industry Sector

7. EUROPE

- European Network Attached Storage (NAS) Market Overview by Geographic Region

- European Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- European Network Attached Storage (NAS) Market Overview by Deployment Type

- European Network Attached Storage (NAS) Market Overview by Company Type

- European Network Attached Storage (NAS) Market Overview by Industry Sector

- Country-wise Analysis of European Network Attached Storage (NAS) Market

- GERMANY

- German Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- German Network Attached Storage (NAS) Market Overview by Deployment Type

- German Network Attached Storage (NAS) Market Overview by Company Type

- German Network Attached Storage (NAS) Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- United Kingdom Network Attached Storage (NAS) Market Overview by Deployment Type

- United Kingdom Network Attached Storage (NAS) Market Overview by Company Type

- United Kingdom Network Attached Storage (NAS) Market Overview by Industry Sector

- FRANCE

- French Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- French Network Attached Storage (NAS) Market Overview by Deployment Type

- French Network Attached Storage (NAS) Market Overview by Company Type

- French Network Attached Storage (NAS) Market Overview by Industry Sector

- ITALY

- Italian Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Italian Network Attached Storage (NAS) Market Overview by Deployment Type

- Italian Network Attached Storage (NAS) Market Overview by Company Type

- Italian Network Attached Storage (NAS) Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Dutch Network Attached Storage (NAS) Market Overview by Deployment Type

- Dutch Network Attached Storage (NAS) Market Overview by Company Type

- Dutch Network Attached Storage (NAS) Market Overview by Industry Sector

- SPAIN

- Spanish Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Spanish Network Attached Storage (NAS) Market Overview by Deployment Type

- Spanish Network Attached Storage (NAS) Market Overview by Company Type

- Spanish Network Attached Storage (NAS) Market Overview by Industry Sector

- RUSSIA

- Russian Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Russian Network Attached Storage (NAS) Market Overview by Deployment Type

- Russian Network Attached Storage (NAS) Market Overview by Company Type

- Russian Network Attached Storage (NAS) Market Overview by Industry Sector

- SWITZERLAND

- Swiss Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Swiss Network Attached Storage (NAS) Market Overview by Deployment Type

- Swiss Network Attached Storage (NAS) Market Overview by Company Type

- Swiss Network Attached Storage (NAS) Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Rest of Europe Network Attached Storage (NAS) Market Overview by Deployment Type

- Rest of Europe Network Attached Storage (NAS) Market Overview by Company Type

- Rest of Europe Network Attached Storage (NAS) Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Network Attached Storage (NAS) Market Overview by Geographic Region

- Asia-Pacific Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Asia-Pacific Network Attached Storage (NAS) Market Overview by Deployment Type

- Asia-Pacific Network Attached Storage (NAS) Market Overview by Company Type

- Asia-Pacific Network Attached Storage (NAS) Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Network Attached Storage (NAS) Market

- CHINA

- Chinese Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Chinese Network Attached Storage (NAS) Market Overview by Deployment Type

- Chinese Network Attached Storage (NAS) Market Overview by Company Type

- Chinese Network Attached Storage (NAS) Market Overview by Industry Sector

- JAPAN

- Japanese Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Japanese Network Attached Storage (NAS) Market Overview by Deployment Type

- Japanese Network Attached Storage (NAS) Market Overview by Company Type

- Japanese Network Attached Storage (NAS) Market Overview by Industry Sector

- INDIA

- Indian Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Indian Network Attached Storage (NAS) Market Overview by Deployment Type

- Indian Network Attached Storage (NAS) Market Overview by Company Type

- Indian Network Attached Storage (NAS) Market Overview by Industry Sector

- AUSTRALIA

- Australia Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Australia Network Attached Storage (NAS) Market Overview by Deployment Type

- Australia Network Attached Storage (NAS) Market Overview by Company Type

- Australia Network Attached Storage (NAS) Market Overview by Industry Sector

- SINGAPORE

- Singaporean Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Singaporean Network Attached Storage (NAS) Market Overview by Deployment Type

- Singaporean Network Attached Storage (NAS) Market Overview by Company Type

- Singaporean Network Attached Storage (NAS) Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- South Korean Network Attached Storage (NAS) Market Overview by Deployment Type

- South Korean Network Attached Storage (NAS) Market Overview by Company Type

- South Korean Network Attached Storage (NAS) Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Rest of Asia-Pacific Network Attached Storage (NAS) Market Overview by Deployment Type

- Rest of Asia-Pacific Network Attached Storage (NAS) Market Overview by Company Type

- Rest of Asia-Pacific Network Attached Storage (NAS) Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Network Attached Storage (NAS) Market Overview by Geographic Region

- South American Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- South American Network Attached Storage (NAS) Market Overview by Deployment Type

- South American Network Attached Storage (NAS) Market Overview by Company Type

- South American Network Attached Storage (NAS) Market Overview by Industry Sector

- Country-wise Analysis of South American Network Attached Storage (NAS) Market

- BRAZIL

- Brazilian Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Brazilian Network Attached Storage (NAS) Market Overview by Deployment Type

- Brazilian Network Attached Storage (NAS) Market Overview by Company Type

- Brazilian Network Attached Storage (NAS) Market Overview by Industry Sector

- ARGENTINA

- Argentine Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Argentine Network Attached Storage (NAS) Market Overview by Deployment Type

- Argentine Network Attached Storage (NAS) Market Overview by Company Type

- Argentine Network Attached Storage (NAS) Market Overview by Industry Sector

- COLOMBIA

- Colombian Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Colombian Network Attached Storage (NAS) Market Overview by Deployment Type

- Colombian Network Attached Storage (NAS) Market Overview by Company Type

- Colombian Network Attached Storage (NAS) Market Overview by Industry Sector

- CHILE

- Chilean Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Chilean Network Attached Storage (NAS) Market Overview by Deployment Type

- Chilean Network Attached Storage (NAS) Market Overview by Company Type

- Chilean Network Attached Storage (NAS) Market Overview by Industry Sector

- PERU

- Peruvian Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Peruvian Network Attached Storage (NAS) Market Overview by Deployment Type

- Peruvian Network Attached Storage (NAS) Market Overview by Company Type

- Peruvian Network Attached Storage (NAS) Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Rest of South America Network Attached Storage (NAS) Market Overview by Deployment Type

- Rest of South America Network Attached Storage (NAS) Market Overview by Company Type

- Rest of South America Network Attached Storage (NAS) Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Network Attached Storage (NAS) Market Overview by Geographic Region

- Middle East & Africa Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Middle East & Africa Network Attached Storage (NAS) Market Overview by Deployment Type

- Middle East & Africa Network Attached Storage (NAS) Market Overview by Company Type

- Middle East & Africa Network Attached Storage (NAS) Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Network Attached Storage (NAS) Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- United Arab Emirates Network Attached Storage (NAS) Market Overview by Deployment Type

- United Arab Emirates Network Attached Storage (NAS) Market Overview by Company Type

- United Arab Emirates Network Attached Storage (NAS) Market Overview by Industry Sector

- SOUTH AFRICA

- South African Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- South African Network Attached Storage (NAS) Market Overview by Deployment Type

- South African Network Attached Storage (NAS) Market Overview by Company Type

- South African Network Attached Storage (NAS) Market Overview by Industry Sector

- EGYPT

- Egyptian Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Egyptian Network Attached Storage (NAS) Market Overview by Deployment Type

- Egyptian Network Attached Storage (NAS) Market Overview by Company Type

- Egyptian Network Attached Storage (NAS) Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Saudi Arabian Network Attached Storage (NAS) Market Overview by Deployment Type

- Saudi Arabian Network Attached Storage (NAS) Market Overview by Company Type

- Saudi Arabian Network Attached Storage (NAS) Market Overview by Industry Sector

- MOROCCO

- Moroccan Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Moroccan Network Attached Storage (NAS) Market Overview by Deployment Type

- Moroccan Network Attached Storage (NAS) Market Overview by Company Type

- Moroccan Network Attached Storage (NAS) Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Kuwaiti Network Attached Storage (NAS) Market Overview by Deployment Type

- Kuwaiti Network Attached Storage (NAS) Market Overview by Company Type

- Kuwaiti Network Attached Storage (NAS) Market Overview by Industry Sector

- QATAR

- Qatari Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Qatari Network Attached Storage (NAS) Market Overview by Deployment Type

- Qatari Network Attached Storage (NAS) Market Overview by Company Type

- Qatari Network Attached Storage (NAS) Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Network Attached Storage (NAS) Market Overview by Drive Bay Capacity

- Rest of Middle East & Africa Network Attached Storage (NAS) Market Overview by Deployment Type

- Rest of Middle East & Africa Network Attached Storage (NAS) Market Overview by Company Type

- Rest of Middle East & Africa Network Attached Storage (NAS) Market Overview by Industry Sector

PART C: INDUSTRY GUIDE

PART D: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

Asustor Inc.

Buffalo Inc.

Ciphertex

Cloudian

Dell Technologies

Drobo Inc.

Fujitsu Ltd.

Hewlett Packard Enterprise

Hitachi Vantara

Huawei Technologies Co. Ltd.

IBM Corporation

Infortrend Technology Inc.

iXsystems

LaCie

Lenovo Group Ltd.

Nasuni

NEC Corp.

NetApp Inc.

Netgear Inc.

Promise Technology

Pure Storage

QNAP Systems Inc.

Qumulo

Seagate Technology PLC

Supermicro Computer Inc.

Synology Inc.

TerraMaster

Thecus Technology Corp.

TrueNAS (iXsystems)

Western Digital Corp.

Zyxel Communications Corp.

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |