Mobile Device Management (MDM) Software - A Global Market Overview

- Published: Aug 2025

- Pages: 573 | Charts: 496

- Report Code: ITM053

SHARE THIS REPORT:

Global Mobile Device Management (MDM) Software Market Trends and Outlook

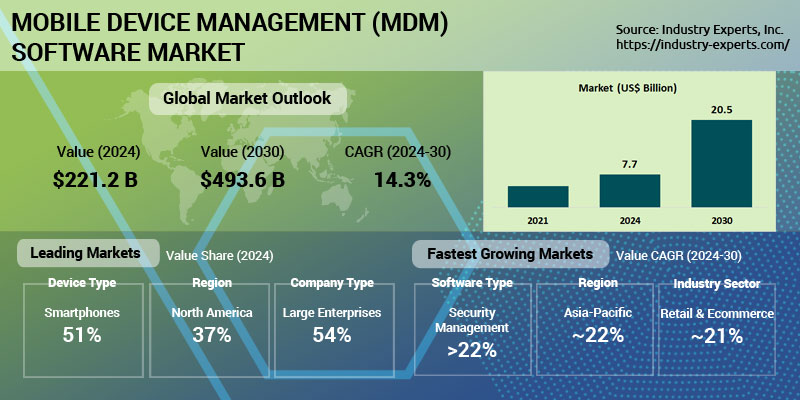

The global Mobile Device Management (MDM) software market is entering a transformative era marked by rapid digitization, intensified security demands, and cloud-native innovation. Valued at approximately US$7.7 billion in 2024, the market is projected to exceed US$20 billion by 2030, expanding at a strong CAGR of 17.6%. This growth is fuelled by the accelerating adoption of hybrid work models, expanding regulatory scrutiny, and the proliferation of mobile and endpoint devices across verticals and geographies.

MDM software is evolving beyond core device provisioning into comprehensive platforms integrating AI-powered threat detection, Zero Trust enforcement, and real-time compliance automation. Cloud-native delivery dominates, accounting for over 65% of deployments in 2024, as enterprises and SMEs alike seek scalable, subscription-based security solutions. As mobile phishing threats surge and endpoints diversify, vendors capable of delivering unified, intelligent, and flexible platforms will define the competitive landscape in the years ahead.

Leading players in the MDM software market include Microsoft (Intune), VMware (Workspace ONE), IBM (MaaS360), Ivanti, Jamf, Hexnode, Scalefusion, and Citrix. These vendors are shaping the industry by integrating MDM into broader endpoint security suites and offering SaaS-based, AI-augmented capabilities.

Mobile Device Management (MDM) Software Regional Market Analysis

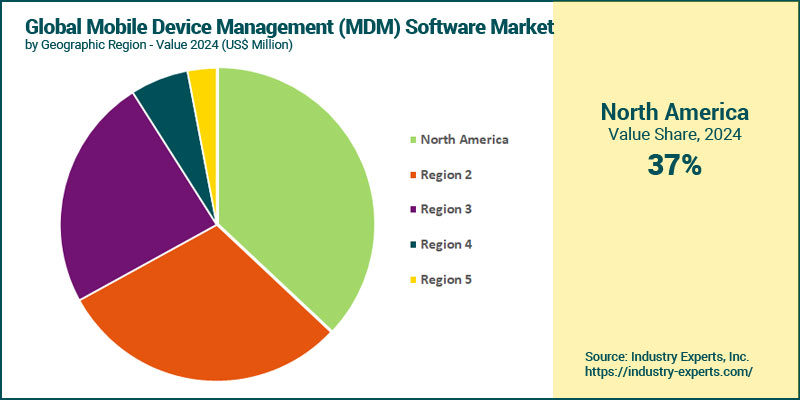

In 2024, North America accounted for the largest share of the global MDM software market, contributing approximately US$2.9 billion, or around 37% of the global total. The region's dominance stems from early cloud adoption, a mature enterprise IT environment, and regulatory mandates driving security-centric deployments. Europe followed closely behind, supported by rising compliance investments across the EU, especially due to GDPR and emerging cybersecurity directives. Asia Pacific is projected to be the fastest-growing regional market between 2024 and 2030, registering a CAGR of 22.1%. This rapid growth is propelled by widespread mobile-first enterprise digitization across China, India, and Southeast Asia, alongside growing SME adoption of SaaS-based endpoint control platforms.

Mobile Device Management (MDM) Software Market Analysis by Software Type

As of 2024, Device Management remained the largest segment, accounting for nearly 46.5% of the global MDM software market. This dominance reflects the foundational role of device enrollment, policy enforcement, and remote wipe capabilities in MDM deployments. However, Security Management is the fastest-growing category, expanding at a CAGR of 22.2% between 2024 and 2030. This is driven by rising threats like mobile ransomware, phishing, and the increased need for Zero Trust architectures. Application Management follows with a robust CAGR of 20.3%, propelled by the need to control and secure app usage across corporate and BYOD environments.

Mobile Device Management (MDM) Software Market Analysis by Device Type

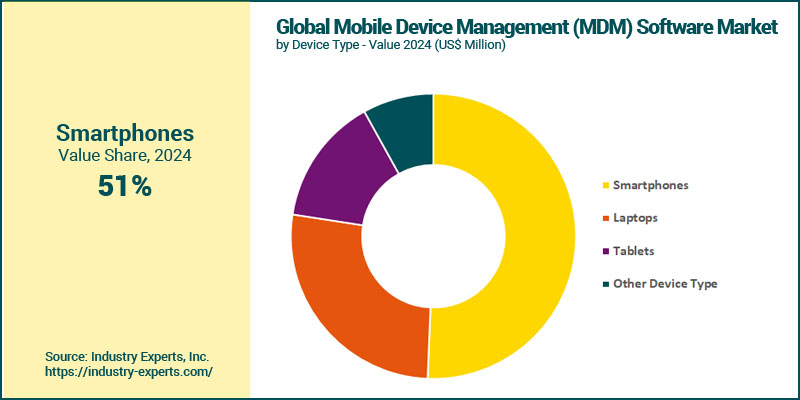

Smartphones led the market in 2024 with a value of US$3.9 billion, contributing nearly 50.7% of global revenue. This leadership is attributed to their ubiquity in enterprise mobility, particularly in hybrid and remote work models. However, Laptops represent the fastest-growing device type, expanding at a CAGR of 19.4% to reach US$6.0 billion by 2030. Enterprises are increasingly including laptops in MDM workflows to achieve unified endpoint management and streamline policy governance across all device types.

Mobile Device Management (MDM) Software Market Analysis by Deployment Type

Cloud-based deployment is the dominant and fastest-growing model, valued at US$4.7 billion in 2024 and expected to surpass US$13.5 billion by 2030, registering a CAGR of 19.4%. This preference is fuelled by the scalability, cost-effectiveness, and ease of implementation of SaaS-based MDM solutions, particularly among SMEs and globally distributed enterprises. On-premise models are still relevant in highly regulated industries but grow at a slower CAGR of 14.6%.

Mobile Device Management (MDM) Software Market Analysis by Company Type

Large enterprises accounted for a larger market share in 2024 at US$4.16 billion, but SMEs are expanding more rapidly with a CAGR of 19.1% through 2030. By the end of the forecast period, SMEs are projected to generate over US$10.1 billion, nearly reaching parity with large enterprises. Growing SaaS availability, modular pricing, and device proliferation in mid-sized firms are driving this trend.

Mobile Device Management (MDM) Software Market Analysis by Industry Sector

The IT & Telecom industry led the MDM software market in 2024. This leadership reflects the sector's high mobile workforce density, rapid device refresh cycles, and ongoing investment in secure endpoint management across globally distributed teams. Healthcare, while growing fast, ranked second in size. Retail & E-commerce emerged as the fastest-growing vertical during the forecast period of 2024-2030, with a CAGR of 20.8%, driven by widespread deployment of mobile POS systems, rugged handhelds in warehouses, and app-based retail operations. Healthcare is the second fastest-growing segment, supported by compliance-driven device adoption and secure mobility solutions for clinicians and administrative staff.

Mobile Device Management (MDM) Software Market Report Scope

This global report on Mobile Device Management (MDM) Software market analyzes the global and regional market based on Software Type, Device Type, Deployment Type, Company Type and Industry Sector for the period 2021-2030 with forecasts from 2024 to 2030 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Historical Period: | 2021-2024 | |

| Base Year: | 2024 | |

| Forecast Period: | 2024-2030 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 25+ |

Mobile Device Management (MDM) Software Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Mobile Device Management (MDM) Software Market by Software Type

- Device Management

- Application Management (MAM)

- Content Management (MCM)

- Security Management

- Email Management

- Other Software Types

Mobile Device Management (MDM) Software Market by Device Type

- Smartphones

- Laptops

- Tablets

- Other Device Type

Mobile Device Management (MDM) Software Market by Deployment Type

- Cloud

- On-Premises

Mobile Device Management (MDM) Software Market by Company Type

- Large Enterprises

- SMEs

Mobile Device Management (MDM) Software Market by Industry Sector

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

Mobile Device Management (MDM) Software Market Frequently Asked Questions (FAQs)

The MDM software market was valued at approximately US$7.7 billion in 2024.

The market is projected to grow at a CAGR of 17.6% between 2024 and 2030, reaching over US$20 billion by 2030.

North America leads with the largest revenue share in 2024, driven by mature IT infrastructure and cloud adoption.

Asia Pacific is the fastest-growing region, expected to grow at a CAGR of 22.1% during 2024-2030.

Cloud deployment is dominant, making up over 65% of global MDM deployments in 2024 and expanding at 19.4% CAGR.

Key drivers include hybrid work models, regulatory compliance (e.g., GDPR, HIPAA), rising mobile threats, and cloud-native SaaS platforms.

Key players include Microsoft, VMware, IBM, Ivanti, Jamf, Hexnode, Scalefusion, Citrix, and Samsung.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Mobile Device Management (MDM) Software

- Market Segmentation for Mobile Device Management (MDM) Software

- Software Types

- Device Types

- Deployment Types

- Company Types

- Industry Sectors

- Key Trends in Mobile Device Management (MDM) Software Market

2. INDUSTRY LANDSCAPE

- Global Mobile Device Management (MDM) Software Market Outlook

- Comprehensive Mobile Device Management (MDM) Software Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Mobile Device Management (MDM) Software Industry

- Startup Strategies for Mobile Device Management (MDM) Software Industry

- SWOT Analysis of Mobile Device Management (MDM) Software Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Mobile Device Management (MDM) Software Companies

- Market Share Analysis of Mobile Device Management (MDM) Software Companies

- SWOT Analysis of Key Players in the Mobile Device Management (MDM) Software Industry

- Key Market Players

- Blackberry Ltd.

- Broadcom, Inc.

- Checkpoint Software Technologies Ltd.

- Cisco Systems

- Citrix Systems

- Codeproof Technologies Inc.

- Hexnode

- IBM Corporation

- Ivanti

- Jamf

- Kaspersky Labs

- Micro Focus

- Microsoft Corporation

- Miradore Ltd.

- Mobilerlon, Inc.

- Qualys

- Quest Software

- Rippling

- Samsung

- SAP SE

- Scalefusion

- Snow Software

- SolarWinds Worldwide, LLC.

- Sophos

- SOTI Inc.

- VMware, Inc.

- Zoho Corp. Pvt. Ltd.

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Mobile Device Management (MDM) Software Market Overview by Type

- Mobile Device Management (MDM) Software Type Market Overview by Global Region

- Device Management

- Application Management (MAM)

- Content Management (MCM)

- Security Management

- Email Management

- Other Software Types

- Global Mobile Device Management (MDM) Software Market Overview by Device Type

- Mobile Device Management (MDM) Software Device Type Market Overview by Global Region

- Smartphones

- Laptops

- Tablets

- Other Device Type

- Global Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Mobile Device Management (MDM) Software Deployment Type Market Overview by Global Region

- Cloud

- On-Premises

- Global Mobile Device Management (MDM) Software Market Overview by Company Type

- Mobile Device Management (MDM) Software Company Type Market Overview by Global Region

- Large Enterprises

- SMEs

- Global Mobile Device Management (MDM) Software Market Overview by Industry Sector

- Mobile Device Management (MDM) Software Industry Sector Market Overview by Global Region

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

PART B: REGIONAL MARKET PERSPECTIVE

- Global Mobile Device Management (MDM) Software Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Mobile Device Management (MDM) Software Market Overview by Geographic Region

- North American Mobile Device Management (MDM) Software Market Overview by Software Type

- North American Mobile Device Management (MDM) Software Market Overview by Device Type

- North American Mobile Device Management (MDM) Software Market Overview by Deployment Type

- North American Mobile Device Management (MDM) Software Market Overview by Company Type

- North American Mobile Device Management (MDM) Software Market Overview by Industry Sector

- Country-wise Analysis of North American Mobile Device Management (MDM) Software Market

- THE UNITED STATES

- United States Mobile Device Management (MDM) Software Market Overview by Software Type

- United States Mobile Device Management (MDM) Software Market Overview by Device Type

- United States Mobile Device Management (MDM) Software Market Overview by Deployment Type

- United States Mobile Device Management (MDM) Software Market Overview by Company Type

- United States Mobile Device Management (MDM) Software Market Overview by Industry Sector

- CANADA

- Canadian Mobile Device Management (MDM) Software Market Overview by Software Type

- Canadian Mobile Device Management (MDM) Software Market Overview by Device Type

- Canadian Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Canadian Mobile Device Management (MDM) Software Market Overview by Company Type

- Canadian Mobile Device Management (MDM) Software Market Overview by Industry Sector

- MEXICO

- Mexican Mobile Device Management (MDM) Software Market Overview by Software Type

- Mexican Mobile Device Management (MDM) Software Market Overview by Device Type

- Mexican Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Mexican Mobile Device Management (MDM) Software Market Overview by Company Type

- Mexican Mobile Device Management (MDM) Software Market Overview by Industry Sector

7. EUROPE

- European Mobile Device Management (MDM) Software Market Overview by Geographic Region

- European Mobile Device Management (MDM) Software Market Overview by Software Type

- European Mobile Device Management (MDM) Software Market Overview by Device Type

- European Mobile Device Management (MDM) Software Market Overview by Deployment Type

- European Mobile Device Management (MDM) Software Market Overview by Company Type

- European Mobile Device Management (MDM) Software Market Overview by Industry Sector

- Country-wise Analysis of European Mobile Device Management (MDM) Software Market

- GERMANY

- German Mobile Device Management (MDM) Software Market Overview by Software Type

- German Mobile Device Management (MDM) Software Market Overview by Device Type

- German Mobile Device Management (MDM) Software Market Overview by Deployment Type

- German Mobile Device Management (MDM) Software Market Overview by Company Type

- German Mobile Device Management (MDM) Software Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Mobile Device Management (MDM) Software Market Overview by Software Type

- United Kingdom Mobile Device Management (MDM) Software Market Overview by Device Type

- United Kingdom Mobile Device Management (MDM) Software Market Overview by Deployment Type

- United Kingdom Mobile Device Management (MDM) Software Market Overview by Company Type

- United Kingdom Mobile Device Management (MDM) Software Market Overview by Industry Sector

- FRANCE

- French Mobile Device Management (MDM) Software Market Overview by Software Type

- French Mobile Device Management (MDM) Software Market Overview by Device Type

- French Mobile Device Management (MDM) Software Market Overview by Deployment Type

- French Mobile Device Management (MDM) Software Market Overview by Company Type

- French Mobile Device Management (MDM) Software Market Overview by Industry Sector

- ITALY

- Italian Mobile Device Management (MDM) Software Market Overview by Software Type

- Italian Mobile Device Management (MDM) Software Market Overview by Device Type

- Italian Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Italian Mobile Device Management (MDM) Software Market Overview by Company Type

- Italian Mobile Device Management (MDM) Software Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Mobile Device Management (MDM) Software Market Overview by Software Type

- Dutch Mobile Device Management (MDM) Software Market Overview by Device Type

- Dutch Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Dutch Mobile Device Management (MDM) Software Market Overview by Company Type

- Dutch Mobile Device Management (MDM) Software Market Overview by Industry Sector

- SPAIN

- Spanish Mobile Device Management (MDM) Software Market Overview by Software Type

- Spanish Mobile Device Management (MDM) Software Market Overview by Device Type

- Spanish Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Spanish Mobile Device Management (MDM) Software Market Overview by Company Type

- Spanish Mobile Device Management (MDM) Software Market Overview by Industry Sector

- RUSSIA

- Russian Mobile Device Management (MDM) Software Market Overview by Software Type

- Russian Mobile Device Management (MDM) Software Market Overview by Device Type

- Russian Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Russian Mobile Device Management (MDM) Software Market Overview by Company Type

- Russian Mobile Device Management (MDM) Software Market Overview by Industry Sector

- SWITZERLAND

- Swiss Mobile Device Management (MDM) Software Market Overview by Software Type

- Swiss Mobile Device Management (MDM) Software Market Overview by Device Type

- Swiss Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Swiss Mobile Device Management (MDM) Software Market Overview by Company Type

- Swiss Mobile Device Management (MDM) Software Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Mobile Device Management (MDM) Software Market Overview by Software Type

- Rest of Europe Mobile Device Management (MDM) Software Market Overview by Device Type

- Rest of Europe Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Rest of Europe Mobile Device Management (MDM) Software Market Overview by Company Type

- Rest of Europe Mobile Device Management (MDM) Software Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Mobile Device Management (MDM) Software Market Overview by Geographic Region

- Asia-Pacific Mobile Device Management (MDM) Software Market Overview by Software Type

- Asia-Pacific Mobile Device Management (MDM) Software Market Overview by Device Type

- Asia-Pacific Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Asia-Pacific Mobile Device Management (MDM) Software Market Overview by Company Type

- Asia-Pacific Mobile Device Management (MDM) Software Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Mobile Device Management (MDM) Software Market

- CHINA

- Chinese Mobile Device Management (MDM) Software Market Overview by Software Type

- Chinese Mobile Device Management (MDM) Software Market Overview by Device Type

- Chinese Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Chinese Mobile Device Management (MDM) Software Market Overview by Company Type

- Chinese Mobile Device Management (MDM) Software Market Overview by Industry Sector

- JAPAN

- Japanese Mobile Device Management (MDM) Software Market Overview by Software Type

- Japanese Mobile Device Management (MDM) Software Market Overview by Device Type

- Japanese Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Japanese Mobile Device Management (MDM) Software Market Overview by Company Type

- Japanese Mobile Device Management (MDM) Software Market Overview by Industry Sector

- INDIA

- Indian Mobile Device Management (MDM) Software Market Overview by Software Type

- Indian Mobile Device Management (MDM) Software Market Overview by Device Type

- Indian Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Indian Mobile Device Management (MDM) Software Market Overview by Company Type

- Indian Mobile Device Management (MDM) Software Market Overview by Industry Sector

- AUSTRALIA

- Australia Mobile Device Management (MDM) Software Market Overview by Software Type

- Australia Mobile Device Management (MDM) Software Market Overview by Device Type

- Australia Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Australia Mobile Device Management (MDM) Software Market Overview by Company Type

- Australia Mobile Device Management (MDM) Software Market Overview by Industry Sector

- SINGAPORE

- Singaporean Mobile Device Management (MDM) Software Market Overview by Software Type

- Singaporean Mobile Device Management (MDM) Software Market Overview by Device Type

- Singaporean Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Singaporean Mobile Device Management (MDM) Software Market Overview by Company Type

- Singaporean Mobile Device Management (MDM) Software Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Mobile Device Management (MDM) Software Market Overview by Software Type

- South Korean Mobile Device Management (MDM) Software Market Overview by Device Type

- South Korean Mobile Device Management (MDM) Software Market Overview by Deployment Type

- South Korean Mobile Device Management (MDM) Software Market Overview by Company Type

- South Korean Mobile Device Management (MDM) Software Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Mobile Device Management (MDM) Software Market Overview by Software Type

- Rest of Asia-Pacific Mobile Device Management (MDM) Software Market Overview by Device Type

- Rest of Asia-Pacific Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Rest of Asia-Pacific Mobile Device Management (MDM) Software Market Overview by Company Type

- Rest of Asia-Pacific Mobile Device Management (MDM) Software Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Mobile Device Management (MDM) Software Market Overview by Geographic Region

- South American Mobile Device Management (MDM) Software Market Overview by Software Type

- South American Mobile Device Management (MDM) Software Market Overview by Device Type

- South American Mobile Device Management (MDM) Software Market Overview by Deployment Type

- South American Mobile Device Management (MDM) Software Market Overview by Company Type

- South American Mobile Device Management (MDM) Software Market Overview by Industry Sector

- Country-wise Analysis of South American Mobile Device Management (MDM) Software Market

- BRAZIL

- Brazilian Mobile Device Management (MDM) Software Market Overview by Software Type

- Brazilian Mobile Device Management (MDM) Software Market Overview by Device Type

- Brazilian Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Brazilian Mobile Device Management (MDM) Software Market Overview by Company Type

- Brazilian Mobile Device Management (MDM) Software Market Overview by Industry Sector

- ARGENTINA

- Argentine Mobile Device Management (MDM) Software Market Overview by Software Type

- Argentine Mobile Device Management (MDM) Software Market Overview by Device Type

- Argentine Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Argentine Mobile Device Management (MDM) Software Market Overview by Company Type

- Argentine Mobile Device Management (MDM) Software Market Overview by Industry Sector

- COLOMBIA

- Colombian Mobile Device Management (MDM) Software Market Overview by Software Type

- Colombian Mobile Device Management (MDM) Software Market Overview by Device Type

- Colombian Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Colombian Mobile Device Management (MDM) Software Market Overview by Company Type

- Colombian Mobile Device Management (MDM) Software Market Overview by Industry Sector

- CHILE

- Chilean Mobile Device Management (MDM) Software Market Overview by Software Type

- Chilean Mobile Device Management (MDM) Software Market Overview by Device Type

- Chilean Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Chilean Mobile Device Management (MDM) Software Market Overview by Company Type

- Chilean Mobile Device Management (MDM) Software Market Overview by Industry Sector

- PERU

- Peruvian Mobile Device Management (MDM) Software Market Overview by Software Type

- Peruvian Mobile Device Management (MDM) Software Market Overview by Device Type

- Peruvian Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Peruvian Mobile Device Management (MDM) Software Market Overview by Company Type

- Peruvian Mobile Device Management (MDM) Software Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Mobile Device Management (MDM) Software Market Overview by Software Type

- Rest of South America Mobile Device Management (MDM) Software Market Overview by Device Type

- Rest of South America Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Rest of South America Mobile Device Management (MDM) Software Market Overview by Company Type

- Rest of South America Mobile Device Management (MDM) Software Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Mobile Device Management (MDM) Software Market Overview by Geographic Region

- Middle East & Africa Mobile Device Management (MDM) Software Market Overview by Software Type

- Middle East & Africa Mobile Device Management (MDM) Software Market Overview by Device Type

- Middle East & Africa Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Middle East & Africa Mobile Device Management (MDM) Software Market Overview by Company Type

- Middle East & Africa Mobile Device Management (MDM) Software Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Mobile Device Management (MDM) Software Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Mobile Device Management (MDM) Software Market Overview by Software Type

- United Arab Emirates Mobile Device Management (MDM) Software Market Overview by Device Type

- United Arab Emirates Mobile Device Management (MDM) Software Market Overview by Deployment Type

- United Arab Emirates Mobile Device Management (MDM) Software Market Overview by Company Type

- United Arab Emirates Mobile Device Management (MDM) Software Market Overview by Industry Sector

- SOUTH AFRICA

- South African Mobile Device Management (MDM) Software Market Overview by Software Type

- South African Mobile Device Management (MDM) Software Market Overview by Device Type

- South African Mobile Device Management (MDM) Software Market Overview by Deployment Type

- South African Mobile Device Management (MDM) Software Market Overview by Company Type

- South African Mobile Device Management (MDM) Software Market Overview by Industry Sector

- EGYPT

- Egyptian Mobile Device Management (MDM) Software Market Overview by Software Type

- Egyptian Mobile Device Management (MDM) Software Market Overview by Device Type

- Egyptian Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Egyptian Mobile Device Management (MDM) Software Market Overview by Company Type

- Egyptian Mobile Device Management (MDM) Software Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Mobile Device Management (MDM) Software Market Overview by Software Type

- Saudi Arabian Mobile Device Management (MDM) Software Market Overview by Device Type

- Saudi Arabian Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Saudi Arabian Mobile Device Management (MDM) Software Market Overview by Company Type

- Saudi Arabian Mobile Device Management (MDM) Software Market Overview by Industry Sector

- MOROCCO

- Moroccan Mobile Device Management (MDM) Software Market Overview by Software Type

- Moroccan Mobile Device Management (MDM) Software Market Overview by Device Type

- Moroccan Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Moroccan Mobile Device Management (MDM) Software Market Overview by Company Type

- Moroccan Mobile Device Management (MDM) Software Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Mobile Device Management (MDM) Software Market Overview by Software Type

- Kuwaiti Mobile Device Management (MDM) Software Market Overview by Device Type

- Kuwaiti Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Kuwaiti Mobile Device Management (MDM) Software Market Overview by Company Type

- Kuwaiti Mobile Device Management (MDM) Software Market Overview by Industry Sector

- QATAR

- Qatari Mobile Device Management (MDM) Software Market Overview by Software Type

- Qatari Mobile Device Management (MDM) Software Market Overview by Device Type

- Qatari Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Qatari Mobile Device Management (MDM) Software Market Overview by Company Type

- Qatari Mobile Device Management (MDM) Software Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Mobile Device Management (MDM) Software Market Overview by Software Type

- Rest of Middle East & Africa Mobile Device Management (MDM) Software Market Overview by Device Type

- Rest of Middle East & Africa Mobile Device Management (MDM) Software Market Overview by Deployment Type

- Rest of Middle East & Africa Mobile Device Management (MDM) Software Market Overview by Company Type

- Rest of Middle East & Africa Mobile Device Management (MDM) Software Market Overview by Industry Sector

PART C: INDUSTRY GUIDE

PART D: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

Blackberry Ltd.

Broadcom, Inc.

Checkpoint Software Technologies Ltd.

Cisco Systems

Citrix Systems

Codeproof Technologies Inc.

Google

Hexnode

IBM Corporation

Ivanti

Jamf

Kaspersky Labs

Micro Focus

Microsoft Corporation

Miradore Ltd.

Mobilerlon, Inc.

Qualys

Quest Software

Rippling

Samsung

SAP SE

Scalefusion

Snow Software

SolarWinds Worldwide, LLC.

Sophos

SOTI Inc.

VMware, Inc.

Zoho Corp. Pvt. Ltd.

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |