Managed Security Services (MSS) - A Global Market Overview

- Published: Aug 2025

- Pages: 597 | Charts: 496

- Report Code: ITM028

SHARE THIS REPORT:

Global Managed Security Services (MSS) Market Trends and Outlook

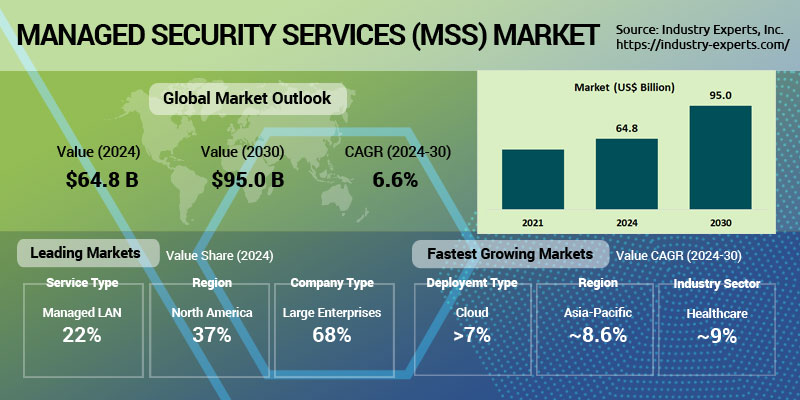

The global Managed Security Services (MSS) market is undergoing a transformative shift, fueled by intensifying cyber threats, regulatory mandates, and a chronic shortage of skilled cybersecurity professionals. Valued at approximately US$33.01 billion in 2024, the market is projected to surpass US$62 billion by 2030, expanding at a compound annual growth rate (CAGR) of 11.1%. While demand remains strongest in North America, driven by early adoption across financial services, healthcare, and government sectors, the Asia-Pacific region is poised for the fastest growth, underpinned by rising enterprise digitization, public cloud adoption, and national cybersecurity initiatives in countries such as India and China. Global MSS revenue will also be shaped by growing uptake in emerging economies like Brazil and Saudi Arabia, where governments are increasingly outsourcing SOC capabilities to counter rising ransomware and third-party supply chain risks.

The MSS landscape is being reshaped by the convergence of technologies and service models. Enterprises are shifting from traditional log monitoring to advanced capabilities such as Managed Detection and Response (MDR), Zero Trust orchestration, and XDR frameworks. Regulatory frameworks such as GDPR, HIPAA, NIS2, CCPA, and DORA are not only catalyzing demand for managed compliance services but also creating operational complexity for MSSPs, who must navigate data localization and audit readiness across jurisdictions. Meanwhile, the acceleration of cloud-native adoption has intensified demand for services like Cloud Security Posture Management (CSPM), container security, and real-time threat remediation. As the cyber insurance market tightens, MSS is also becoming a prerequisite for policy eligibility, particularly among SMEs. Together, these dynamics are solidifying MSS as a foundational component of modern cybersecurity strategy, with platform-based, outcome-driven delivery models emerging as the future of the market.

Leading players in the global Managed Security Services (MSS) market include IBM, Atos, BT, Verizon, SecureWorks, and AT&T, alongside fast-growing specialists like Arctic Wolf, eSentire, and Rapid7. Cloud and security giants such as Microsoft, AWS, Palo Alto Networks, Check Point, and CrowdStrike are also expanding their MSS portfolios, reshaping competition through platform-based and cloud-native offerings.

Managed Security Services (MSS) Regional Market Analysis

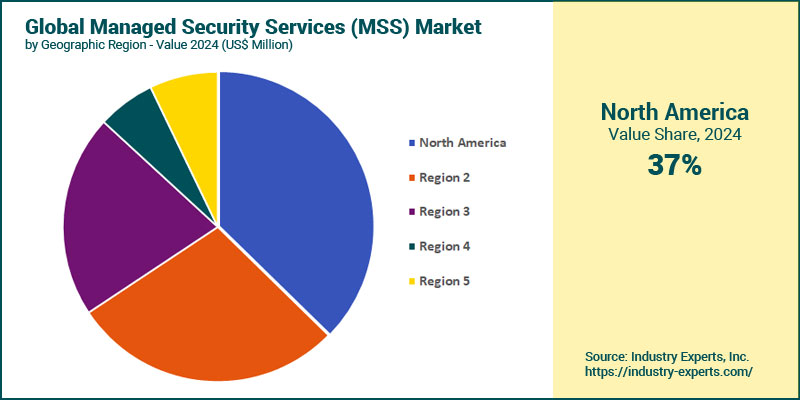

North America remains the largest regional market throughout the forecast period. In 2024, the region accounted for 37.8% of global MSS revenue. The region is expected to reach nearly US$33.4 billion by 2030. Growth in North America is driven by early MSS adoption in banking, healthcare, and government sectors, along with increasing demand for co-managed SOCs among large enterprises and regulatory compliance with frameworks like HIPAA, CCPA, and NIST. Asia-Pacific is projected to be the fastest-growing region, registering a CAGR of 8.6% between 2024 and 2030. This rapid growth is attributed to increased cloud adoption, rising cyberattacks on public infrastructure, and expanding regulatory regimes across China, India, and ASEAN countries. National cybersecurity initiatives and demand for cloud-native MDR solutions are reshaping regional MSS procurement.

Managed Security Services (MSS) Market Analysis by Service Type

Managed Log Analysis (LA) leads as the largest service category, contributing approximately 21.6% of global MSS revenue. The segment is forecast to grow to US$21.1 billion by 2030. Its dominance is underpinned by persistent enterprise demand for log aggregation, SIEM integration, and regulatory auditability, especially in financial services and critical infrastructure. Managed Network Security (N) emerges as the fastest-growing segment, with a CAGR of 9.8%. Growth is accelerating due to increased adoption of Zero Trust frameworks, hybrid cloud security demands, and next-gen firewall services. This segment is also benefiting from the convergence of Managed Firewall, IDS/IPS, and network segmentation under unified policies.

Managed Security Services (MSS) Market Analysis by Network Security Type

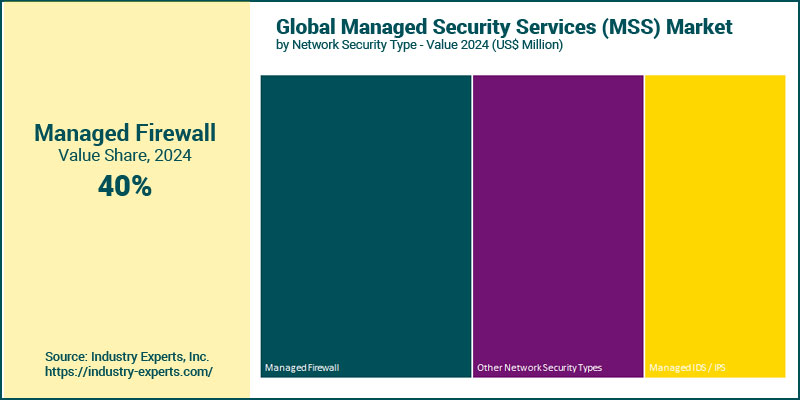

Managed Firewall services continue to dominate the network security landscape, which represents 40.4% of total MSS revenue that year. This segment is expected to reach US$38.3 billion by 2030. The enduring strength of firewall services is driven by regulatory mandates, demand for Zero Trust Network Access (ZTNA), and increasing adoption of next-gen firewall (NGFW) platforms integrated with intrusion prevention and deep packet inspection. Other Network Security Services [which include services like Secure Web Gateway (SWG), DNS security, micro-segmentation, and network traffic analysis] are the fastest-growing segment, advancing at a 2024-2030 CAGR of 6.8%. This growth reflects rising enterprise demand for layered defenses, SASE-aligned architectures, and protection against encrypted malware and lateral movement attacks.

Managed Security Services (MSS) Market Analysis by Deployment Type

Cloud-based MSS represents the dominant and fastest-growing deployment model making up 58.9% of the total market in 2024. This segment is expected to reach US$58.4 billion by 2030. The surge is fueled by widespread adoption of hybrid and multi-cloud infrastructures, demand for scalable threat monitoring, and the proliferation of cloud-native security platforms such as CSPM, CWPP, and SASE-aligned services. Cloud-based MSS offerings are also being prioritized by SMEs seeking rapid onboarding and fixed-cost models. On-Premise MSS, while still significant, is growing at a comparatively slower CAGR of 5.4%. This model remains favored in highly regulated sectors such as government, defense, and financial services, where data residency, latency, and internal governance constraints inhibit cloud migration. However, demand is shifting toward co-managed on-premise SOCs with integrated threat intelligence and automated response frameworks.

Managed Security Services (MSS) Market Analysis by Company Type

Large Enterprises continue to dominate MSS spending, contributing approximately 68.1% of the global market. Further growth among large enterprises is driven by adoption of co-managed SOC models, SASE and XDR convergence, and complex compliance obligations. These organizations typically demand deep visibility, custom SLAs, and integration across multi-vendor ecosystems, especially in finance, healthcare, and critical infrastructure sectors. Small and Medium-Sized Enterprises (SMEs) are the fastest-growing customer segment, expanding at a CAGR of 7.7% from 2024 to 2030. This growth is fueled by rising ransomware threats, cyber insurance requirements, and the lack of internal cybersecurity expertise. SMEs are turning to turnkey MSS bundles with preconfigured Managed SIEM, Firewall, and Vulnerability Management capabilities.

Managed Security Services (MSS) Market Analysis by Industry Sector

BFSI (Banking, Financial Services & Insurance) remains the largest industry segment for MSS accounting for 22.4% of total global revenue in 2024. The sector's dominance stems from its high exposure to cyber threats, reliance on legacy systems, and the regulatory complexity posed by PCI DSS, GDPR, and financial supervisory bodies. Demand is strongest for co-managed SOCs, compliance reporting, and managed threat detection. However, Healthcare is the fastest-growing sector, expected to expand at a CAGR of 9% during 2024-2030. Escalating ransomware attacks, the criticality of patient data protection, and growing HIPAA/GDPR enforcement are driving adoption of managed endpoint security, DLP, and 24/7 monitoring services. Hospitals and clinics with limited in-house cyber staff are increasingly outsourcing SOC operations and incident response functions.

Managed Security Services (MSS) Market Report Scope

This global report on Managed Security Services (MSS) market analyzes the global and regional market based on Service Type, Network Security Type, Deployment Type, Company Type and Industry Sector for the period 2021-2030 with forecasts from 2024 to 2030 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Historical Period: | 2021-2024 | |

| Base Year: | 2024 | |

| Forecast Period: | 2024-2030 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 40+ |

Managed Security Services (MSS) Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Managed Security Services (MSS) Market by Service Type

- Managed LAN

- Managed WI-FI

- Managed VPN

- Managed WAN

- Network Monitoring

- Managed NFV

- Managed Network Security

Managed Security Services (MSS) Market by Network Security Type

- Managed Firewall

- Managed IDS / IPS

- Other Network Security Types

Managed Security Services (MSS) Market by Deployment Type

- Cloud

- On-Premises

Managed Security Services (MSS) Market by Company Type

- Large Enterprises

- SMEs

Managed Security Services (MSS) Market by Industry Sector

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Retail

- Healthcare

- Manufacturing

- Public Sector

- Energy & Utilities

- Other End-Uses

Managed Security Services (MSS) Market Frequently Asked Questions (FAQs)

As of 2024, the global MSS market is valued at approximately US$33.01 billion, driven by increasing cyber threats, compliance mandates, and widespread cloud adoption across enterprises of all sizes.

The global MSS market is projected to reach over US$62 billion by 2030, growing at a compound annual growth rate (CAGR) of 11.1% during the forecast period from 2024 to 2030.

North America remains the largest MSS market, supported by mature cybersecurity maturity across sectors like finance and healthcare. However, Asia-Pacific is the fastest-growing region, with an 8.6% CAGR, fueled by rising cyberattacks, public cloud adoption, and evolving data protection laws in countries like China and India.

Top trends include the rise of Managed Detection and Response (MDR), adoption of cloud-native security services, convergence of SASE, Zero Trust, and XDR frameworks, and demand for co-managed SOCs and regulatory-driven compliance services.

Cloud-based MSS dominates with nearly 59% market share in 2024, and is growing faster than on-premise deployments due to scalability, flexibility, and alignment with hybrid/multi-cloud strategies.

Major players include IBM, Atos, BT, Verizon, SecureWorks, and AT&T, alongside fast-growing vendors like Arctic Wolf, eSentire, Rapid7, CrowdStrike, and Palo Alto Networks, who are redefining MSS with AI and cloud-native approaches.

BFSI is the largest industry segment due to regulatory complexity and high threat exposure, while healthcare is the fastest-growing sector, with MSS adoption driven by ransomware risks, HIPAA/GDPR compliance, and increased digitalization of patient data.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Managed Security Services (MSS)

- Market Segmentation for Managed Security Services (MSS)

- Service Types

- Network Security Types

- Deployment Types

- Company Types

- Industry Sectors

- Key Trends in Managed Security Services (MSS) Market

2. INDUSTRY LANDSCAPE

- Global Managed Security Services (MSS) Market Outlook

- Comprehensive Managed Security Services (MSS) Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Managed Security Services (MSS) Industry

- Startup Strategies for Managed Security Services (MSS) Industry

- SWOT Analysis of Managed Security Services (MSS) Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Managed Security Services (MSS) Companies

- Market Share Analysis of Managed Security Services (MSS) Companies

- SWOT Analysis of Key Players in the Managed Security Services (MSS) Industry

- Key Market Players

- Accenture

- Ascend Technologies

- AT&T

- Atos

- Avertium

- BAE Systems, Inc.

- Broadcom

- Capgemini

- Check Point Software Technologies Ltd.

- Cipher Security

- Cisco

- CrowdStrike

- Cyflare

- DigitalXRAID

- DXC Technology

- F5

- Fortinet Inc.

- Fujitsu

- HelpSystems

- Hewlett Packard Enterprise Development LP

- IBM

- Infosys

- Kroll

- Kudelski Security

- LightEdge

- Lumen Technologies

- Nettitude

- Nokia Networks

- NTT

- Orange Cyberdefense

- Palo Alto Networks

- Proficio

- Rapid

- RSI Security

- SecureWorks

- SecurityHQ

- TCS

- Teceze

- Trend Micro

- TrustNet

- Trustwave

- Verizon

- VirtualArmour

- Wipro

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Managed Security Services (MSS) Market Overview by Service Type

- Managed Security Services (MSS) Service Type Market Overview by Global Region

- Managed LAN

- Managed WI-FI

- Managed VPN

- Managed WAN

- Network Monitoring

- Managed NFV

- Managed Network Security

- Global Managed Security Services (MSS) Market Overview by Network Security Type

- Managed Security Services (MSS) Network Security Type Market Overview by Global Region

- Managed Firewall

- Managed IDS / IPS

- Other Network Security Types

- Global Managed Security Services (MSS) Market Overview by Deployment Type

- Managed Security Services (MSS) Deployment Type Market Overview by Global Region

- Cloud

- On-Premises

- Global Managed Security Services (MSS) Market Overview by Company Type

- Managed Security Services (MSS) Company Type Market Overview by Global Region

- Large Enterprises

- SMEs

- Global Managed Security Services (MSS) Market Overview by Industry Sector

- Managed Security Services (MSS) Industry Sector Market Overview by Global Region

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Media & Entertainment

- Other Industry Sectors

PART B: REGIONAL MARKET PERSPECTIVE

- Global Managed Security Services (MSS) Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Managed Security Services (MSS) Market Overview by Geographic Region

- North American Managed Security Services (MSS) Market Overview by Service Type

- North American Managed Security Services (MSS) Market Overview by Network Security Type

- North American Managed Security Services (MSS) Market Overview by Deployment Type

- North American Managed Security Services (MSS) Market Overview by Company Type

- North American Managed Security Services (MSS) Market Overview by Industry Sector

- Country-wise Analysis of North American Managed Security Services (MSS) Market

- THE UNITED STATES

- United States Managed Security Services (MSS) Market Overview by Service Type

- United States Managed Security Services (MSS) Market Overview by Network Security Type

- United States Managed Security Services (MSS) Market Overview by Deployment Type

- United States Managed Security Services (MSS) Market Overview by Company Type

- United States Managed Security Services (MSS) Market Overview by Industry Sector

- CANADA

- Canadian Managed Security Services (MSS) Market Overview by Service Type

- Canadian Managed Security Services (MSS) Market Overview by Network Security Type

- Canadian Managed Security Services (MSS) Market Overview by Deployment Type

- Canadian Managed Security Services (MSS) Market Overview by Company Type

- Canadian Managed Security Services (MSS) Market Overview by Industry Sector

- MEXICO

- Mexican Managed Security Services (MSS) Market Overview by Service Type

- Mexican Managed Security Services (MSS) Market Overview by Network Security Type

- Mexican Managed Security Services (MSS) Market Overview by Deployment Type

- Mexican Managed Security Services (MSS) Market Overview by Company Type

- Mexican Managed Security Services (MSS) Market Overview by Industry Sector

7. EUROPE

- European Managed Security Services (MSS) Market Overview by Geographic Region

- European Managed Security Services (MSS) Market Overview by Service Type

- European Managed Security Services (MSS) Market Overview by Network Security Type

- European Managed Security Services (MSS) Market Overview by Deployment Type

- European Managed Security Services (MSS) Market Overview by Company Type

- European Managed Security Services (MSS) Market Overview by Industry Sector

- Country-wise Analysis of European Managed Security Services (MSS) Market

- GERMANY

- German Managed Security Services (MSS) Market Overview by Service Type

- German Managed Security Services (MSS) Market Overview by Network Security Type

- German Managed Security Services (MSS) Market Overview by Deployment Type

- German Managed Security Services (MSS) Market Overview by Company Type

- German Managed Security Services (MSS) Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Managed Security Services (MSS) Market Overview by Service Type

- United Kingdom Managed Security Services (MSS) Market Overview by Network Security Type

- United Kingdom Managed Security Services (MSS) Market Overview by Deployment Type

- United Kingdom Managed Security Services (MSS) Market Overview by Company Type

- United Kingdom Managed Security Services (MSS) Market Overview by Industry Sector

- FRANCE

- French Managed Security Services (MSS) Market Overview by Service Type

- French Managed Security Services (MSS) Market Overview by Network Security Type

- French Managed Security Services (MSS) Market Overview by Deployment Type

- French Managed Security Services (MSS) Market Overview by Company Type

- French Managed Security Services (MSS) Market Overview by Industry Sector

- ITALY

- Italian Managed Security Services (MSS) Market Overview by Service Type

- Italian Managed Security Services (MSS) Market Overview by Network Security Type

- Italian Managed Security Services (MSS) Market Overview by Deployment Type

- Italian Managed Security Services (MSS) Market Overview by Company Type

- Italian Managed Security Services (MSS) Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Managed Security Services (MSS) Market Overview by Service Type

- Dutch Managed Security Services (MSS) Market Overview by Network Security Type

- Dutch Managed Security Services (MSS) Market Overview by Deployment Type

- Dutch Managed Security Services (MSS) Market Overview by Company Type

- Dutch Managed Security Services (MSS) Market Overview by Industry Sector

- SPAIN

- Spanish Managed Security Services (MSS) Market Overview by Service Type

- Spanish Managed Security Services (MSS) Market Overview by Network Security Type

- Spanish Managed Security Services (MSS) Market Overview by Deployment Type

- Spanish Managed Security Services (MSS) Market Overview by Company Type

- Spanish Managed Security Services (MSS) Market Overview by Industry Sector

- RUSSIA

- Russian Managed Security Services (MSS) Market Overview by Service Type

- Russian Managed Security Services (MSS) Market Overview by Network Security Type

- Russian Managed Security Services (MSS) Market Overview by Deployment Type

- Russian Managed Security Services (MSS) Market Overview by Company Type

- Russian Managed Security Services (MSS) Market Overview by Industry Sector

- SWITZERLAND

- Swiss Managed Security Services (MSS) Market Overview by Service Type

- Swiss Managed Security Services (MSS) Market Overview by Network Security Type

- Swiss Managed Security Services (MSS) Market Overview by Deployment Type

- Swiss Managed Security Services (MSS) Market Overview by Company Type

- Swiss Managed Security Services (MSS) Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Managed Security Services (MSS) Market Overview by Service Type

- Rest of Europe Managed Security Services (MSS) Market Overview by Network Security Type

- Rest of Europe Managed Security Services (MSS) Market Overview by Deployment Type

- Rest of Europe Managed Security Services (MSS) Market Overview by Company Type

- Rest of Europe Managed Security Services (MSS) Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Managed Security Services (MSS) Market Overview by Geographic Region

- Asia-Pacific Managed Security Services (MSS) Market Overview by Service Type

- Asia-Pacific Managed Security Services (MSS) Market Overview by Network Security Type

- Asia-Pacific Managed Security Services (MSS) Market Overview by Deployment Type

- Asia-Pacific Managed Security Services (MSS) Market Overview by Company Type

- Asia-Pacific Managed Security Services (MSS) Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Managed Security Services (MSS) Market

- CHINA

- Chinese Managed Security Services (MSS) Market Overview by Service Type

- Chinese Managed Security Services (MSS) Market Overview by Network Security Type

- Chinese Managed Security Services (MSS) Market Overview by Deployment Type

- Chinese Managed Security Services (MSS) Market Overview by Company Type

- Chinese Managed Security Services (MSS) Market Overview by Industry Sector

- JAPAN

- Japanese Managed Security Services (MSS) Market Overview by Service Type

- Japanese Managed Security Services (MSS) Market Overview by Network Security Type

- Japanese Managed Security Services (MSS) Market Overview by Deployment Type

- Japanese Managed Security Services (MSS) Market Overview by Company Type

- Japanese Managed Security Services (MSS) Market Overview by Industry Sector

- INDIA

- Indian Managed Security Services (MSS) Market Overview by Service Type

- Indian Managed Security Services (MSS) Market Overview by Network Security Type

- Indian Managed Security Services (MSS) Market Overview by Deployment Type

- Indian Managed Security Services (MSS) Market Overview by Company Type

- Indian Managed Security Services (MSS) Market Overview by Industry Sector

- AUSTRALIA

- Australia Managed Security Services (MSS) Market Overview by Service Type

- Australia Managed Security Services (MSS) Market Overview by Network Security Type

- Australia Managed Security Services (MSS) Market Overview by Deployment Type

- Australia Managed Security Services (MSS) Market Overview by Company Type

- Australia Managed Security Services (MSS) Market Overview by Industry Sector

- SINGAPORE

- Singaporean Managed Security Services (MSS) Market Overview by Service Type

- Singaporean Managed Security Services (MSS) Market Overview by Network Security Type

- Singaporean Managed Security Services (MSS) Market Overview by Deployment Type

- Singaporean Managed Security Services (MSS) Market Overview by Company Type

- Singaporean Managed Security Services (MSS) Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Managed Security Services (MSS) Market Overview by Service Type

- South Korean Managed Security Services (MSS) Market Overview by Network Security Type

- South Korean Managed Security Services (MSS) Market Overview by Deployment Type

- South Korean Managed Security Services (MSS) Market Overview by Company Type

- South Korean Managed Security Services (MSS) Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Managed Security Services (MSS) Market Overview by Service Type

- Rest of Asia-Pacific Managed Security Services (MSS) Market Overview by Network Security Type

- Rest of Asia-Pacific Managed Security Services (MSS) Market Overview by Deployment Type

- Rest of Asia-Pacific Managed Security Services (MSS) Market Overview by Company Type

- Rest of Asia-Pacific Managed Security Services (MSS) Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Managed Security Services (MSS) Market Overview by Geographic Region

- South American Managed Security Services (MSS) Market Overview by Service Type

- South American Managed Security Services (MSS) Market Overview by Network Security Type

- South American Managed Security Services (MSS) Market Overview by Deployment Type

- South American Managed Security Services (MSS) Market Overview by Company Type

- South American Managed Security Services (MSS) Market Overview by Industry Sector

- Country-wise Analysis of South American Managed Security Services (MSS) Market

- BRAZIL

- Brazilian Managed Security Services (MSS) Market Overview by Service Type

- Brazilian Managed Security Services (MSS) Market Overview by Network Security Type

- Brazilian Managed Security Services (MSS) Market Overview by Deployment Type

- Brazilian Managed Security Services (MSS) Market Overview by Company Type

- Brazilian Managed Security Services (MSS) Market Overview by Industry Sector

- ARGENTINA

- Argentine Managed Security Services (MSS) Market Overview by Service Type

- Argentine Managed Security Services (MSS) Market Overview by Network Security Type

- Argentine Managed Security Services (MSS) Market Overview by Deployment Type

- Argentine Managed Security Services (MSS) Market Overview by Company Type

- Argentine Managed Security Services (MSS) Market Overview by Industry Sector

- COLOMBIA

- Colombian Managed Security Services (MSS) Market Overview by Service Type

- Colombian Managed Security Services (MSS) Market Overview by Network Security Type

- Colombian Managed Security Services (MSS) Market Overview by Deployment Type

- Colombian Managed Security Services (MSS) Market Overview by Company Type

- Colombian Managed Security Services (MSS) Market Overview by Industry Sector

- CHILE

- Chilean Managed Security Services (MSS) Market Overview by Service Type

- Chilean Managed Security Services (MSS) Market Overview by Network Security Type

- Chilean Managed Security Services (MSS) Market Overview by Deployment Type

- Chilean Managed Security Services (MSS) Market Overview by Company Type

- Chilean Managed Security Services (MSS) Market Overview by Industry Sector

- PERU

- Peruvian Managed Security Services (MSS) Market Overview by Service Type

- Peruvian Managed Security Services (MSS) Market Overview by Network Security Type

- Peruvian Managed Security Services (MSS) Market Overview by Deployment Type

- Peruvian Managed Security Services (MSS) Market Overview by Company Type

- Peruvian Managed Security Services (MSS) Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Managed Security Services (MSS) Market Overview by Service Type

- Rest of South America Managed Security Services (MSS) Market Overview by Network Security Type

- Rest of South America Managed Security Services (MSS) Market Overview by Deployment Type

- Rest of South America Managed Security Services (MSS) Market Overview by Company Type

- Rest of South America Managed Security Services (MSS) Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Managed Security Services (MSS) Market Overview by Geographic Region

- Middle East & Africa Managed Security Services (MSS) Market Overview by Service Type

- Middle East & Africa Managed Security Services (MSS) Market Overview by Network Security Type

- Middle East & Africa Managed Security Services (MSS) Market Overview by Deployment Type

- Middle East & Africa Managed Security Services (MSS) Market Overview by Company Type

- Middle East & Africa Managed Security Services (MSS) Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Managed Security Services (MSS) Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Managed Security Services (MSS) Market Overview by Service Type

- United Arab Emirates Managed Security Services (MSS) Market Overview by Network Security Type

- United Arab Emirates Managed Security Services (MSS) Market Overview by Deployment Type

- United Arab Emirates Managed Security Services (MSS) Market Overview by Company Type

- United Arab Emirates Managed Security Services (MSS) Market Overview by Industry Sector

- SOUTH AFRICA

- South African Managed Security Services (MSS) Market Overview by Service Type

- South African Managed Security Services (MSS) Market Overview by Network Security Type

- South African Managed Security Services (MSS) Market Overview by Deployment Type

- South African Managed Security Services (MSS) Market Overview by Company Type

- South African Managed Security Services (MSS) Market Overview by Industry Sector

- EGYPT

- Egyptian Managed Security Services (MSS) Market Overview by Service Type

- Egyptian Managed Security Services (MSS) Market Overview by Network Security Type

- Egyptian Managed Security Services (MSS) Market Overview by Deployment Type

- Egyptian Managed Security Services (MSS) Market Overview by Company Type

- Egyptian Managed Security Services (MSS) Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Managed Security Services (MSS) Market Overview by Service Type

- Saudi Arabian Managed Security Services (MSS) Market Overview by Network Security Type

- Saudi Arabian Managed Security Services (MSS) Market Overview by Deployment Type

- Saudi Arabian Managed Security Services (MSS) Market Overview by Company Type

- Saudi Arabian Managed Security Services (MSS) Market Overview by Industry Sector

- MOROCCO

- Moroccan Managed Security Services (MSS) Market Overview by Service Type

- Moroccan Managed Security Services (MSS) Market Overview by Network Security Type

- Moroccan Managed Security Services (MSS) Market Overview by Deployment Type

- Moroccan Managed Security Services (MSS) Market Overview by Company Type

- Moroccan Managed Security Services (MSS) Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Managed Security Services (MSS) Market Overview by Service Type

- Kuwaiti Managed Security Services (MSS) Market Overview by Network Security Type

- Kuwaiti Managed Security Services (MSS) Market Overview by Deployment Type

- Kuwaiti Managed Security Services (MSS) Market Overview by Company Type

- Kuwaiti Managed Security Services (MSS) Market Overview by Industry Sector

- QATAR

- Qatari Managed Security Services (MSS) Market Overview by Service Type

- Qatari Managed Security Services (MSS) Market Overview by Network Security Type

- Qatari Managed Security Services (MSS) Market Overview by Deployment Type

- Qatari Managed Security Services (MSS) Market Overview by Company Type

- Qatari Managed Security Services (MSS) Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Managed Security Services (MSS) Market Overview by Service Type

- Rest of Middle East & Africa Managed Security Services (MSS) Market Overview by Network Security Type

- Rest of Middle East & Africa Managed Security Services (MSS) Market Overview by Deployment Type

- Rest of Middle East & Africa Managed Security Services (MSS) Market Overview by Company Type

- Rest of Middle East & Africa Managed Security Services (MSS) Market Overview by Industry Sector

PART C: INDUSTRY GUIDE

PART D: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

Accenture

Ascend Technologies

AT&T

Atos

Avertium

BAE Systems, Inc.

Broadcom

Capgemini

Check Point Software Technologies Ltd.

Cipher Security

Cisco

CrowdStrike

Cyflare

DigitalXRAID

DXC Technology

F5

Fortinet Inc.

Fujitsu

HelpSystems

Hewlett Packard Enterprise Development LP

IBM

Infosys

Kroll

Kudelski Security

LightEdge

Lumen Technologies

Nettitude

Nokia Networks

NTT

Orange Cyberdefense

Palo Alto Networks

Proficio

Rapid

RSI Security

SecureWorks

SecurityHQ

TCS

Teceze

Trend Micro

TrustNet

Trustwave

Verizon

VirtualArmour

Wipro

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |