Managed Mobility Services (MMS) - A Global Market Overview

- Published: Aug 2025

- Pages: 491 | Charts: 405

- Report Code: ITM121

SHARE THIS REPORT:

Global Managed Mobility Services (MMS) Market Trends and Outlook

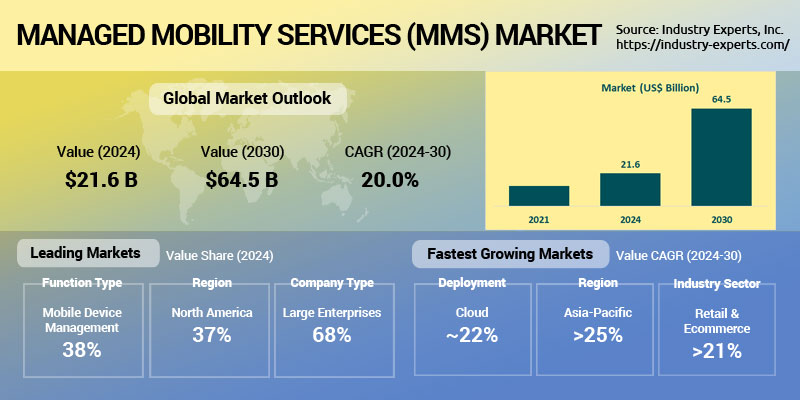

The global Managed Mobility Services (MMS) market is on a strong growth trajectory, projected to expand from US$21.6 billion in 2024 to over US$64.5 billion by 2030, registering a compound annual growth rate (CAGR) of 20% during the forecast period. This surge is fueled by the rapid proliferation of mobile endpoints across enterprises, the widespread adoption of hybrid and remote work models, and the growing need for secure, centralized, and scalable management of mobile devices, applications, and data. As organizations shift toward mobile-first and cloud-first strategies, MMS solutions are becoming essential for ensuring visibility, compliance, and cost efficiency in increasingly complex IT environments.

Key market drivers include the growing complexity of managing multivendor mobile ecosystems, the rise of BYOD (Bring Your Own Device) policies, and the need to enforce security and governance at scale. Enterprises are also seeking to reduce the burden on internal IT teams by outsourcing mobile lifecycle management, fueling demand for MMS platforms that offer end-to-end capabilities, from device provisioning to security, expense control, and support. The integration of AI, automation, and zero-trust frameworks into MMS solutions is further transforming the landscape, enabling more proactive management and dynamic policy enforcement. As mobile usage continues to reshape how businesses operate, the MMS market is set to play a pivotal role in enterprise digital transformation strategies through 2030.

Leading MMS vendors include IBM, Vodafone Business, AT&T, Capgemini, Infosys, HCLTech, Orange Business Services, DXC Technology, Wipro, Kyndryl, Verizon Business, Cognizant, and GEMA, among others.

Managed Mobility Services (MMS) Regional Market Analysis

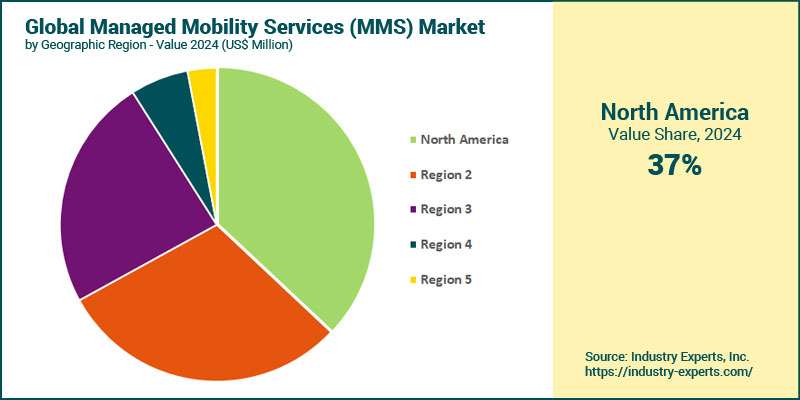

In 2024, North America led the global Managed Mobility Services (MMS) market with an estimated share of approximately 37% of global revenue. The region's dominance is attributed to early enterprise mobility adoption, a high concentration of large multinational corporations, and strong demand for BYOD, mobile security, and unified endpoint management solutions. Looking ahead, Asia-Pacific is set to record the fastest growth, registering a CAGR of 25.6% between 2024 and 2030. This rapid expansion is driven by escalating enterprise mobility adoption, large mobile workforce populations in China and India, and government-led digitalization initiatives. South America is the second fastest-growing region, fueled by increasing smartphone penetration, growing SME sector demand, and telecom modernization across Brazil, Argentina, and Chile.

Managed Mobility Services (MMS) Market Analysis by Function Type

In terms of function type, Mobile Device Management (MDM) emerged as the largest segment in 2024, generating an estimated 38% of global MMS revenue. The MDM segment continues to dominate due to its foundational role in enterprise mobility frameworks, supporting centralized control, policy enforcement, and lifecycle management of diverse mobile endpoints. The segment benefits from increasing demand for secure remote access, especially in hybrid work environments, and the proliferation of enterprise-issued and BYOD devices. Mobile Application Management (MAM) is set to be the fastest-growing function segment, expanding at a CAGR of 23.1% between 2024 and 2030. This surge is fueled by the explosion of enterprise mobile apps, the rise of mobile-first strategies, and the need for fine-grained app-level security and control across corporate and personal devices. Organizations are prioritizing app containerization, app wrapping, and dynamic policy updates to manage data without compromising user privacy.

Managed Mobility Services (MMS) Market Analysis by Deployment Type

In 2024, the Cloud-based deployment model dominated the global Managed Mobility Services (MMS) market, cornering a 56% share of total revenues. The strong momentum for cloud deployment is driven by the growing need for scalability, cost-effectiveness, remote accessibility, and faster onboarding across distributed enterprises. The cloud model is particularly appealing to SMEs and multinational organizations adopting hybrid work models and requiring centralized mobility management without extensive on-premise infrastructure. Looking ahead, the Cloud segment is expected to grow at a robust CAGR of 22.1% between 2024 and 2030, reaching US$40.2 billion by the end of the forecast period. The accelerating transition to cloud-first mobility strategies, boosted by advances in AI, automation, and zero-trust security, is reshaping vendor offerings and enterprise buying behavior globally.

Managed Mobility Services (MMS) Market Analysis by Company Type

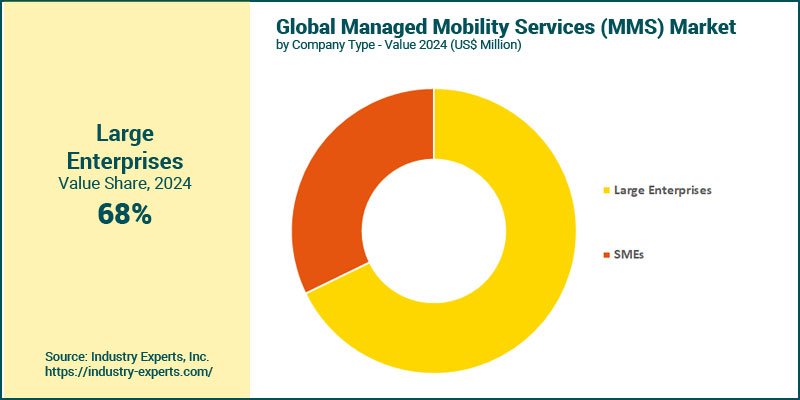

As of 2024, Large Enterprises formed the dominant customer segment in the global Managed Mobility Services (MMS) market, accounting for nearly 68% of global revenues. This stronghold is due to their complex mobility needs, vast device ecosystems, and heightened emphasis on mobile security, compliance, and global endpoint management. Large organizations also typically engage in multi-vendor MMS outsourcing strategies, favoring comprehensive, scalable solutions across regions and subsidiaries. In contrast, Small and Medium Enterprises (SMEs) are poised to be the fastest-growing customer segment, expanding at a 22.8% CAGR between 2024 and 2030, and expected to reach US$23.9 billion by 2030. The accelerating growth among SMEs is fueled by their adoption of cloud-native mobility platforms, demand for affordable bundled services, and increasing reliance on mobile devices for core business functions. The rising availability of subscription-based MMS offerings tailored for SME scalability and cost sensitivity is further catalyzing uptake.

Managed Mobility Services (MMS) Market Analysis by Industry Sector

IT & Telecom led all industry sectors in MMS adoption in 2024, contributing an estimated 22.5% of total global revenues. This dominance stems from high device volumes, geographically distributed workforces, and the sector's early embrace of digital workplace strategies and advanced mobile security. Healthcare followed closely, driven by the rising integration of mobile health (mHealth) tools, remote patient care, and regulatory compliance needs. The Healthcare sector is projected to be the fastest-growing industry segment, expanding at a CAGR of 23% from 2024 to 2030. This rapid growth is fueled by increased telehealth adoption, patient data mobility, and the urgent need for HIPAA-compliant mobile solutions across hospitals, clinics, and insurers. Retail & Ecommerce is another high-growth segment, supported by rising demand for mobile point-of-sale (mPOS) systems, field sales mobility, and consumer-facing mobile apps.

Managed Mobility Services (MMS) Market Report Scope

This global report on Managed Mobility Services (MMS) market analyzes the global and regional market based on Function Type, Deployment Type, Company Type and Industry Sector for the period 2021-2030 with forecasts from 2024 to 2030 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Historical Period: | 2021-2024 | |

| Base Year: | 2024 | |

| Forecast Period: | 2024-2030 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 30+ |

Managed Mobility Services (MMS) Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Managed Mobility Services (MMS) Market by Function Type

- Mobile Device Management

- Mobile Application Management

- Mobile Security

- Other Function Types

Managed Mobility Services (MMS) Market by Deployment Type

- Cloud

- On-Premises

Managed Mobility Services (MMS) Market by Company Type

- Large Enterprises

- SMEs

Managed Mobility Services (MMS) Market by Industry Sector

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

Managed Mobility Services (MMS) Market Frequently Asked Questions (FAQs)

The global MMS market is valued at US$21.6 billion in 2024 and projected to reach US$64.5 billion by 2030, growing at a CAGR of 20%.

North America leads the market with a 37% share, driven by high enterprise mobility maturity, cloud adoption, and large-scale endpoint management demand.

Asia-Pacific is the fastest-growing region, forecast to expand at 25.6% CAGR, reaching over US$20.3 billion by 2030.

Mobile Device Management (MDM) is the largest in 2024 (US$8.2B), while Mobile Application Management (MAM) is the fastest-growing, registering 23.1% CAGR.

Cloud deployment leads with 56% share in 2024 and is projected to exceed US$40.2 billion by 2030, driven by SaaS models and hybrid workforces.

Large enterprises dominate the market, but SMEs are growing rapidly due to the availability of flexible, affordable MMS offerings.

IT & Telecom leads in 2024, while Healthcare is the fastest-growing industry sector (23% CAGR), followed by Retail, Education, and Manufacturing.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Managed Mobility Services (MMS)

- Market Segmentation for Managed Mobility Services (MMS)

- Function Types

- Deployment Types

- Company Types

- Industry Sectors

- Key Trends in Managed Mobility Services (MMS) Market

2. INDUSTRY LANDSCAPE

- Global Managed Mobility Services (MMS) Market Outlook

- Comprehensive Managed Mobility Services (MMS) Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Managed Mobility Services (MMS) Industry

- Startup Strategies for Managed Mobility Services (MMS) Industry

- SWOT Analysis of Managed Mobility Services (MMS) Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Managed Mobility Services (MMS) Companies

- Market Share Analysis of Managed Mobility Services (MMS) Companies

- SWOT Analysis of Key Players in the Managed Mobility Services (MMS) Industry

- Key Market Players

- Accenture

- AT&T Business

- Atos

- Barrachd (Capita)

- BT Global Services

- Cancom

- Capgemini

- CDW

- Cognizant

- Computacenter

- Deutsche Telekom (T-Systems)

- DMI (Digital Management LLC)

- DXC Technology

- Fujitsu

- GEMA (Global Enterprise Mobility Alliance)

- HCLTech

- IBM

- Infosys

- Insight Enterprises

- Kyndryl

- Mobliciti

- NTT Ltd.

- Orange Business Services

- Presidio

- SCC (Specialist Computer Centres)

- Singtel Enterprise

- Synnex / TD SYNNEX

- Tata Consultancy Services (TCS)

- Tech Data

- Telefonica Tech

- Verizon Business

- Vodafone Business

- Wipro

- Zones

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Managed Mobility Services (MMS) Market Overview by Function Type

- Managed Mobility Services (MMS) Function Type Market Overview by Global Region

- Mobile Device Management

- Mobile Application Management

- Mobile Security

- Other Function Types

- Global Managed Mobility Services (MMS) Market Overview by Deployment Type

- Managed Mobility Services (MMS) Deployment Type Market Overview by Global Region

- Cloud

- On-Premises

- Global Managed Mobility Services (MMS) Market Overview by Company Type

- Managed Mobility Services (MMS) Company Type Market Overview by Global Region

- Large Enterprises

- SMEs

- Global Managed Mobility Services (MMS) Market Overview by Industry Sector

- Managed Mobility Services (MMS) Industry Sector Market Overview by Global Region

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

PART B: REGIONAL MARKET PERSPECTIVE

- Global Managed Mobility Services (MMS) Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Managed Mobility Services (MMS) Market Overview by Geographic Region

- North American Managed Mobility Services (MMS) Market Overview by Function Type

- North American Managed Mobility Services (MMS) Market Overview by Deployment Type

- North American Managed Mobility Services (MMS) Market Overview by Company Type

- North American Managed Mobility Services (MMS) Market Overview by Industry Sector

- Country-wise Analysis of North American Managed Mobility Services (MMS) Market

- THE UNITED STATES

- United States Managed Mobility Services (MMS) Market Overview by Function Type

- United States Managed Mobility Services (MMS) Market Overview by Deployment Type

- United States Managed Mobility Services (MMS) Market Overview by Company Type

- United States Managed Mobility Services (MMS) Market Overview by Industry Sector

- CANADA

- Canadian Managed Mobility Services (MMS) Market Overview by Function Type

- Canadian Managed Mobility Services (MMS) Market Overview by Deployment Type

- Canadian Managed Mobility Services (MMS) Market Overview by Company Type

- Canadian Managed Mobility Services (MMS) Market Overview by Industry Sector

- MEXICO

- Mexican Managed Mobility Services (MMS) Market Overview by Function Type

- Mexican Managed Mobility Services (MMS) Market Overview by Deployment Type

- Mexican Managed Mobility Services (MMS) Market Overview by Company Type

- Mexican Managed Mobility Services (MMS) Market Overview by Industry Sector

7. EUROPE

- European Managed Mobility Services (MMS) Market Overview by Geographic Region

- European Managed Mobility Services (MMS) Market Overview by Function Type

- European Managed Mobility Services (MMS) Market Overview by Deployment Type

- European Managed Mobility Services (MMS) Market Overview by Company Type

- European Managed Mobility Services (MMS) Market Overview by Industry Sector

- Country-wise Analysis of European Managed Mobility Services (MMS) Market

- GERMANY

- German Managed Mobility Services (MMS) Market Overview by Function Type

- German Managed Mobility Services (MMS) Market Overview by Deployment Type

- German Managed Mobility Services (MMS) Market Overview by Company Type

- German Managed Mobility Services (MMS) Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Managed Mobility Services (MMS) Market Overview by Function Type

- United Kingdom Managed Mobility Services (MMS) Market Overview by Deployment Type

- United Kingdom Managed Mobility Services (MMS) Market Overview by Company Type

- United Kingdom Managed Mobility Services (MMS) Market Overview by Industry Sector

- FRANCE

- French Managed Mobility Services (MMS) Market Overview by Function Type

- French Managed Mobility Services (MMS) Market Overview by Deployment Type

- French Managed Mobility Services (MMS) Market Overview by Company Type

- French Managed Mobility Services (MMS) Market Overview by Industry Sector

- ITALY

- Italian Managed Mobility Services (MMS) Market Overview by Function Type

- Italian Managed Mobility Services (MMS) Market Overview by Deployment Type

- Italian Managed Mobility Services (MMS) Market Overview by Company Type

- Italian Managed Mobility Services (MMS) Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Managed Mobility Services (MMS) Market Overview by Function Type

- Dutch Managed Mobility Services (MMS) Market Overview by Deployment Type

- Dutch Managed Mobility Services (MMS) Market Overview by Company Type

- Dutch Managed Mobility Services (MMS) Market Overview by Industry Sector

- SPAIN

- Spanish Managed Mobility Services (MMS) Market Overview by Function Type

- Spanish Managed Mobility Services (MMS) Market Overview by Deployment Type

- Spanish Managed Mobility Services (MMS) Market Overview by Company Type

- Spanish Managed Mobility Services (MMS) Market Overview by Industry Sector

- RUSSIA

- Russian Managed Mobility Services (MMS) Market Overview by Function Type

- Russian Managed Mobility Services (MMS) Market Overview by Deployment Type

- Russian Managed Mobility Services (MMS) Market Overview by Company Type

- Russian Managed Mobility Services (MMS) Market Overview by Industry Sector

- SWITZERLAND

- Swiss Managed Mobility Services (MMS) Market Overview by Function Type

- Swiss Managed Mobility Services (MMS) Market Overview by Deployment Type

- Swiss Managed Mobility Services (MMS) Market Overview by Company Type

- Swiss Managed Mobility Services (MMS) Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Managed Mobility Services (MMS) Market Overview by Function Type

- Rest of Europe Managed Mobility Services (MMS) Market Overview by Deployment Type

- Rest of Europe Managed Mobility Services (MMS) Market Overview by Company Type

- Rest of Europe Managed Mobility Services (MMS) Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Managed Mobility Services (MMS) Market Overview by Geographic Region

- Asia-Pacific Managed Mobility Services (MMS) Market Overview by Function Type

- Asia-Pacific Managed Mobility Services (MMS) Market Overview by Deployment Type

- Asia-Pacific Managed Mobility Services (MMS) Market Overview by Company Type

- Asia-Pacific Managed Mobility Services (MMS) Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Managed Mobility Services (MMS) Market

- CHINA

- Chinese Managed Mobility Services (MMS) Market Overview by Function Type

- Chinese Managed Mobility Services (MMS) Market Overview by Deployment Type

- Chinese Managed Mobility Services (MMS) Market Overview by Company Type

- Chinese Managed Mobility Services (MMS) Market Overview by Industry Sector

- JAPAN

- Japanese Managed Mobility Services (MMS) Market Overview by Function Type

- Japanese Managed Mobility Services (MMS) Market Overview by Deployment Type

- Japanese Managed Mobility Services (MMS) Market Overview by Company Type

- Japanese Managed Mobility Services (MMS) Market Overview by Industry Sector

- INDIA

- Indian Managed Mobility Services (MMS) Market Overview by Function Type

- Indian Managed Mobility Services (MMS) Market Overview by Deployment Type

- Indian Managed Mobility Services (MMS) Market Overview by Company Type

- Indian Managed Mobility Services (MMS) Market Overview by Industry Sector

- AUSTRALIA

- Australia Managed Mobility Services (MMS) Market Overview by Function Type

- Australia Managed Mobility Services (MMS) Market Overview by Deployment Type

- Australia Managed Mobility Services (MMS) Market Overview by Company Type

- Australia Managed Mobility Services (MMS) Market Overview by Industry Sector

- SINGAPORE

- Singaporean Managed Mobility Services (MMS) Market Overview by Function Type

- Singaporean Managed Mobility Services (MMS) Market Overview by Deployment Type

- Singaporean Managed Mobility Services (MMS) Market Overview by Company Type

- Singaporean Managed Mobility Services (MMS) Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Managed Mobility Services (MMS) Market Overview by Function Type

- South Korean Managed Mobility Services (MMS) Market Overview by Deployment Type

- South Korean Managed Mobility Services (MMS) Market Overview by Company Type

- South Korean Managed Mobility Services (MMS) Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Managed Mobility Services (MMS) Market Overview by Function Type

- Rest of Asia-Pacific Managed Mobility Services (MMS) Market Overview by Deployment Type

- Rest of Asia-Pacific Managed Mobility Services (MMS) Market Overview by Company Type

- Rest of Asia-Pacific Managed Mobility Services (MMS) Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Managed Mobility Services (MMS) Market Overview by Geographic Region

- South American Managed Mobility Services (MMS) Market Overview by Function Type

- South American Managed Mobility Services (MMS) Market Overview by Deployment Type

- South American Managed Mobility Services (MMS) Market Overview by Company Type

- South American Managed Mobility Services (MMS) Market Overview by Industry Sector

- Country-wise Analysis of South American Managed Mobility Services (MMS) Market

- BRAZIL

- Brazilian Managed Mobility Services (MMS) Market Overview by Function Type

- Brazilian Managed Mobility Services (MMS) Market Overview by Deployment Type

- Brazilian Managed Mobility Services (MMS) Market Overview by Company Type

- Brazilian Managed Mobility Services (MMS) Market Overview by Industry Sector

- ARGENTINA

- Argentine Managed Mobility Services (MMS) Market Overview by Function Type

- Argentine Managed Mobility Services (MMS) Market Overview by Deployment Type

- Argentine Managed Mobility Services (MMS) Market Overview by Company Type

- Argentine Managed Mobility Services (MMS) Market Overview by Industry Sector

- COLOMBIA

- Colombian Managed Mobility Services (MMS) Market Overview by Function Type

- Colombian Managed Mobility Services (MMS) Market Overview by Deployment Type

- Colombian Managed Mobility Services (MMS) Market Overview by Company Type

- Colombian Managed Mobility Services (MMS) Market Overview by Industry Sector

- CHILE

- Chilean Managed Mobility Services (MMS) Market Overview by Function Type

- Chilean Managed Mobility Services (MMS) Market Overview by Deployment Type

- Chilean Managed Mobility Services (MMS) Market Overview by Company Type

- Chilean Managed Mobility Services (MMS) Market Overview by Industry Sector

- PERU

- Peruvian Managed Mobility Services (MMS) Market Overview by Function Type

- Peruvian Managed Mobility Services (MMS) Market Overview by Deployment Type

- Peruvian Managed Mobility Services (MMS) Market Overview by Company Type

- Peruvian Managed Mobility Services (MMS) Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Managed Mobility Services (MMS) Market Overview by Function Type

- Rest of South America Managed Mobility Services (MMS) Market Overview by Deployment Type

- Rest of South America Managed Mobility Services (MMS) Market Overview by Company Type

- Rest of South America Managed Mobility Services (MMS) Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Managed Mobility Services (MMS) Market Overview by Geographic Region

- Middle East & Africa Managed Mobility Services (MMS) Market Overview by Function Type

- Middle East & Africa Managed Mobility Services (MMS) Market Overview by Deployment Type

- Middle East & Africa Managed Mobility Services (MMS) Market Overview by Company Type

- Middle East & Africa Managed Mobility Services (MMS) Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Managed Mobility Services (MMS) Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Managed Mobility Services (MMS) Market Overview by Function Type

- United Arab Emirates Managed Mobility Services (MMS) Market Overview by Deployment Type

- United Arab Emirates Managed Mobility Services (MMS) Market Overview by Company Type

- United Arab Emirates Managed Mobility Services (MMS) Market Overview by Industry Sector

- SOUTH AFRICA

- South African Managed Mobility Services (MMS) Market Overview by Function Type

- South African Managed Mobility Services (MMS) Market Overview by Deployment Type

- South African Managed Mobility Services (MMS) Market Overview by Company Type

- South African Managed Mobility Services (MMS) Market Overview by Industry Sector

- EGYPT

- Egyptian Managed Mobility Services (MMS) Market Overview by Function Type

- Egyptian Managed Mobility Services (MMS) Market Overview by Deployment Type

- Egyptian Managed Mobility Services (MMS) Market Overview by Company Type

- Egyptian Managed Mobility Services (MMS) Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Managed Mobility Services (MMS) Market Overview by Function Type

- Saudi Arabian Managed Mobility Services (MMS) Market Overview by Deployment Type

- Saudi Arabian Managed Mobility Services (MMS) Market Overview by Company Type

- Saudi Arabian Managed Mobility Services (MMS) Market Overview by Industry Sector

- MOROCCO

- Moroccan Managed Mobility Services (MMS) Market Overview by Function Type

- Moroccan Managed Mobility Services (MMS) Market Overview by Deployment Type

- Moroccan Managed Mobility Services (MMS) Market Overview by Company Type

- Moroccan Managed Mobility Services (MMS) Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Managed Mobility Services (MMS) Market Overview by Function Type

- Kuwaiti Managed Mobility Services (MMS) Market Overview by Deployment Type

- Kuwaiti Managed Mobility Services (MMS) Market Overview by Company Type

- Kuwaiti Managed Mobility Services (MMS) Market Overview by Industry Sector

- QATAR

- Qatari Managed Mobility Services (MMS) Market Overview by Function Type

- Qatari Managed Mobility Services (MMS) Market Overview by Deployment Type

- Qatari Managed Mobility Services (MMS) Market Overview by Company Type

- Qatari Managed Mobility Services (MMS) Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Managed Mobility Services (MMS) Market Overview by Function Type

- Rest of Middle East & Africa Managed Mobility Services (MMS) Market Overview by Deployment Type

- Rest of Middle East & Africa Managed Mobility Services (MMS) Market Overview by Company Type

- Rest of Middle East & Africa Managed Mobility Services (MMS) Market Overview by Industry Sector

PART C: INDUSTRY GUIDE

PART D: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

Accenture

AT&T Business

Atos

Barrachd (Capita)

BT Global Services

Cancom

Capgemini

CDW

Cognizant

Computacenter

Deutsche Telekom (T-Systems)

DMI (Digital Management LLC)

DXC Technology

Fujitsu

GEMA (Global Enterprise Mobility Alliance)

HCLTech

IBM

Infosys

Insight Enterprises

Kyndryl

Mobliciti

NTT Ltd.

Orange Business Services

Presidio

SCC (Specialist Computer Centres)

Singtel Enterprise

Synnex / TD SYNNEX

Tata Consultancy Services (TCS)

Tech Data

Telefonica Tech

Verizon Business

Vodafone Business

Wipro

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |