Managed Cloud Services (MCS) - A Global Market Overview

- Published: Aug 2025

- Pages: 499 | Charts: 411

- Report Code: ITM023

SHARE THIS REPORT:

Global Managed Cloud Services (MCS) Market Trends and Outlook

The global Managed Cloud Services (MCS) market is undergoing a significant transformation, with total revenues projected to rise from US$73.9 billion in 2024 to US$164.5 billion by 2030, expanding at a CAGR of 14.3%. This robust growth reflects the escalating complexity of enterprise IT environments and the need for expert management across hybrid, multi-cloud, and edge architectures. Organizations are increasingly outsourcing cloud operations not just for cost optimization, but to enable business resilience, faster innovation, and regulatory alignment. While public cloud remains foundational, the fastest momentum is seen in hybrid deployments, automation services, and platform management-driven by the need for flexibility, security, and workload orchestration across environments.

Key growth drivers include accelerating digital transformation across industries, a global shortage of skilled cloud professionals, and the proliferation of AI/ML and edge computing. Enterprises are seeking MCS providers that can deliver outcome-based services-integrating observability, security, and compliance into unified platforms that scale with business demand. Meanwhile, the rise of generative AI, data sovereignty laws, and cloud-native modernization is reshaping the service delivery landscape. As a result, the MCS model is evolving from tactical infrastructure support to a strategic enabler of innovation and agility, with providers competing on value-added offerings such as AI Ops, FinOps, secure DevOps, and industry-specific cloud frameworks.

Managed Cloud Services (MCS) Regional Market Analysis

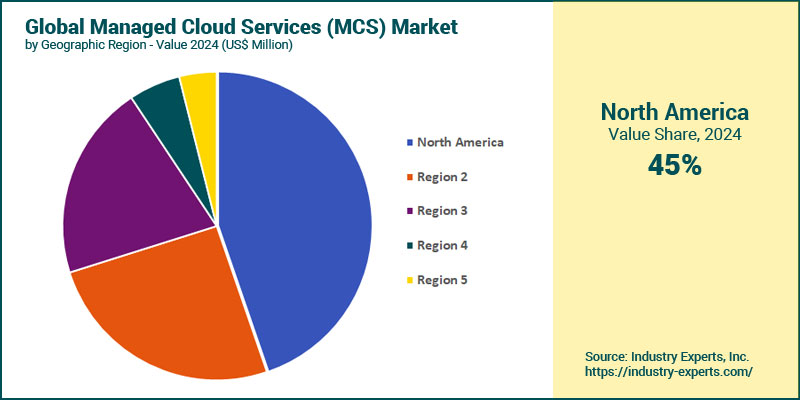

North America is the dominant region in the MCS market, contributing 44.8% of the global market in 2024. This leadership position is driven by its mature cloud infrastructure, high enterprise cloud penetration, and the strong presence of key hyperscalers such as AWS, Microsoft Azure, and Google Cloud. The region is expected to reach US$69 billion by 2030, maintaining its lead despite slower relative growth compared to emerging regions. North American enterprises are increasingly leveraging MCS for hybrid cloud management, security automation, and compliance readiness. Asia-Pacific is projected to grow at the fastest CAGR of 17.8% between 2024 and 2030, fueled by accelerated digital transformation across India, Southeast Asia, and China, with SMEs adopting cloud-native environments and leapfrogging traditional IT. The region's appetite for managed DevOps, cloud cost governance, and industry-specific compliance is contributing to the surge in demand.

Managed Cloud Services (MCS) Market Analysis by Deployment Type

Public cloud deployment holds the largest share of the global MCS market, contributing approximately 54.8% of total market value in 2024. Despite its size, public cloud growth is relatively moderate. The continued reliance on hyperscaler ecosystems like AWS, Azure, and GCP for IaaS, PaaS, and SaaS workloads sustains public cloud's dominance. However, rising security, latency, and compliance demands are gradually shifting attention toward more flexible deployment models. Hybrid cloud is expected to record the fastest CAGR at 16.1%, fueled by growing enterprise needs for workload portability, data sovereignty, and security customization. Industries under regulatory scrutiny, such as BFSI and healthcare, are increasingly opting for hybrid MCS offerings that blend public scalability with on-premise control.

Managed Cloud Services (MCS) Market Analysis by Service Type

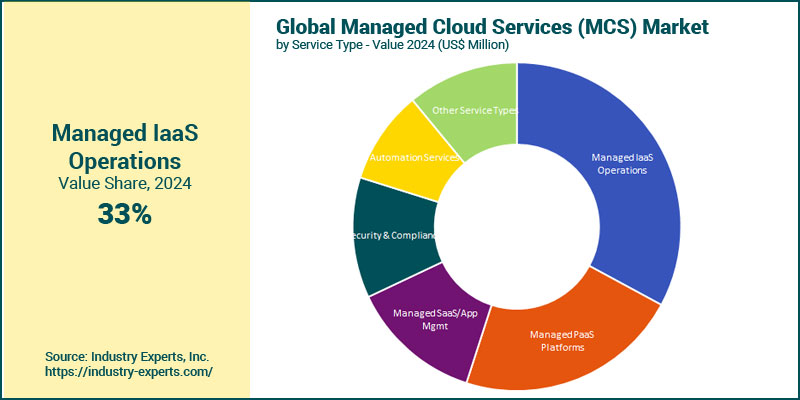

Managed IaaS Operations is the dominant service category, contributing approximately 32.9% of the total MCS market in 2024. This segment is expected to grow at a CAGR of 12.2%, fueled by enterprise reliance on infrastructure outsourcing for uptime assurance, SLA compliance, and workload optimization across public, private, and hybrid clouds. Managed PaaS Platforms is set to be the fastest-growing category, expanding at a CAGR of 16.4%. Demand is being driven by the need to streamline application development, enable DevOps automation, and support containerized workloads with built-in scalability and governance. This trend is closely followed by strong growth in Automation Services and Managed SaaS/Application Management, both reflecting increasing enterprise focus on agility, software lifecycle efficiency, and value-added support across complex environments.

Managed Cloud Services (MCS) Market Analysis by Company Type

Large enterprises continue to command the majority of global MCS spending in 2024, contributing 67.9% of the total market. Large organizations are investing heavily in hybrid and multi-cloud MCS strategies, particularly to meet operational complexity, global compliance mandates, and integration of AI and edge capabilities across vast digital estates. These enterprises also drive demand for managed security, observability, and workload portability across environments. Small and mid-sized enterprises (SMEs) are projected to grow at a CAGR of 17%, outpacing their larger counterparts. This surge is being driven by the democratization of cloud-native platforms and the rise of simplified, scalable managed service offerings. SMEs, particularly in Asia-Pacific and Latin America, are embracing MCS as a means to avoid costly in-house IT operations while maintaining agility and security. Industry-specific managed service bundles and AI-powered automation are helping accelerate this adoption curve.

Managed Cloud Services (MCS) Market Analysis by Industry Sector

Banking, Financial Services, and Insurance (BFSI) is the top industry in the MCS market, with a share of 19.5% of total global revenue in 2024. With a projected value of US$32 billion by 2030, BFSI will grow at a CAGR of 14.3%, sustaining its leadership throughout the forecast period. The segment's demand is driven by the need for continuous availability, real-time fraud detection, risk analytics, and regulatory compliance. Financial institutions are adopting hybrid MCS models to support secure data localization, advanced governance, and automation of mission-critical workloads. Retail & E-commerce will experience the fastest growth, with a CAGR of 19.3%. This rapid expansion is fueled by global omnichannel transformation, personalized customer engagement, and the need for scalable infrastructure to support seasonal surges and AI-driven customer analytics. Healthcare follows closely, reflecting growing adoption of MCS for HIPAA-compliant data storage, diagnostics automation, and AI/ML model hosting in digital health ecosystems.

Managed Cloud Services (MCS) Market Report Scope

This global report on Managed Cloud Services (MCS) market analyzes the global and regional market based on Deployment Type, Service Type, Company Type, and Industry Sector for the period 2021-2030 with forecasts from 2024 to 2030 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Historical Period: | 2021-2024 | |

| Base Year: | 2024 | |

| Forecast Period: | 2024-2030 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 35+ |

Managed Cloud Services (MCS) Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Managed Cloud Services (MCS) Market by Deployment Type

- Public Cloud

- Private Cloud

- Hybrid Cloud

Managed Cloud Services (MCS) Market by Service Type

- Managed IaaS Operations

- Managed PaaS Platforms

- Managed SaaS/App Management

- Security & Compliance

- Automation Services

- Other Service Types

Managed Cloud Services (MCS) Market by Company Type

- Large Enterprises

- Small-to-medium Enterprises (SMEs)

Managed Cloud Services (MCS) Market by Industry Sector

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

Managed Cloud Services (MCS) Market Frequently Asked Questions (FAQs)

As of 2024, the global MCS market is valued at approximately US$73.9 billion, with strong demand from enterprises seeking managed infrastructure, automation, and compliance support across public, private, and hybrid clouds.

The global MCS market is projected to grow at a CAGR of 14.3% from 2024 to 2030, reaching US$164.5 billion by 2030, driven by cloud complexity, digital transformation, AI/ML integration, and compliance pressures.

North America leads the market with over US$33.1 billion in 2024, thanks to mature cloud infrastructure, enterprise cloud maturity, and the dominance of key providers like AWS, Microsoft Azure, and Google Cloud.

Asia-Pacific is the fastest-growing region, projected to expand at a 17.8% CAGR, as SMEs and digital-native businesses in India, Southeast Asia, and China drive rapid adoption of cloud-native managed services.

Major trends include AI-powered automation, hybrid and multi-cloud orchestration, FinOps and cloud cost governance, DevSecOps enablement, data sovereignty solutions, and managed edge-to-cloud infrastructure.

Hybrid cloud is the fastest-growing deployment model, with a 16.1% CAGR, as enterprises seek flexibility, data localization, and secure workload portability across environments.

Key providers include Cognizant, TCS, Infosys, Wipro, HCLTech, DXC Technology, AWS Managed Services, Microsoft Azure Managed Applications, Google Cloud MSPs, Rackspace, and a range of niche cloud-native firms.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Managed Cloud Services (MCS)

- Market Segmentation for Managed Cloud Services (MCS)

- Deployment Types

- Service Types

- Company Types

- Industry Sectors

- Key Trends in Managed Cloud Services (MCS) Market

2. INDUSTRY LANDSCAPE

- Global Managed Cloud Services (MCS) Market Outlook

- Comprehensive Managed Cloud Services (MCS) Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Managed Cloud Services (MCS) Industry

- Startup Strategies for Managed Cloud Services (MCS) Industry

- SWOT Analysis of Managed Cloud Services (MCS) Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Managed Cloud Services (MCS) Companies

- Market Share Analysis of Managed Cloud Services (MCS) Companies

- SWOT Analysis of Key Players in the Managed Cloud Services (MCS) Industry

- Key Market Players

- 2nd Watch

- 8K Miles

- Accenture

- AHEAD

- AllCloud

- AWS Managed Services (AMS)

- BitTitan

- Capgemini

- Claranet

- Cloudnexa

- Cloudreach

- Cognizant

- Contino

- DataBank

- DXC Technology

- Ensono

- Google Cloud

- HCLTech

- IBM

- Infosys

- Leaseweb

- Logicworks

- Microsoft Azure

- Mission Cloud

- Navisite

- Nordcloud

- NTT Ltd.

- Onica (Rackspace)

- OpsRamp

- OVHcloud

- PhoenixNAP

- Rackspace Technology

- Softchoice

- Tata Consultancy Services (TCS)

- Wipro

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Managed Cloud Services (MCS) Market Overview by Deployment Type

- Managed Cloud Services (MCS) Deployment Type Market Overview by Global Region

- Public Cloud

- Private Cloud

- Hybrid Cloud

- Global Managed Cloud Services (MCS) Market Overview by Service Type

- Managed Cloud Services (MCS) Service Type Market Overview by Global Region

- Managed IaaS Operations

- Managed PaaS Platforms

- Managed SaaS/App Management

- Security & Compliance

- Automation Services

- Other Service Types

- Global Managed Cloud Services (MCS) Market Overview by Company Type

- Managed Cloud Services (MCS) Company Type Market Overview by Global Region

- Large Enterprises

- SMEs

- Global Managed Cloud Services (MCS) Market Overview by Industry Sector

- Managed Cloud Services (MCS) Industry Sector Market Overview by Global Region

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

PART B: REGIONAL MARKET PERSPECTIVE

- Global Managed Cloud Services (MCS) Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Managed Cloud Services (MCS) Market Overview by Geographic Region

- North American Managed Cloud Services (MCS) Market Overview by Deployment Type

- North American Managed Cloud Services (MCS) Market Overview by Service Type

- North American Managed Cloud Services (MCS) Market Overview by Company Type

- North American Managed Cloud Services (MCS) Market Overview by Industry Sector

- Country-wise Analysis of North American Managed Cloud Services (MCS) Market

- THE UNITED STATES

- United States Managed Cloud Services (MCS) Market Overview by Deployment Type

- United States Managed Cloud Services (MCS) Market Overview by Service Type

- United States Managed Cloud Services (MCS) Market Overview by Company Type

- United States Managed Cloud Services (MCS) Market Overview by Industry Sector

- CANADA

- Canadian Managed Cloud Services (MCS) Market Overview by Deployment Type

- Canadian Managed Cloud Services (MCS) Market Overview by Service Type

- Canadian Managed Cloud Services (MCS) Market Overview by Company Type

- Canadian Managed Cloud Services (MCS) Market Overview by Industry Sector

- MEXICO

- Mexican Managed Cloud Services (MCS) Market Overview by Deployment Type

- Mexican Managed Cloud Services (MCS) Market Overview by Service Type

- Mexican Managed Cloud Services (MCS) Market Overview by Company Type

- Mexican Managed Cloud Services (MCS) Market Overview by Industry Sector

7. EUROPE

- European Managed Cloud Services (MCS) Market Overview by Geographic Region

- European Managed Cloud Services (MCS) Market Overview by Deployment Type

- European Managed Cloud Services (MCS) Market Overview by Service Type

- European Managed Cloud Services (MCS) Market Overview by Company Type

- European Managed Cloud Services (MCS) Market Overview by Industry Sector

- Country-wise Analysis of European Managed Cloud Services (MCS) Market

- GERMANY

- German Managed Cloud Services (MCS) Market Overview by Deployment Type

- German Managed Cloud Services (MCS) Market Overview by Service Type

- German Managed Cloud Services (MCS) Market Overview by Company Type

- German Managed Cloud Services (MCS) Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Managed Cloud Services (MCS) Market Overview by Deployment Type

- United Kingdom Managed Cloud Services (MCS) Market Overview by Service Type

- United Kingdom Managed Cloud Services (MCS) Market Overview by Company Type

- United Kingdom Managed Cloud Services (MCS) Market Overview by Industry Sector

- FRANCE

- French Managed Cloud Services (MCS) Market Overview by Deployment Type

- French Managed Cloud Services (MCS) Market Overview by Service Type

- French Managed Cloud Services (MCS) Market Overview by Company Type

- French Managed Cloud Services (MCS) Market Overview by Industry Sector

- ITALY

- Italian Managed Cloud Services (MCS) Market Overview by Deployment Type

- Italian Managed Cloud Services (MCS) Market Overview by Service Type

- Italian Managed Cloud Services (MCS) Market Overview by Company Type

- Italian Managed Cloud Services (MCS) Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Managed Cloud Services (MCS) Market Overview by Deployment Type

- Dutch Managed Cloud Services (MCS) Market Overview by Service Type

- Dutch Managed Cloud Services (MCS) Market Overview by Company Type

- Dutch Managed Cloud Services (MCS) Market Overview by Industry Sector

- SPAIN

- Spanish Managed Cloud Services (MCS) Market Overview by Deployment Type

- Spanish Managed Cloud Services (MCS) Market Overview by Service Type

- Spanish Managed Cloud Services (MCS) Market Overview by Company Type

- Spanish Managed Cloud Services (MCS) Market Overview by Industry Sector

- RUSSIA

- Russian Managed Cloud Services (MCS) Market Overview by Deployment Type

- Russian Managed Cloud Services (MCS) Market Overview by Service Type

- Russian Managed Cloud Services (MCS) Market Overview by Company Type

- Russian Managed Cloud Services (MCS) Market Overview by Industry Sector

- SWITZERLAND

- Swiss Managed Cloud Services (MCS) Market Overview by Deployment Type

- Swiss Managed Cloud Services (MCS) Market Overview by Service Type

- Swiss Managed Cloud Services (MCS) Market Overview by Company Type

- Swiss Managed Cloud Services (MCS) Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Managed Cloud Services (MCS) Market Overview by Deployment Type

- Rest of Europe Managed Cloud Services (MCS) Market Overview by Service Type

- Rest of Europe Managed Cloud Services (MCS) Market Overview by Company Type

- Rest of Europe Managed Cloud Services (MCS) Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Managed Cloud Services (MCS) Market Overview by Geographic Region

- Asia-Pacific Managed Cloud Services (MCS) Market Overview by Deployment Type

- Asia-Pacific Managed Cloud Services (MCS) Market Overview by Service Type

- Asia-Pacific Managed Cloud Services (MCS) Market Overview by Company Type

- Asia-Pacific Managed Cloud Services (MCS) Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Managed Cloud Services (MCS) Market

- CHINA

- Chinese Managed Cloud Services (MCS) Market Overview by Deployment Type

- Chinese Managed Cloud Services (MCS) Market Overview by Service Type

- Chinese Managed Cloud Services (MCS) Market Overview by Company Type

- Chinese Managed Cloud Services (MCS) Market Overview by Industry Sector

- JAPAN

- Japanese Managed Cloud Services (MCS) Market Overview by Deployment Type

- Japanese Managed Cloud Services (MCS) Market Overview by Service Type

- Japanese Managed Cloud Services (MCS) Market Overview by Company Type

- Japanese Managed Cloud Services (MCS) Market Overview by Industry Sector

- INDIA

- Indian Managed Cloud Services (MCS) Market Overview by Deployment Type

- Indian Managed Cloud Services (MCS) Market Overview by Service Type

- Indian Managed Cloud Services (MCS) Market Overview by Company Type

- Indian Managed Cloud Services (MCS) Market Overview by Industry Sector

- AUSTRALIA

- Australia Managed Cloud Services (MCS) Market Overview by Deployment Type

- Australia Managed Cloud Services (MCS) Market Overview by Service Type

- Australia Managed Cloud Services (MCS) Market Overview by Company Type

- Australia Managed Cloud Services (MCS) Market Overview by Industry Sector

- SINGAPORE

- Singaporean Managed Cloud Services (MCS) Market Overview by Deployment Type

- Singaporean Managed Cloud Services (MCS) Market Overview by Service Type

- Singaporean Managed Cloud Services (MCS) Market Overview by Company Type

- Singaporean Managed Cloud Services (MCS) Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Managed Cloud Services (MCS) Market Overview by Deployment Type

- South Korean Managed Cloud Services (MCS) Market Overview by Service Type

- South Korean Managed Cloud Services (MCS) Market Overview by Company Type

- South Korean Managed Cloud Services (MCS) Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Managed Cloud Services (MCS) Market Overview by Deployment Type

- Rest of Asia-Pacific Managed Cloud Services (MCS) Market Overview by Service Type

- Rest of Asia-Pacific Managed Cloud Services (MCS) Market Overview by Company Type

- Rest of Asia-Pacific Managed Cloud Services (MCS) Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Managed Cloud Services (MCS) Market Overview by Geographic Region

- South American Managed Cloud Services (MCS) Market Overview by Deployment Type

- South American Managed Cloud Services (MCS) Market Overview by Service Type

- South American Managed Cloud Services (MCS) Market Overview by Company Type

- South American Managed Cloud Services (MCS) Market Overview by Industry Sector

- Country-wise Analysis of South American Managed Cloud Services (MCS) Market

- BRAZIL

- Brazilian Managed Cloud Services (MCS) Market Overview by Deployment Type

- Brazilian Managed Cloud Services (MCS) Market Overview by Service Type

- Brazilian Managed Cloud Services (MCS) Market Overview by Company Type

- Brazilian Managed Cloud Services (MCS) Market Overview by Industry Sector

- ARGENTINA

- Argentine Managed Cloud Services (MCS) Market Overview by Deployment Type

- Argentine Managed Cloud Services (MCS) Market Overview by Service Type

- Argentine Managed Cloud Services (MCS) Market Overview by Company Type

- Argentine Managed Cloud Services (MCS) Market Overview by Industry Sector

- COLOMBIA

- Colombian Managed Cloud Services (MCS) Market Overview by Deployment Type

- Colombian Managed Cloud Services (MCS) Market Overview by Service Type

- Colombian Managed Cloud Services (MCS) Market Overview by Company Type

- Colombian Managed Cloud Services (MCS) Market Overview by Industry Sector

- CHILE

- Chilean Managed Cloud Services (MCS) Market Overview by Deployment Type

- Chilean Managed Cloud Services (MCS) Market Overview by Service Type

- Chilean Managed Cloud Services (MCS) Market Overview by Company Type

- Chilean Managed Cloud Services (MCS) Market Overview by Industry Sector

- PERU

- Peruvian Managed Cloud Services (MCS) Market Overview by Deployment Type

- Peruvian Managed Cloud Services (MCS) Market Overview by Service Type

- Peruvian Managed Cloud Services (MCS) Market Overview by Company Type

- Peruvian Managed Cloud Services (MCS) Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Managed Cloud Services (MCS) Market Overview by Deployment Type

- Rest of South America Managed Cloud Services (MCS) Market Overview by Service Type

- Rest of South America Managed Cloud Services (MCS) Market Overview by Company Type

- Rest of South America Managed Cloud Services (MCS) Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Managed Cloud Services (MCS) Market Overview by Geographic Region

- Middle East & Africa Managed Cloud Services (MCS) Market Overview by Deployment Type

- Middle East & Africa Managed Cloud Services (MCS) Market Overview by Service Type

- Middle East & Africa Managed Cloud Services (MCS) Market Overview by Company Type

- Middle East & Africa Managed Cloud Services (MCS) Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Managed Cloud Services (MCS) Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Managed Cloud Services (MCS) Market Overview by Deployment Type

- United Arab Emirates Managed Cloud Services (MCS) Market Overview by Service Type

- United Arab Emirates Managed Cloud Services (MCS) Market Overview by Company Type

- United Arab Emirates Managed Cloud Services (MCS) Market Overview by Industry Sector

- SOUTH AFRICA

- South African Managed Cloud Services (MCS) Market Overview by Deployment Type

- South African Managed Cloud Services (MCS) Market Overview by Service Type

- South African Managed Cloud Services (MCS) Market Overview by Company Type

- South African Managed Cloud Services (MCS) Market Overview by Industry Sector

- EGYPT

- Egyptian Managed Cloud Services (MCS) Market Overview by Deployment Type

- Egyptian Managed Cloud Services (MCS) Market Overview by Service Type

- Egyptian Managed Cloud Services (MCS) Market Overview by Company Type

- Egyptian Managed Cloud Services (MCS) Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Managed Cloud Services (MCS) Market Overview by Deployment Type

- Saudi Arabian Managed Cloud Services (MCS) Market Overview by Service Type

- Saudi Arabian Managed Cloud Services (MCS) Market Overview by Company Type

- Saudi Arabian Managed Cloud Services (MCS) Market Overview by Industry Sector

- MOROCCO

- Moroccan Managed Cloud Services (MCS) Market Overview by Deployment Type

- Moroccan Managed Cloud Services (MCS) Market Overview by Service Type

- Moroccan Managed Cloud Services (MCS) Market Overview by Company Type

- Moroccan Managed Cloud Services (MCS) Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Managed Cloud Services (MCS) Market Overview by Deployment Type

- Kuwaiti Managed Cloud Services (MCS) Market Overview by Service Type

- Kuwaiti Managed Cloud Services (MCS) Market Overview by Company Type

- Kuwaiti Managed Cloud Services (MCS) Market Overview by Industry Sector

- QATAR

- Qatari Managed Cloud Services (MCS) Market Overview by Deployment Type

- Qatari Managed Cloud Services (MCS) Market Overview by Service Type

- Qatari Managed Cloud Services (MCS) Market Overview by Company Type

- Qatari Managed Cloud Services (MCS) Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Managed Cloud Services (MCS) Market Overview by Deployment Type

- Rest of Middle East & Africa Managed Cloud Services (MCS) Market Overview by Service Type

- Rest of Middle East & Africa Managed Cloud Services (MCS) Market Overview by Company Type

- Rest of Middle East & Africa Managed Cloud Services (MCS) Market Overview by Industry Sector

PART C: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

2nd Watch

8K Miles

Accenture

AHEAD

AllCloud

AWS Managed Services (AMS)

BitTitan

Capgemini

Claranet

Cloudnexa

Cloudreach

Cognizant

Contino

DataBank

DXC Technology

Ensono

Google Cloud

HCLTech

IBM

Infosys

Leaseweb

Logicworks

Microsoft Azure

Mission Cloud

Navisite

Nordcloud

NTT Ltd.

Onica (Rackspace)

OpsRamp

OVHcloud

PhoenixNAP

Rackspace Technology

Softchoice

Tata Consultancy Services (TCS)

Wipro

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |