Internet of Things (IoT) Hardware - A Global Market Overview

- Published: Aug 2025

- Pages: 502 | Charts: 413

- Report Code: ITM069

SHARE THIS REPORT:

Global Internet of Things (IoT) Hardware Market Trends and Outlook

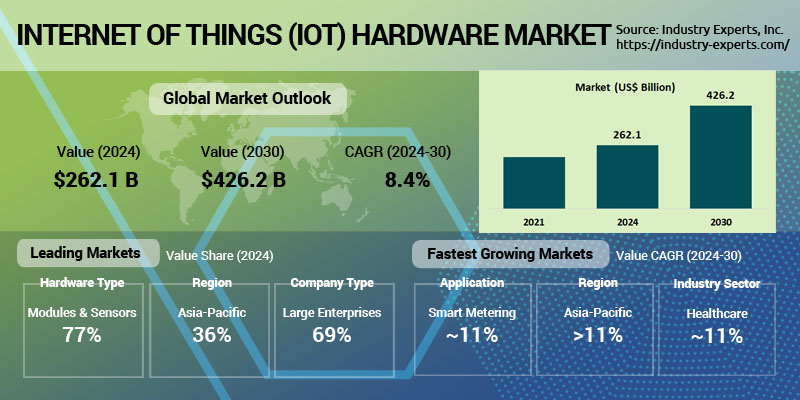

The global Internet of Things (IoT) hardware market is witnessing rapid evolution as edge computing, AI integration, and industry-specific demands reshape its strategic role across digital infrastructure. Valued at approximately US$262.1 billion in 2024, IoT hardware accounts for nearly 35% of total IoT spending, underscoring its critical position in enabling real-time, decentralized decision-making. Comprising sensors, secure modules, edge servers, storage, and embedded systems, these components serve as the interface between the physical world and digital platforms.

By 2030, the market is projected to reach US$426.2 billion, registering a CAGR of 8.4% between 2024 and 2030. Growth is being driven by widespread adoption across manufacturing, utilities, transportation, and healthcare sectors. Trends such as AI-capable modules, secure edge hardware, and vertically tailored device ecosystems are fueling market expansion. Asia-Pacific leads the market both in size and momentum, while North America continues to innovate in secure, standards-driven deployments. SMEs are emerging as a key growth driver, embracing cost-effective and scalable hardware solutions tailored for their needs.

Major players in the global IoT hardware market include Intel, Qualcomm, Texas Instruments, STMicroelectronics, Bosch Sensortec, NXP Semiconductors, Renesas, Advantech, Huawei, and Murata, among others. These companies lead the ecosystem in sensor development, secure microcontrollers, edge computing modules, and domain-specific hardware innovations.

Internet of Things (IoT) Hardware Regional Market Analysis

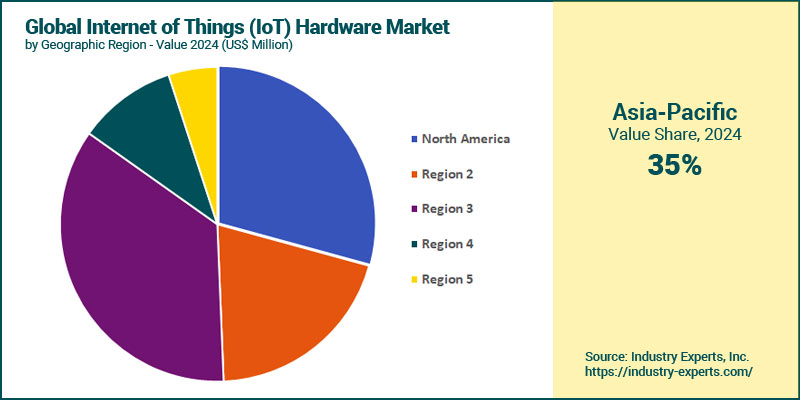

Among all regions, Asia-Pacific dominates the global market with an estimated 35.5% share of global IoT hardware spending in 2024. This dominance is primarily attributed to robust deployments in China, India, Japan, and South Korea, driven by aggressive smart manufacturing initiatives, national digital infrastructure programs, and high adoption across utilities and transportation sectors. North America follows as the second-largest regional market, fueled by early enterprise adoption, edge-native infrastructure, and security-focused innovation in sectors such as healthcare, automotive, and energy. In terms of growth trajectory, Asia-Pacific is forecast to be the fastest-growing region, expanding at a CAGR of 11.1% between 2024 and 2030. This rapid growth is underpinned by government-backed smart city initiatives, 5G deployments, industrial IoT (IIoT) investments, and the emergence of edge-AI enabled modules tailored for local and vertical-specific needs.

Internet of Things (IoT) Hardware Market Analysis by Hardware Type

The IoT hardware market is led by the Modules & Sensors segment, accounting for 77% of the total market in 2024. This dominance is attributed to the pervasive use of smart sensors and connectivity modules in virtually every IoT deployment, from industrial automation and environmental monitoring to consumer electronics and smart cities. These components form the foundational layer of IoT infrastructure, capturing and transmitting real-time data from edge environments to cloud platforms. With strong demand across industrial, transportation, healthcare, and energy sectors, this segment will continue to anchor market value through the decade. However, the fastest-growing segment is Security Hardware, projected to expand at a CAGR of 12.3% between 2024 and 2030. The surge in demand for secure elements, TPMs, hardware encryption modules, and secure microcontrollers is being driven by increasing IoT security threats, privacy regulations, and the critical need for tamper-proof data integrity, especially in sectors like automotive, healthcare, finance, and critical infrastructure.

Internet of Things (IoT) Hardware Market Analysis by Application

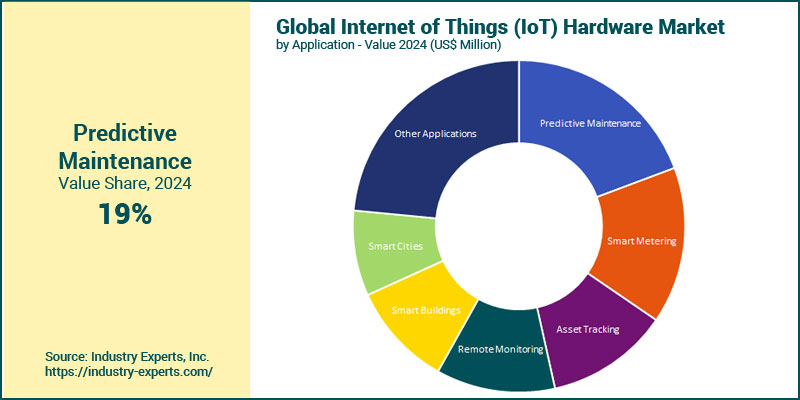

In 2024, Predictive Maintenance is the largest application area for IoT hardware, contributing 19.3% of the global market. Its dominance is fueled by widespread adoption across industrial and manufacturing sectors, where downtime prevention, equipment longevity, and operational efficiency are critical. Sensor-driven hardware combined with edge intelligence enables real-time condition monitoring and fault detection across factories, logistics, energy plants, and transportation systems. Smart Metering emerges as the second-largest application. Utility providers across electricity, gas, and water networks continue to deploy smart meters for remote diagnostics, usage-based billing, and grid optimization. Regulatory mandates and sustainability targets in developed and emerging markets alike are further accelerating smart metering installations. In terms of growth momentum, Smart Metering is also the fastest-growing segment, projected to expand at a CAGR of 10.5%. This growth is driven by government-backed smart grid rollouts, electrification trends, and rising demand for resource efficiency in cities and industrial parks.

Internet of Things (IoT) Hardware Market Analysis by Company Type

Large enterprises continue to represent the majority of IoT hardware spending, accounting for 68.5% of global market value. This dominance stems from their substantial investments in industrial automation, digital transformation, smart manufacturing, and infrastructure projects across sectors such as automotive, energy, utilities, and logistics. These organizations are integrating advanced edge hardware, AI-powered modules, and secure gateways to enhance real-time decision-making and resilience at scale. However, SMEs are the fastest-growing user group, projected to expand at a CAGR of 9.4% from 2024 to 2030. This acceleration is driven by the rising availability of affordable, plug-and-play IoT hardware solutions, combined with cloud-native platforms that reduce setup complexity and cost barriers. Key SME-led adoption areas include smart farming, remote asset monitoring, retail automation, and building management, particularly in Asia-Pacific and South America, where government-backed digitalization initiatives and startup ecosystems are flourishing.

Internet of Things (IoT) Hardware Market Analysis by Industry Sector

Manufacturing remains the leading vertical for IoT hardware investments, representing 24.9% of the global market in 2024. This leadership is reinforced by ongoing investments in Industry 4.0, predictive maintenance, machine condition monitoring, and factory automation across major economies. As industrial enterprises continue to scale digital twins, AI-driven production optimization, and real-time quality control, manufacturing will retain its central role in hardware consumption, reaching US$99.1 billion by 2030 at a CAGR of 7.2%. Healthcare is projected to be the fastest-growing industry sector, advancing at a CAGR of 10.8% through 2030. This rapid expansion is driven by the proliferation of remote patient monitoring (RPM), connected medical devices, IoT-enabled diagnostics, and hospital asset tracking. The post-pandemic digital health boom and aging population trends have made IoT hardware essential in improving care delivery and operational efficiency.

Internet of Things (IoT) Hardware Market Report Scope

This global report on Internet of Things (IoT) Hardware market analyzes the global and regional market based on Hardware Type, Application, Company Type and Industry Sector for the period 2021-2030 with forecasts from 2024 to 2030 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Historical Period: | 2021-2024 | |

| Base Year: | 2024 | |

| Forecast Period: | 2024-2030 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 35+ |

Internet of Things (IoT) Hardware Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Internet of Things (IoT) Hardware Market by Hardware Type

- Modules & Sensors

- Security Hardware

- Servers

- Storage

- Other Hardware Types

Internet of Things (IoT) Hardware Market by Application

- Predictive Maintenance

- Smart Metering

- Asset Tracking

- Remote Monitoring

- Smart Buildings

- Smart Cities

- Other Applications

Internet of Things (IoT) Hardware Market by Company Type

- Large Enterprises

- SMEs

Internet of Things (IoT) Hardware Market by Industry Sector

- Manufacturing

- Utilities

- Transportation

- Retail

- Healthcare

- Government & Public

- Cross-industry

- Other Industry Sectors

Internet of Things (IoT) Hardware Market Frequently Asked Questions (FAQs)

The market is valued at approximately US$262.1 billion in 2024, accounting for 35% of total global IoT spending.

The IoT hardware market is expected to reach US$426.2 billion by 2030, growing at a CAGR of 8.4% from 2024.

Asia-Pacific leads the global market with a 35.4% share in 2024 and is also the fastest-growing region (11.1% CAGR).

Modules and sensors dominate the market, contributing over 80% of total hardware spending in 2024.

Security hardware is the fastest-growing segment, with a CAGR of 12.3%, driven by increasing cyber threats and compliance needs.

Smart Metering is the fastest-growing application, with a CAGR of 10.5%, fueled by utility digitalization and smart grid rollouts.

Yes, SMEs are the fastest-growing company segment, with 9.4% CAGR, driven by low-cost, scalable IoT solutions for remote monitoring and automation.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Internet of Things (IoT) Hardware

- Market Segmentation for Internet of Things (IoT) Hardware

- Hardware Types

- Applications

- Company Types

- Industry Sectors

- Key Trends in Internet of Things (IoT) Hardware Market

2. INDUSTRY LANDSCAPE

- Global Internet of Things (IoT) Hardware Market Outlook

- Comprehensive Internet of Things (IoT) Hardware Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Internet of Things (IoT) Hardware Industry

- Startup Strategies for Internet of Things (IoT) Hardware Industry

- SWOT Analysis of Internet of Things (IoT) Hardware Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Internet of Things (IoT) Hardware Companies

- Market Share Analysis of Internet of Things (IoT) Hardware Companies

- SWOT Analysis of Key Players in the Internet of Things (IoT) Hardware Industry

- Key Market Players

- ABB

- Advantech

- Bosch (Rexroth, Sensortec)

- Cisco

- Dell Technologies

- Dragino

- Emerson Electric

- Espressif Systems

- FOSSA Systems

- Garmin

- Honeywell

- HPE

- Infineon Technologies

- Libelium

- Lumotive

- MediaTek

- Microchip Technology

- Murata Manufacturing

- Myriota

- Nordic Semiconductor

- NXP Semiconductors

- Panasonic

- Particle.io

- Qualcomm

- Quectel Wireless

- Schneider Electric

- Seeed Studio

- Semtech

- Siemens

- STMicroelectronics

- Stratus Technologies

- Telit Cinterion

- Texas Instruments

- u-blox

- Wiliot

- Zebra Technologies

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Internet of Things (IoT) Hardware Type Market Overview by Global Region

- Modules & Sensors

- Security Hardware

- Servers

- Storage

- Other Hardware Types

- Global Internet of Things (IoT) Hardware Market Overview by Application

- Internet of Things (IoT) Hardware Application Market Overview by Global Region

- Predictive Maintenance

- Smart Metering

- Asset Tracking

- Remote Monitoring

- Smart Buildings

- Smart Cities

- Other Applications

- Global Internet of Things (IoT) Hardware Market Overview by Company Type

- Internet of Things (IoT) Hardware Company Type Market Overview by Global Region

- Large Enterprises

- SMEs

- Global Internet of Things (IoT) Hardware Market Overview by Industry Sector

- Internet of Things (IoT) Hardware Industry Sector Market Overview by Global Region

- Manufacturing

- Utilities

- Transportation

- Retail

- Healthcare

- Government & Public

- Cross-industry

- Other Industry Sectors

PART B: REGIONAL MARKET PERSPECTIVE

- Global Internet of Things (IoT) Hardware Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Internet of Things (IoT) Hardware Market Overview by Geographic Region

- North American Internet of Things (IoT) Hardware Market Overview by Hardware Type

- North American Internet of Things (IoT) Hardware Market Overview by Application

- North American Internet of Things (IoT) Hardware Market Overview by Company Type

- North American Internet of Things (IoT) Hardware Market Overview by Industry Sector

- Country-wise Analysis of North American Internet of Things (IoT) Hardware Market

- THE UNITED STATES

- United States Internet of Things (IoT) Hardware Market Overview by Hardware Type

- United States Internet of Things (IoT) Hardware Market Overview by Application

- United States Internet of Things (IoT) Hardware Market Overview by Company Type

- United States Internet of Things (IoT) Hardware Market Overview by Industry Sector

- CANADA

- Canadian Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Canadian Internet of Things (IoT) Hardware Market Overview by Application

- Canadian Internet of Things (IoT) Hardware Market Overview by Company Type

- Canadian Internet of Things (IoT) Hardware Market Overview by Industry Sector

- MEXICO

- Mexican Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Mexican Internet of Things (IoT) Hardware Market Overview by Application

- Mexican Internet of Things (IoT) Hardware Market Overview by Company Type

- Mexican Internet of Things (IoT) Hardware Market Overview by Industry Sector

7. EUROPE

- European Internet of Things (IoT) Hardware Market Overview by Geographic Region

- European Internet of Things (IoT) Hardware Market Overview by Hardware Type

- European Internet of Things (IoT) Hardware Market Overview by Application

- European Internet of Things (IoT) Hardware Market Overview by Company Type

- European Internet of Things (IoT) Hardware Market Overview by Industry Sector

- Country-wise Analysis of European Internet of Things (IoT) Hardware Market

- GERMANY

- German Internet of Things (IoT) Hardware Market Overview by Hardware Type

- German Internet of Things (IoT) Hardware Market Overview by Application

- German Internet of Things (IoT) Hardware Market Overview by Company Type

- German Internet of Things (IoT) Hardware Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Internet of Things (IoT) Hardware Market Overview by Hardware Type

- United Kingdom Internet of Things (IoT) Hardware Market Overview by Application

- United Kingdom Internet of Things (IoT) Hardware Market Overview by Company Type

- United Kingdom Internet of Things (IoT) Hardware Market Overview by Industry Sector

- FRANCE

- French Internet of Things (IoT) Hardware Market Overview by Hardware Type

- French Internet of Things (IoT) Hardware Market Overview by Application

- French Internet of Things (IoT) Hardware Market Overview by Company Type

- French Internet of Things (IoT) Hardware Market Overview by Industry Sector

- ITALY

- Italian Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Italian Internet of Things (IoT) Hardware Market Overview by Application

- Italian Internet of Things (IoT) Hardware Market Overview by Company Type

- Italian Internet of Things (IoT) Hardware Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Dutch Internet of Things (IoT) Hardware Market Overview by Application

- Dutch Internet of Things (IoT) Hardware Market Overview by Company Type

- Dutch Internet of Things (IoT) Hardware Market Overview by Industry Sector

- SPAIN

- Spanish Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Spanish Internet of Things (IoT) Hardware Market Overview by Application

- Spanish Internet of Things (IoT) Hardware Market Overview by Company Type

- Spanish Internet of Things (IoT) Hardware Market Overview by Industry Sector

- RUSSIA

- Russian Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Russian Internet of Things (IoT) Hardware Market Overview by Application

- Russian Internet of Things (IoT) Hardware Market Overview by Company Type

- Russian Internet of Things (IoT) Hardware Market Overview by Industry Sector

- SWITZERLAND

- Swiss Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Swiss Internet of Things (IoT) Hardware Market Overview by Application

- Swiss Internet of Things (IoT) Hardware Market Overview by Company Type

- Swiss Internet of Things (IoT) Hardware Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Rest of Europe Internet of Things (IoT) Hardware Market Overview by Application

- Rest of Europe Internet of Things (IoT) Hardware Market Overview by Company Type

- Rest of Europe Internet of Things (IoT) Hardware Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Internet of Things (IoT) Hardware Market Overview by Geographic Region

- Asia-Pacific Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Asia-Pacific Internet of Things (IoT) Hardware Market Overview by Application

- Asia-Pacific Internet of Things (IoT) Hardware Market Overview by Company Type

- Asia-Pacific Internet of Things (IoT) Hardware Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Internet of Things (IoT) Hardware Market

- CHINA

- Chinese Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Chinese Internet of Things (IoT) Hardware Market Overview by Application

- Chinese Internet of Things (IoT) Hardware Market Overview by Company Type

- Chinese Internet of Things (IoT) Hardware Market Overview by Industry Sector

- JAPAN

- Japanese Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Japanese Internet of Things (IoT) Hardware Market Overview by Application

- Japanese Internet of Things (IoT) Hardware Market Overview by Company Type

- Japanese Internet of Things (IoT) Hardware Market Overview by Industry Sector

- INDIA

- Indian Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Indian Internet of Things (IoT) Hardware Market Overview by Application

- Indian Internet of Things (IoT) Hardware Market Overview by Company Type

- Indian Internet of Things (IoT) Hardware Market Overview by Industry Sector

- AUSTRALIA

- Australia Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Australia Internet of Things (IoT) Hardware Market Overview by Application

- Australia Internet of Things (IoT) Hardware Market Overview by Company Type

- Australia Internet of Things (IoT) Hardware Market Overview by Industry Sector

- SINGAPORE

- Singaporean Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Singaporean Internet of Things (IoT) Hardware Market Overview by Application

- Singaporean Internet of Things (IoT) Hardware Market Overview by Company Type

- Singaporean Internet of Things (IoT) Hardware Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Internet of Things (IoT) Hardware Market Overview by Hardware Type

- South Korean Internet of Things (IoT) Hardware Market Overview by Application

- South Korean Internet of Things (IoT) Hardware Market Overview by Company Type

- South Korean Internet of Things (IoT) Hardware Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Rest of Asia-Pacific Internet of Things (IoT) Hardware Market Overview by Application

- Rest of Asia-Pacific Internet of Things (IoT) Hardware Market Overview by Company Type

- Rest of Asia-Pacific Internet of Things (IoT) Hardware Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Internet of Things (IoT) Hardware Market Overview by Geographic Region

- South American Internet of Things (IoT) Hardware Market Overview by Hardware Type

- South American Internet of Things (IoT) Hardware Market Overview by Application

- South American Internet of Things (IoT) Hardware Market Overview by Company Type

- South American Internet of Things (IoT) Hardware Market Overview by Industry Sector

- Country-wise Analysis of South American Internet of Things (IoT) Hardware Market

- BRAZIL

- Brazilian Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Brazilian Internet of Things (IoT) Hardware Market Overview by Application

- Brazilian Internet of Things (IoT) Hardware Market Overview by Company Type

- Brazilian Internet of Things (IoT) Hardware Market Overview by Industry Sector

- ARGENTINA

- Argentine Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Argentine Internet of Things (IoT) Hardware Market Overview by Application

- Argentine Internet of Things (IoT) Hardware Market Overview by Company Type

- Argentine Internet of Things (IoT) Hardware Market Overview by Industry Sector

- COLOMBIA

- Colombian Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Colombian Internet of Things (IoT) Hardware Market Overview by Application

- Colombian Internet of Things (IoT) Hardware Market Overview by Company Type

- Colombian Internet of Things (IoT) Hardware Market Overview by Industry Sector

- CHILE

- Chilean Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Chilean Internet of Things (IoT) Hardware Market Overview by Application

- Chilean Internet of Things (IoT) Hardware Market Overview by Company Type

- Chilean Internet of Things (IoT) Hardware Market Overview by Industry Sector

- PERU

- Peruvian Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Peruvian Internet of Things (IoT) Hardware Market Overview by Application

- Peruvian Internet of Things (IoT) Hardware Market Overview by Company Type

- Peruvian Internet of Things (IoT) Hardware Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Rest of South America Internet of Things (IoT) Hardware Market Overview by Application

- Rest of South America Internet of Things (IoT) Hardware Market Overview by Company Type

- Rest of South America Internet of Things (IoT) Hardware Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Internet of Things (IoT) Hardware Market Overview by Geographic Region

- Middle East & Africa Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Middle East & Africa Internet of Things (IoT) Hardware Market Overview by Application

- Middle East & Africa Internet of Things (IoT) Hardware Market Overview by Company Type

- Middle East & Africa Internet of Things (IoT) Hardware Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Internet of Things (IoT) Hardware Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Internet of Things (IoT) Hardware Market Overview by Hardware Type

- United Arab Emirates Internet of Things (IoT) Hardware Market Overview by Application

- United Arab Emirates Internet of Things (IoT) Hardware Market Overview by Company Type

- United Arab Emirates Internet of Things (IoT) Hardware Market Overview by Industry Sector

- SOUTH AFRICA

- South African Internet of Things (IoT) Hardware Market Overview by Hardware Type

- South African Internet of Things (IoT) Hardware Market Overview by Application

- South African Internet of Things (IoT) Hardware Market Overview by Company Type

- South African Internet of Things (IoT) Hardware Market Overview by Industry Sector

- EGYPT

- Egyptian Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Egyptian Internet of Things (IoT) Hardware Market Overview by Application

- Egyptian Internet of Things (IoT) Hardware Market Overview by Company Type

- Egyptian Internet of Things (IoT) Hardware Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Saudi Arabian Internet of Things (IoT) Hardware Market Overview by Application

- Saudi Arabian Internet of Things (IoT) Hardware Market Overview by Company Type

- Saudi Arabian Internet of Things (IoT) Hardware Market Overview by Industry Sector

- MOROCCO

- Moroccan Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Moroccan Internet of Things (IoT) Hardware Market Overview by Application

- Moroccan Internet of Things (IoT) Hardware Market Overview by Company Type

- Moroccan Internet of Things (IoT) Hardware Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Kuwaiti Internet of Things (IoT) Hardware Market Overview by Application

- Kuwaiti Internet of Things (IoT) Hardware Market Overview by Company Type

- Kuwaiti Internet of Things (IoT) Hardware Market Overview by Industry Sector

- QATAR

- Qatari Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Qatari Internet of Things (IoT) Hardware Market Overview by Application

- Qatari Internet of Things (IoT) Hardware Market Overview by Company Type

- Qatari Internet of Things (IoT) Hardware Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Internet of Things (IoT) Hardware Market Overview by Hardware Type

- Rest of Middle East & Africa Internet of Things (IoT) Hardware Market Overview by Application

- Rest of Middle East & Africa Internet of Things (IoT) Hardware Market Overview by Company Type

- Rest of Middle East & Africa Internet of Things (IoT) Hardware Market Overview by Industry Sector

PART C: INDUSTRY GUIDE

PART D: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

ABB

Advantech

Bosch (Rexroth, Sensortec)

Cisco

Dell Technologies

Dragino

Emerson Electric

Espressif Systems

FOSSA Systems

Garmin

Honeywell

HPE

Infineon Technologies

Libelium

Lumotive

MediaTek

Microchip Technology

Murata Manufacturing

Myriota

Nordic Semiconductor

NXP Semiconductors

Panasonic

Particle.io

Qualcomm

Quectel Wireless

Schneider Electric

Seeed Studio

Semtech

Siemens

STMicroelectronics

Stratus Technologies

Telit Cinterion

Texas Instruments

u-blox

Wiliot

Zebra Technologies

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |