Global Internet of Things (IoT) Connectivity Market - Types, Applications and Industry Sectors

- Published: Aug 2025

- Pages: 488 | Charts: 409

- Report Code: ITM119

SHARE THIS REPORT:

Global Internet of Things (IoT) Connectivity Market Trends and Outlook

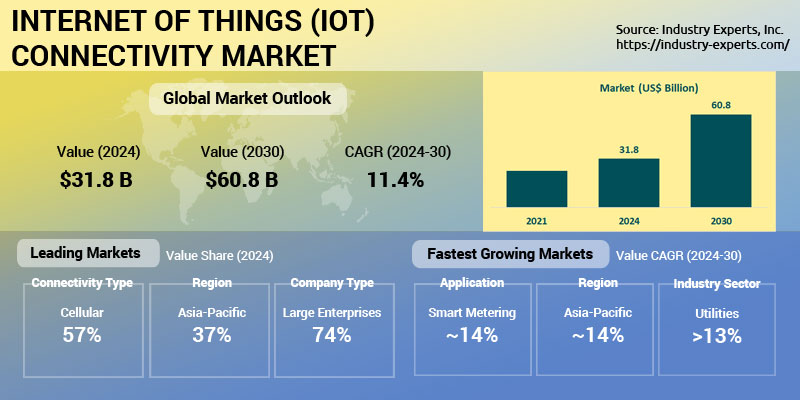

The global Internet of Things (IoT) connectivity market is entering a transformative growth phase, projected to expand from US$31.8 billion in 2024 to over US$60.8 billion by 2030, growing at a CAGR of 11.4%. This acceleration is driven by the rapid evolution from basic device connectivity toward intelligent, SLA-driven, and application-specific network solutions. IoT deployments are being increasingly influenced by AI and edge integration, demand for localized processing, eSIM/iSIM adoption, and the commercialization of new technologies such as 5G RedCap and LEO satellites. Connectivity is no longer a commodity, it's a competitive differentiator, especially as enterprises shift toward full-stack, secure, and monetizable connectivity-as-a-service (CaaS) offerings.

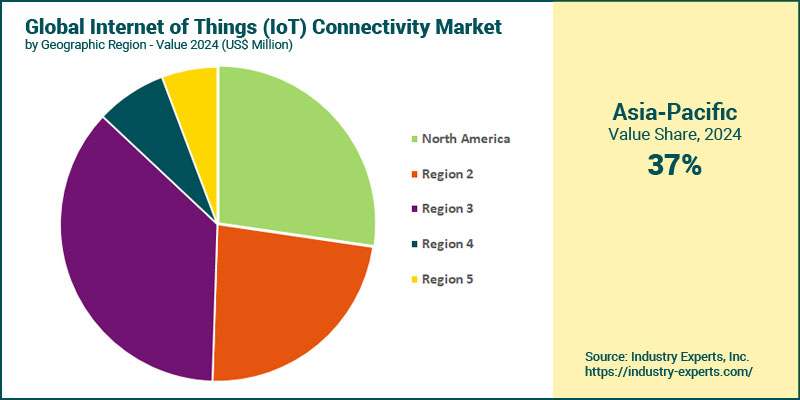

Regionally, Asia-Pacific dominates the global landscape with the largest share in 2024 (~36.5%) and is also the fastest-growing region, expected to reach US$25.3 billion by 2030 at a CAGR of 13.9%. Growth is underpinned by aggressive smart infrastructure rollouts in China and India, strong public-private partnerships, and the expansion of both LPWAN and cellular IoT ecosystems. Europe and North America follow, with Europe benefiting from green digital mandates and data sovereignty regulations, while North America leads in high-value deployments such as private 5G networks and cross-border asset tracking.

Leading players in the global IoT connectivity ecosystem include Vodafone, AT&T, China Mobile, KORE Wireless, Eseye, Telit, and EMnify, many of whom are transitioning from network providers to platform-centric orchestrators offering managed services, CaaS bundles, and vertical-specific solutions.

Internet of Things (IoT) Connectivity Regional Market Analysis

In 2024, Asia-Pacific emerged as the largest regional market, accounting for approximately 36.5% of global revenue. This leadership is driven by rapid smart infrastructure deployment, strong investments from China and India, and the widespread rollout of cellular IoT and LPWAN technologies. Asia-Pacific is also expected to remain the fastest-growing region, with a CAGR of 13.9% between 2024 and 2030. This growth is bolstered by rising adoption in energy, manufacturing, and urban mobility sectors, along with national strategies to digitize agriculture and public infrastructure. South America, while smaller in absolute terms, closely follows, driven by demand for remote asset tracking, smart agriculture, and government-led urban safety initiatives. The robust pace in emerging regions highlights the shift from traditional device-centric models toward SLA-backed, intelligent connectivity platforms tailored for regional needs.

Internet of Things (IoT) Connectivity Market Analysis by Connectivity Type

Cellular connectivity remained the dominant segment in the global IoT connectivity market, accounting for approximately 57.4% of total market value in 2024. Its widespread adoption across automotive, industrial automation, and logistics sectors continues to drive growth, particularly through 4G, LTE-M, NB-IoT, and the ongoing 5G rollout. The second-largest segment in 2024 was LPWAN (Low Power Wide Area Networks). From a growth standpoint, LPWAN is forecast to be the fastest-growing connectivity type, expanding at a 14.2% CAGR between 2024 and 2030. This growth is fueled by the global proliferation of smart utility projects, battery-efficient IoT deployments, and expansion in remote and infrastructure-poor regions.

Internet of Things (IoT) Connectivity Market Analysis by Application

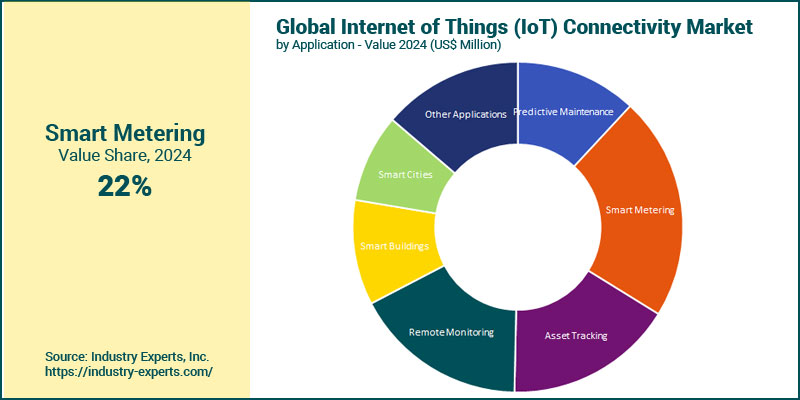

In 2024, smart metering represented the largest application segment, cornering 22% of the global market. Its leadership is driven by widespread deployment in utilities, especially in Asia-Pacific and Europe, where smart grid modernization and regulatory mandates are accelerating LPWAN-based connectivity adoption. Smart metering is also projected to be the fastest-growing segment, expanding at a 13.7% CAGR between 2024 and 2030, to reach US$15 billion. This rapid growth is attributed to ongoing utility digitization, emissions compliance initiatives, and large-scale rollout of intelligent energy infrastructure. Smart cities is the second fastest-growing application, supported by rising investments in traffic intelligence, surveillance, pollution monitoring, and urban mobility.

Internet of Things (IoT) Connectivity Market Analysis by Company Type

Large enterprises accounted for the majority share of the global IoT connectivity market in 2024, with approximately 74% of total market revenue. Their dominance stems from complex, large-scale IoT deployments in sectors such as automotive, utilities, manufacturing, and logistics, where integration with private networks, eSIMs, and multi-region orchestration is critical. Between 2024 and 2030, SMEs are projected to be the fastest-growing customer group, expanding at a 13.4% CAGR. This acceleration is driven by increasing affordability of IoT hardware, simplified onboarding through cloud-native platforms, and rising adoption in verticals such as smart retail, agriculture, and light industry.

Internet of Things (IoT) Connectivity Market Analysis by Industry Sector

In 2024, manufacturing was the largest industry sector in the global IoT connectivity market, accounting for around 27% of total market value. This leadership is driven by large-scale adoption of industrial IoT (IIoT), digital twins, predictive maintenance, and factory automation, particularly in China, Germany, and the U.S. Between 2024 and 2030, utilities are projected to be the fastest-growing sector, expanding at a 13.1% CAGR and expected to reach US$9.7 billion by 2030. This strong growth is fueled by global mandates for smart metering, grid resilience, and emissions tracking, all of which rely heavily on long-range, low-power connectivity such as LPWAN. Utilities are increasingly adopting hybrid connectivity models, combining cellular, LPWAN, and satellite solutions, to manage millions of endpoints with secure, centralized orchestration.

Internet of Things (IoT) Connectivity Market Report Scope

This global report on Internet of Things (IoT) Connectivity market analyzes the global and regional market based on Connectivity Type, Application, Company Type and Industry Sector for the period 2021-2030 with forecasts from 2024 to 2030 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Historical Period: | 2021-2024 | |

| Base Year: | 2024 | |

| Forecast Period: | 2024-2030 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 25+ |

Internet of Things (IoT) Connectivity Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Internet of Things (IoT) Connectivity Market by Connectivity Type

- Cellular

- LPWAN

- Other Connectivity Types

Internet of Things (IoT) Connectivity Market by Application

- Predictive Maintenance

- Smart Metering

- Asset Tracking

- Remote Monitoring

- Smart Buildings

- Smart Cities

- Other Applications

Internet of Things (IoT) Connectivity Market by Company Type

- Large Enterprises

- SMEs

Internet of Things (IoT) Connectivity Market by Industry Sector

- Manufacturing

- Utilities

- Transportation

- Retail

- Healthcare

- Government & Public

- Cross-industry

- Other Industry Sectors

Internet of Things (IoT) Connectivity Market Frequently Asked Questions (FAQs)

The market is estimated at US$31.8 billion in 2024, driven by increasing connected devices, smart metering mandates, and adoption of cellular and LPWAN technologies.

The market is projected to grow at a CAGR of 11.4% between 2024 and 2030, reaching US$60.8 billion by the end of the forecast period.

Asia-Pacific is the largest and fastest-growing region, expected to reach US$25.3 billion by 2030, fueled by aggressive infrastructure investment in China and India.

LPWAN (Low Power Wide Area Networks) is the fastest-growing segment, with a 14.2% CAGR, due to its scalability in utilities, agriculture, and smart cities.

Smart metering leads the market, contributing over US$7 billion in 2024, and is also the fastest-growing application segment.

SMEs are adopting plug-and-play, cloud-native IoT platforms at a rapid pace, with their market share growing at 13.4% CAGR, outpacing large enterprises.

Key trends include the rise of connectivity-as-a-service (CaaS), eSIM/iSIM, 5G RedCap, edge intelligence, LEO satellite IoT, and regulatory-driven localization of connectivity services.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Internet of Things (IoT) Connectivity

- Market Segmentation for Internet of Things (IoT) Connectivity

- Connectivity Types

- Applications

- Company Types

- Industry Sectors

- Key Trends in Internet of Things (IoT) Connectivity Market

2. INDUSTRY LANDSCAPE

- Global Internet of Things (IoT) Connectivity Market Outlook

- Comprehensive Internet of Things (IoT) Connectivity Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Internet of Things (IoT) Connectivity Industry

- Startup Strategies for Internet of Things (IoT) Connectivity Industry

- SWOT Analysis of Internet of Things (IoT) Connectivity Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Internet of Things (IoT) Connectivity Companies

- Market Share Analysis of Internet of Things (IoT) Connectivity Companies

- SWOT Analysis of Key Players in the Internet of Things (IoT) Connectivity Industry

- Key Market Players

- 1NCE

- Actility

- Aeris Communications

- Astrocast

- AT&T

- BICS

- China Mobile

- China Telecom / Unicom

- Deutsche Telekom (T-Mobile)

- EMnify

- Eseye

- Eutelsat / OneWeb

- Iridium Communications

- KORE Wireless

- Lacuna Space

- NTT (Docomo)

- Orange

- Sateliot

- Semtech (LoRa)

- Senet

- Sigfox (Unabiz)

- Soracom

- Telefonica

- Telstra

- Thales

- The Things Industries

- Truphone

- Verizon

- Vodafone

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Internet of Things (IoT) Connectivity Connectivity Type Market Overview by Global Region

- Cellular

- LPWAN

- Other Connectivity Types

- Global Internet of Things (IoT) Connectivity Market Overview by Application

- Internet of Things (IoT) Connectivity Application Market Overview by Global Region

- Predictive Maintenance

- Smart Metering

- Asset Tracking

- Remote Monitoring

- Smart Buildings

- Smart Cities

- Other Applications

- Global Internet of Things (IoT) Connectivity Market Overview by Company Type

- Internet of Things (IoT) Connectivity Company Type Market Overview by Global Region

- Large Enterprises

- SMEs

- Global Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- Internet of Things (IoT) Connectivity Industry Sector Market Overview by Global Region

- Manufacturing

- Utilities

- Transportation

- Retail

- Healthcare

- Government & Public

- Cross-industry

- Other Industry Sectors

PART B: REGIONAL MARKET PERSPECTIVE

- Global Internet of Things (IoT) Connectivity Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Internet of Things (IoT) Connectivity Market Overview by Geographic Region

- North American Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- North American Internet of Things (IoT) Connectivity Market Overview by Application

- North American Internet of Things (IoT) Connectivity Market Overview by Company Type

- North American Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- Country-wise Analysis of North American Internet of Things (IoT) Connectivity Market

- THE UNITED STATES

- United States Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- United States Internet of Things (IoT) Connectivity Market Overview by Application

- United States Internet of Things (IoT) Connectivity Market Overview by Company Type

- United States Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- CANADA

- Canadian Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Canadian Internet of Things (IoT) Connectivity Market Overview by Application

- Canadian Internet of Things (IoT) Connectivity Market Overview by Company Type

- Canadian Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- MEXICO

- Mexican Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Mexican Internet of Things (IoT) Connectivity Market Overview by Application

- Mexican Internet of Things (IoT) Connectivity Market Overview by Company Type

- Mexican Internet of Things (IoT) Connectivity Market Overview by Industry Sector

7. EUROPE

- European Internet of Things (IoT) Connectivity Market Overview by Geographic Region

- European Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- European Internet of Things (IoT) Connectivity Market Overview by Application

- European Internet of Things (IoT) Connectivity Market Overview by Company Type

- European Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- Country-wise Analysis of European Internet of Things (IoT) Connectivity Market

- GERMANY

- German Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- German Internet of Things (IoT) Connectivity Market Overview by Application

- German Internet of Things (IoT) Connectivity Market Overview by Company Type

- German Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- United Kingdom Internet of Things (IoT) Connectivity Market Overview by Application

- United Kingdom Internet of Things (IoT) Connectivity Market Overview by Company Type

- United Kingdom Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- FRANCE

- French Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- French Internet of Things (IoT) Connectivity Market Overview by Application

- French Internet of Things (IoT) Connectivity Market Overview by Company Type

- French Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- ITALY

- Italian Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Italian Internet of Things (IoT) Connectivity Market Overview by Application

- Italian Internet of Things (IoT) Connectivity Market Overview by Company Type

- Italian Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Dutch Internet of Things (IoT) Connectivity Market Overview by Application

- Dutch Internet of Things (IoT) Connectivity Market Overview by Company Type

- Dutch Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- SPAIN

- Spanish Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Spanish Internet of Things (IoT) Connectivity Market Overview by Application

- Spanish Internet of Things (IoT) Connectivity Market Overview by Company Type

- Spanish Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- RUSSIA

- Russian Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Russian Internet of Things (IoT) Connectivity Market Overview by Application

- Russian Internet of Things (IoT) Connectivity Market Overview by Company Type

- Russian Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- SWITZERLAND

- Swiss Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Swiss Internet of Things (IoT) Connectivity Market Overview by Application

- Swiss Internet of Things (IoT) Connectivity Market Overview by Company Type

- Swiss Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Rest of Europe Internet of Things (IoT) Connectivity Market Overview by Application

- Rest of Europe Internet of Things (IoT) Connectivity Market Overview by Company Type

- Rest of Europe Internet of Things (IoT) Connectivity Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Internet of Things (IoT) Connectivity Market Overview by Geographic Region

- Asia-Pacific Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Asia-Pacific Internet of Things (IoT) Connectivity Market Overview by Application

- Asia-Pacific Internet of Things (IoT) Connectivity Market Overview by Company Type

- Asia-Pacific Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Internet of Things (IoT) Connectivity Market

- CHINA

- Chinese Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Chinese Internet of Things (IoT) Connectivity Market Overview by Application

- Chinese Internet of Things (IoT) Connectivity Market Overview by Company Type

- Chinese Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- JAPAN

- Japanese Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Japanese Internet of Things (IoT) Connectivity Market Overview by Application

- Japanese Internet of Things (IoT) Connectivity Market Overview by Company Type

- Japanese Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- INDIA

- Indian Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Indian Internet of Things (IoT) Connectivity Market Overview by Application

- Indian Internet of Things (IoT) Connectivity Market Overview by Company Type

- Indian Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- AUSTRALIA

- Australia Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Australia Internet of Things (IoT) Connectivity Market Overview by Application

- Australia Internet of Things (IoT) Connectivity Market Overview by Company Type

- Australia Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- SINGAPORE

- Singaporean Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Singaporean Internet of Things (IoT) Connectivity Market Overview by Application

- Singaporean Internet of Things (IoT) Connectivity Market Overview by Company Type

- Singaporean Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- South Korean Internet of Things (IoT) Connectivity Market Overview by Application

- South Korean Internet of Things (IoT) Connectivity Market Overview by Company Type

- South Korean Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Rest of Asia-Pacific Internet of Things (IoT) Connectivity Market Overview by Application

- Rest of Asia-Pacific Internet of Things (IoT) Connectivity Market Overview by Company Type

- Rest of Asia-Pacific Internet of Things (IoT) Connectivity Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Internet of Things (IoT) Connectivity Market Overview by Geographic Region

- South American Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- South American Internet of Things (IoT) Connectivity Market Overview by Application

- South American Internet of Things (IoT) Connectivity Market Overview by Company Type

- South American Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- Country-wise Analysis of South American Internet of Things (IoT) Connectivity Market

- BRAZIL

- Brazilian Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Brazilian Internet of Things (IoT) Connectivity Market Overview by Application

- Brazilian Internet of Things (IoT) Connectivity Market Overview by Company Type

- Brazilian Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- ARGENTINA

- Argentine Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Argentine Internet of Things (IoT) Connectivity Market Overview by Application

- Argentine Internet of Things (IoT) Connectivity Market Overview by Company Type

- Argentine Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- COLOMBIA

- Colombian Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Colombian Internet of Things (IoT) Connectivity Market Overview by Application

- Colombian Internet of Things (IoT) Connectivity Market Overview by Company Type

- Colombian Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- CHILE

- Chilean Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Chilean Internet of Things (IoT) Connectivity Market Overview by Application

- Chilean Internet of Things (IoT) Connectivity Market Overview by Company Type

- Chilean Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- PERU

- Peruvian Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Peruvian Internet of Things (IoT) Connectivity Market Overview by Application

- Peruvian Internet of Things (IoT) Connectivity Market Overview by Company Type

- Peruvian Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Rest of South America Internet of Things (IoT) Connectivity Market Overview by Application

- Rest of South America Internet of Things (IoT) Connectivity Market Overview by Company Type

- Rest of South America Internet of Things (IoT) Connectivity Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Internet of Things (IoT) Connectivity Market Overview by Geographic Region

- Middle East & Africa Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Middle East & Africa Internet of Things (IoT) Connectivity Market Overview by Application

- Middle East & Africa Internet of Things (IoT) Connectivity Market Overview by Company Type

- Middle East & Africa Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Internet of Things (IoT) Connectivity Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- United Arab Emirates Internet of Things (IoT) Connectivity Market Overview by Application

- United Arab Emirates Internet of Things (IoT) Connectivity Market Overview by Company Type

- United Arab Emirates Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- SOUTH AFRICA

- South African Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- South African Internet of Things (IoT) Connectivity Market Overview by Application

- South African Internet of Things (IoT) Connectivity Market Overview by Company Type

- South African Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- EGYPT

- Egyptian Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Egyptian Internet of Things (IoT) Connectivity Market Overview by Application

- Egyptian Internet of Things (IoT) Connectivity Market Overview by Company Type

- Egyptian Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Saudi Arabian Internet of Things (IoT) Connectivity Market Overview by Application

- Saudi Arabian Internet of Things (IoT) Connectivity Market Overview by Company Type

- Saudi Arabian Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- MOROCCO

- Moroccan Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Moroccan Internet of Things (IoT) Connectivity Market Overview by Application

- Moroccan Internet of Things (IoT) Connectivity Market Overview by Company Type

- Moroccan Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Kuwaiti Internet of Things (IoT) Connectivity Market Overview by Application

- Kuwaiti Internet of Things (IoT) Connectivity Market Overview by Company Type

- Kuwaiti Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- QATAR

- Qatari Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Qatari Internet of Things (IoT) Connectivity Market Overview by Application

- Qatari Internet of Things (IoT) Connectivity Market Overview by Company Type

- Qatari Internet of Things (IoT) Connectivity Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Internet of Things (IoT) Connectivity Market Overview by Connectivity Type

- Rest of Middle East & Africa Internet of Things (IoT) Connectivity Market Overview by Application

- Rest of Middle East & Africa Internet of Things (IoT) Connectivity Market Overview by Company Type

- Rest of Middle East & Africa Internet of Things (IoT) Connectivity Market Overview by Industry Sector

PART C: INDUSTRY GUIDE

PART D: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

1NCE

Actility

Aeris Communications

Astrocast

AT&T

BICS

China Mobile

China Telecom / Unicom

Deutsche Telekom (T-Mobile)

EMnify

Eseye

Eutelsat / OneWeb

Iridium Communications

KORE Wireless

Lacuna Space

NTT (Docomo)

Orange

Sateliot

Semtech (LoRa)

Senet

Sigfox (Unabiz)

Soracom

Telefonica

Telstra

Thales

The Things Industries

Truphone

Verizon

Vodafone

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |