Global Hybrid Cloud Services Market - Service Types, Company Types, and Industry Sectors

- Published: Jul 2025

- Pages: 398 | Charts: 324

- Report Code: ITM021

SHARE THIS REPORT:

Global Hybrid Cloud Services Market Trends and Outlook

The global hybrid cloud services market is undergoing a robust expansion phase, projected to reach close to US$175 billion by 2030, at a CAGR of 13.7%. This growth is fueled by enterprises increasingly adopting hybrid cloud strategies to balance agility, control, and compliance in an evolving digital landscape. Rather than serving as a transitional model, hybrid cloud has emerged as a permanent architecture enabling seamless interoperability between on-premises systems and public cloud platforms. The shift is especially prominent among regulated sectors such as BFSI, healthcare, and government, where security, latency, and data residency requirements necessitate flexible deployment models. Enterprises are prioritizing hybrid platforms that support workload portability, containerization, and unified orchestration, paving the way for rising adoption of tools like Azure Arc, VMware Tanzu, and Red Hat OpenShift.

A primary driver of this market expansion is the enterprise need for architectural flexibility amid shifting regulatory, operational, and digital transformation demands. Hybrid cloud enables organizations to dynamically manage workloads across diverse environments, ensuring continuity during mergers, compliance shifts, or infrastructure modernization efforts. Simultaneously, the increasing complexity of data privacy and localization laws, such as GDPR, India's DPDP Act, and China's Cybersecurity Law, is compelling global businesses to retain sensitive data in-country while leveraging public cloud resources for scalability. These trends are accelerating demand for hybrid frameworks that deliver localized control without sacrificing innovation or global reach.

Hybrid Cloud Services Regional Market Analysis

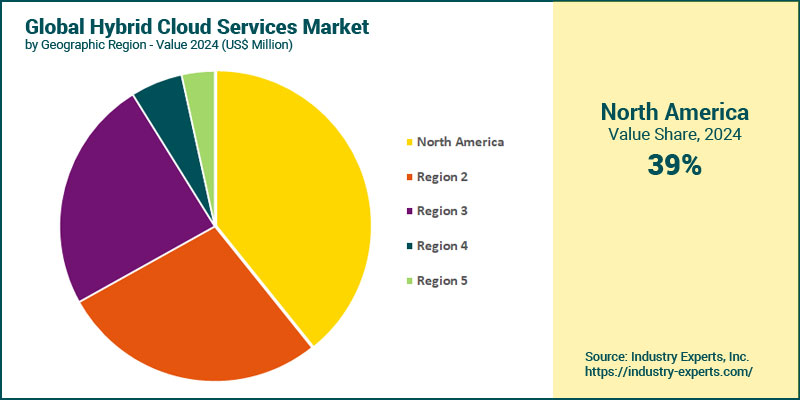

In 2024, North America was the largest regional market for hybrid cloud services, accounting for approximately 39.2% of global market value. Its leadership is underpinned by early enterprise adoption of hybrid architectures, particularly across the financial services and tech sectors, as well as widespread deployment of AI-integrated cloud platforms. Robust investments in platforms such as Azure Arc, AWS Outposts, and hybrid-ready security services continue to drive demand across both public and private sectors. Meanwhile, Asia-Pacific is expected to be the fastest-growing region through 2030, expanding at a 17.3% CAGR. Growth in this region is being fuelled by accelerated digital transformation initiatives, large-scale government modernization programs, and increasing adoption of cloud-native development among SMEs in countries like China, India, and Indonesia.

Hybrid Cloud Services Market Analysis by Service Type

As of 2024, Cloud Integration represents the largest segment in the hybrid cloud services market, accounting for approximately 44% of global market value of US$81 billion. Its dominance reflects the foundational role integration plays in unifying on-premises systems with public and private cloud environments, particularly for enterprises managing legacy IT infrastructure. Demand is further supported by the increasing adoption of APIs, microservices, and containerized architectures, all of which require robust integration capabilities across hybrid landscapes. On the other hand, Cloud Security is the fastest-growing service segment, projected to expand at a CAGR of 17% through 2030, with market value expected to more than double from 2024. This surge is driven by rising concerns over cybersecurity in hybrid environments, as enterprises grapple with distributed attack surfaces, compliance requirements, and zero-trust enforcement.

Hybrid Cloud Services Market Analysis by Company Type

Large enterprises dominated the hybrid cloud services market, contributing approximately 61.6% of global market value in 2024. Their lead is fueled by complex IT environments that demand robust hybrid strategies to integrate legacy systems, ensure regulatory compliance, and scale AI and data-intensive workloads. These organizations are investing heavily in multi-cloud orchestration, container management, and full-stack observability tools to drive efficiency and governance across distributed infrastructures. In contrast, small and medium-sized enterprises (SMEs) are poised to be the fastest-growing segment, expanding at a 15.2% CAGR between 2024 and 2030. This rapid growth is underpinned by the rising availability of modular, cost-effective, and pre-packaged hybrid solutions tailored to SMEs' needs. Simplified onboarding, managed services, and turnkey deployments are enabling smaller firms, especially in sectors like retail, healthcare, and logistics, to embrace hybrid architectures without requiring extensive internal IT capabilities. A key trend across both segments is the rising demand for industry-specific hybrid stacks that deliver business outcomes rather than just infrastructure integration.

Hybrid Cloud Services Market Analysis by Industry Sector

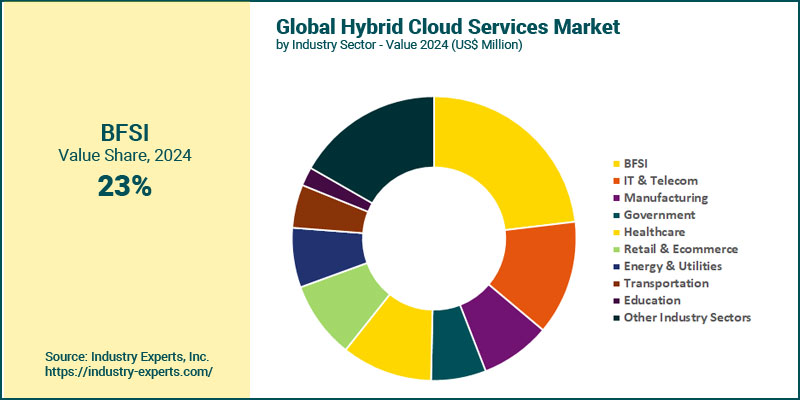

In 2024, the Banking, Financial Services, and Insurance (BFSI) sector represented the largest vertical in the hybrid cloud services market, contributing approximately 23.1% of global value (US$18.7 billion out of US$81.0 billion). This dominance is driven by the industry's ongoing need for secure, compliant, and scalable infrastructure capable of supporting core banking applications, fraud analytics, and AI-driven customer engagement-all while meeting strict regulatory demands. Financial institutions are also leading adopters of sovereign hybrid architectures, leveraging hybrid models to balance local data residency with global processing scalability. Meanwhile, the IT & Telecom vertical is projected to be the fastest-growing segment, expanding at a 16.6% CAGR from 2024 to 2030 and reaching US$26.6 billion by 2030. This rapid growth is attributed to the sector's central role in delivering digital infrastructure, cloud-native platforms, and 5G services. Telecom providers are adopting hybrid cloud to support edge computing, AI-powered network operations, and multi-cloud orchestration for enterprise clients. A key emerging trend across verticals is the integration of hybrid cloud services with AI workloads-particularly in healthcare, manufacturing, and government sectors-enabling localized data processing, predictive analytics, and real-time operational intelligence while maintaining compliance with industry-specific regulations.

Hybrid Cloud Services Market Report Scope

This global report on Hybrid Cloud Services analyzes the global and regional market based on Service Type, Company Type, and Industry Sector for the period 2021-2030 with projection from 2024 to 2030 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Historical Period: | 2021-2024 | |

| Base Year: | 2024 | |

| Forecast Period: | 2024-2030 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 25+ |

Hybrid Cloud Services Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Hybrid Cloud Services Market by Service Type

- Cloud Integration

- Cloud Management

- Consulting

- Cloud Security

- Networking

Hybrid Cloud Services Market by Company Type

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

Hybrid Cloud Services Market by Industry Sector

- BFSI

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

Hybrid Cloud Services Market Frequently Asked Questions (FAQs)

The global Hybrid Cloud Services market is projected to grow at a 13.7% CAGR, reaching approximately US$175 billion by 2030.

North America led the global Hybrid Cloud Services market with a 39.2% share, followed by Europe and Asia-Pacific.

Asia-Pacific is expected to be the fastest-growing region through 2030, expanding at a 17.3% CAGR. Growth in this region is being fueled by accelerated digital transformation initiatives, large-scale government modernization programs, etc.

Cloud Integration represents the largest segment in the hybrid cloud services market, accounting for approximately 44% of global market value.

IT & Telecom vertical is projected to be the fastest-growing segment, expanding at a 16.6% CAGR from 2024 to 2030, attributed to the sector's central role in delivering digital infrastructure.

In 2024, large enterprises dominated the hybrid cloud services market, contributing approximately 61.6% of global market value of US$81 billion.

The hybrid cloud services market is led by Amazon Web Services (AWS), Microsoft Azure, Google Cloud Platform (GCP), and IBM, which together account for the majority of global market share. Other notable players include Oracle, Hewlett Packard Enterprise (HPE), VMware (now under Broadcom), Cisco, and Dell Technologies, who serve as strong followers.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Hybrid Cloud Services

- Market Segmentation for Hybrid Cloud Services

- Service Types

- Company Types based on size

- Industry Sectors

- Key Trends in Hybrid Cloud Services Market

2. INDUSTRY LANDSCAPE

- Global Hybrid Cloud Services Market Outlook

- Comprehensive Hybrid Cloud Services Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Hybrid Cloud Services Industry

- SWOT Analysis of Hybrid Cloud Services Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Hybrid Cloud Services Companies

- Market Share Analysis of Hybrid Cloud Services Companies

- Key Market Players

- Alibaba

- Atos

- Amazon Web Services (AWS)

- Broadcom (VMware)

- CenturyLink

- Cisco Systems

- Citrix

- Dell EMC

- DXC Technology Company

- Equinix

- Fujitsu

- Hewlett Packard Enterprise (HPE)

- Huawei

- IBM

- Micro Focus

- Microsoft

- NetApp

- NTT Communications

- Oracle

- Pure Storage

- Quest Software

- Rackspace

- RightScale

- T-Systems

- Unitas Global

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Hybrid Cloud Services Market Overview by Service Type

- Hybrid Cloud Services Service Type Market Overview by Global Region

- Cloud Integration

- Cloud Management

- Consulting

- Cloud Security

- Networking

- Global Hybrid Cloud Services Market Overview by Company Type

- Hybrid Cloud Services Company Type Market Overview by Global Region

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

- Global Hybrid Cloud Services Market Overview by Industry Sector

- Hybrid Cloud Services Industry Sector Market Overview by Global Region

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

PART B: REGIONAL MARKET PERSPECTIVE

- Global Hybrid Cloud Services Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Hybrid Cloud Services Market Overview by Geographic Region

- North American Hybrid Cloud Services Market Overview by Service Type

- North American Hybrid Cloud Services Market Overview by Company Type

- North American Hybrid Cloud Services Market Overview by Industry Sector

- Country-wise Analysis of North American Hybrid Cloud Services Market

- THE UNITED STATES

- United States Hybrid Cloud Services Market Overview by Service Type

- United States Hybrid Cloud Services Market Overview by Company Type

- United States Hybrid Cloud Services Market Overview by Industry Sector

- CANADA

- Canadian Hybrid Cloud Services Market Overview by Service Type

- Canadian Hybrid Cloud Services Market Overview by Company Type

- Canadian Hybrid Cloud Services Market Overview by Industry Sector

- MEXICO

- Mexican Hybrid Cloud Services Market Overview by Service Type

- Mexican Hybrid Cloud Services Market Overview by Company Type

- Mexican Hybrid Cloud Services Market Overview by Industry Sector

7. EUROPE

- European Hybrid Cloud Services Market Overview by Geographic Region

- European Hybrid Cloud Services Market Overview by Service Type

- European Hybrid Cloud Services Market Overview by Company Type

- European Hybrid Cloud Services Market Overview by Industry Sector

- Country-wise Analysis of European Hybrid Cloud Services Market

- GERMANY

- German Hybrid Cloud Services Market Overview by Service Type

- German Hybrid Cloud Services Market Overview by Company Type

- German Hybrid Cloud Services Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Hybrid Cloud Services Market Overview by Service Type

- United Kingdom Hybrid Cloud Services Market Overview by Company Type

- United Kingdom Hybrid Cloud Services Market Overview by Industry Sector

- FRANCE

- French Hybrid Cloud Services Market Overview by Service Type

- French Hybrid Cloud Services Market Overview by Company Type

- French Hybrid Cloud Services Market Overview by Industry Sector

- ITALY

- Italian Hybrid Cloud Services Market Overview by Service Type

- Italian Hybrid Cloud Services Market Overview by Company Type

- Italian Hybrid Cloud Services Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Hybrid Cloud Services Market Overview by Service Type

- Dutch Hybrid Cloud Services Market Overview by Company Type

- Dutch Hybrid Cloud Services Market Overview by Industry Sector

- SPAIN

- Spanish Hybrid Cloud Services Market Overview by Service Type

- Spanish Hybrid Cloud Services Market Overview by Company Type

- Spanish Hybrid Cloud Services Market Overview by Industry Sector

- RUSSIA

- Russian Hybrid Cloud Services Market Overview by Service Type

- Russian Hybrid Cloud Services Market Overview by Company Type

- Russian Hybrid Cloud Services Market Overview by Industry Sector

- SWITZERLAND

- Swiss Hybrid Cloud Services Market Overview by Service Type

- Swiss Hybrid Cloud Services Market Overview by Company Type

- Swiss Hybrid Cloud Services Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Hybrid Cloud Services Market Overview by Service Type

- Rest of Europe Hybrid Cloud Services Market Overview by Company Type

- Rest of Europe Hybrid Cloud Services Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Hybrid Cloud Services Market Overview by Geographic Region

- Asia-Pacific Hybrid Cloud Services Market Overview by Service Type

- Asia-Pacific Hybrid Cloud Services Market Overview by Company Type

- Asia-Pacific Hybrid Cloud Services Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Hybrid Cloud Services Market

- CHINA

- Chinese Hybrid Cloud Services Market Overview by Service Type

- Chinese Hybrid Cloud Services Market Overview by Company Type

- Chinese Hybrid Cloud Services Market Overview by Industry Sector

- JAPAN

- Japanese Hybrid Cloud Services Market Overview by Service Type

- Japanese Hybrid Cloud Services Market Overview by Company Type

- Japanese Hybrid Cloud Services Market Overview by Industry Sector

- INDIA

- Indian Hybrid Cloud Services Market Overview by Service Type

- Indian Hybrid Cloud Services Market Overview by Company Type

- Indian Hybrid Cloud Services Market Overview by Industry Sector

- AUSTRALIA

- Australia Hybrid Cloud Services Market Overview by Service Type

- Australia Hybrid Cloud Services Market Overview by Company Type

- Australia Hybrid Cloud Services Market Overview by Industry Sector

- SINGAPORE

- Singaporean Hybrid Cloud Services Market Overview by Service Type

- Singaporean Hybrid Cloud Services Market Overview by Company Type

- Singaporean Hybrid Cloud Services Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Hybrid Cloud Services Market Overview by Service Type

- South Korean Hybrid Cloud Services Market Overview by Company Type

- South Korean Hybrid Cloud Services Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Hybrid Cloud Services Market Overview by Service Type

- Rest of Asia-Pacific Hybrid Cloud Services Market Overview by Company Type

- Rest of Asia-Pacific Hybrid Cloud Services Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Hybrid Cloud Services Market Overview by Geographic Region

- South American Hybrid Cloud Services Market Overview by Service Type

- South American Hybrid Cloud Services Market Overview by Company Type

- South American Hybrid Cloud Services Market Overview by Industry Sector

- Country-wise Analysis of South American Hybrid Cloud Services Market

- BRAZIL

- Brazilian Hybrid Cloud Services Market Overview by Service Type

- Brazilian Hybrid Cloud Services Market Overview by Company Type

- Brazilian Hybrid Cloud Services Market Overview by Industry Sector

- ARGENTINA

- Argentine Hybrid Cloud Services Market Overview by Service Type

- Argentine Hybrid Cloud Services Market Overview by Company Type

- Argentine Hybrid Cloud Services Market Overview by Industry Sector

- COLOMBIA

- Colombian Hybrid Cloud Services Market Overview by Service Type

- Colombian Hybrid Cloud Services Market Overview by Company Type

- Colombian Hybrid Cloud Services Market Overview by Industry Sector

- CHILE

- Chilean Hybrid Cloud Services Market Overview by Service Type

- Chilean Hybrid Cloud Services Market Overview by Company Type

- Chilean Hybrid Cloud Services Market Overview by Industry Sector

- PERU

- Peruvian Hybrid Cloud Services Market Overview by Service Type

- Peruvian Hybrid Cloud Services Market Overview by Company Type

- Peruvian Hybrid Cloud Services Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Hybrid Cloud Services Market Overview by Service Type

- Rest of South America Hybrid Cloud Services Market Overview by Company Type

- Rest of South America Hybrid Cloud Services Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Hybrid Cloud Services Market Overview by Geographic Region

- Middle East & Africa Hybrid Cloud Services Market Overview by Service Type

- Middle East & Africa Hybrid Cloud Services Market Overview by Company Type

- Middle East & Africa Hybrid Cloud Services Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Hybrid Cloud Services Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Hybrid Cloud Services Market Overview by Service Type

- United Arab Emirates Hybrid Cloud Services Market Overview by Company Type

- United Arab Emirates Hybrid Cloud Services Market Overview by Industry Sector

- SOUTH AFRICA

- South African Hybrid Cloud Services Market Overview by Service Type

- South African Hybrid Cloud Services Market Overview by Company Type

- South African Hybrid Cloud Services Market Overview by Industry Sector

- EGYPT

- Egyptian Hybrid Cloud Services Market Overview by Service Type

- Egyptian Hybrid Cloud Services Market Overview by Company Type

- Egyptian Hybrid Cloud Services Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Hybrid Cloud Services Market Overview by Service Type

- Saudi Arabian Hybrid Cloud Services Market Overview by Company Type

- Saudi Arabian Hybrid Cloud Services Market Overview by Industry Sector

- MOROCCO

- Moroccan Hybrid Cloud Services Market Overview by Service Type

- Moroccan Hybrid Cloud Services Market Overview by Company Type

- Moroccan Hybrid Cloud Services Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Hybrid Cloud Services Market Overview by Service Type

- Kuwaiti Hybrid Cloud Services Market Overview by Company Type

- Kuwaiti Hybrid Cloud Services Market Overview by Industry Sector

- QATAR

- Qatari Hybrid Cloud Services Market Overview by Service Type

- Qatari Hybrid Cloud Services Market Overview by Company Type

- Qatari Hybrid Cloud Services Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Hybrid Cloud Services Market Overview by Service Type

- Rest of Middle East & Africa Hybrid Cloud Services Market Overview by Company Type

- Rest of Middle East & Africa Hybrid Cloud Services Market Overview by Industry Sector

PART C: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

Alibaba

Atos

Amazon Web Services (AWS)

Broadcom (VMware)

CenturyLink

Cisco Systems

Citrix

Dell EMC

DXC Technology Company

Equinix

Fujitsu

Google

Hewlett Packard Enterprise (HPE)

Huawei

IBM

Micro Focus

Microsoft

NetApp

NTT Communications

Oracle

Pure Storage

Quest Software

Rackspace

RightScale

T-Systems

Unitas Global

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |