Global Generative AI Market - Technologies, Models, Applications and Industry Sectors

- Published: Aug 2025

- Pages: 590 | Charts: 496

- Report Code: ITM137

SHARE THIS REPORT:

Global Generative AI Market Trends and Outlook

The global Generative AI market is undergoing a rapid transformation, evolving from a research-centric novelty into a foundational pillar of enterprise digital strategy. Valued at approximately US$18.5 billion in 2024, the market is projected to exceed US$445 billion by 2034, growing at a CAGR of 37.4%. This explosive growth is fueled by surging enterprise demand across sectors such as finance, healthcare, media, and retail, where generative models are increasingly embedded into business-critical workflows. The pace of adoption has accelerated due to a confluence of factors, maturing foundation models, democratization of APIs, availability of fine-tuning tools, and aggressive investment from cloud hyperscalers and startups alike.

A fundamental enabler of this expansion is the convergence of hardware and software innovation. GPU clusters, AI accelerators, and next-generation cloud infrastructure are reducing training times and scaling performance, while breakthroughs in model compression - like quantization, LoRA, and pruning - are enabling real-time inference even on edge and mobile devices. In parallel, the competitive dynamics are shifting rapidly with the rise of open-weight models such as LLaMA and Mixtral, which are empowering enterprises to develop proprietary solutions without ceding control over data privacy or compliance. This democratization is intensifying innovation cycles and broadening accessibility to a wider range of industries and company sizes.

Generative AI Regional Market Analysis

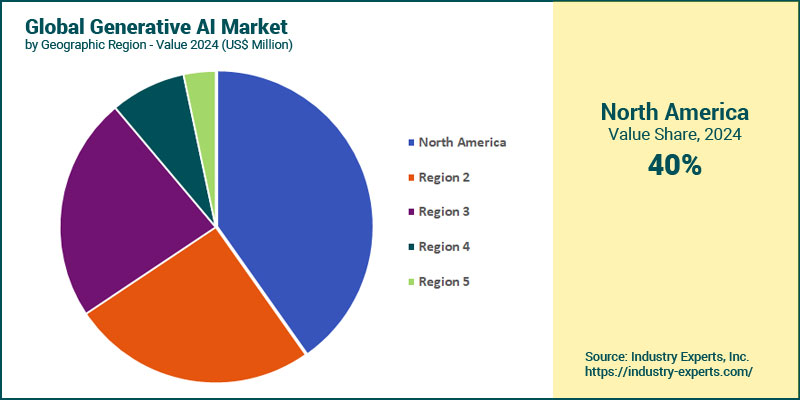

In 2024, North America is the largest regional market, accounting for a 40.2% share of global Generative AI revenue. This dominance stems from aggressive investments by hyperscalers like Microsoft, Amazon, and Google, coupled with a mature AI startup ecosystem and early enterprise adoption across sectors. Europe ranks second, with US$4.7 billion, backed by regulatory clarity under the EU AI Act and strong public-private collaboration. Asia-Pacific is the fastest-growing region, poised to reach US$197 billion by 2034, registering a CAGR of 46.6% between 2024 and 2034. Growth is fueled by strategic government backing - especially in China's LLM race - and enterprise demand in Japan, India, and South Korea for generative AI in manufacturing, media, and customer engagement. South America also shows strong momentum with a 40.5% CAGR, driven by adoption in digital banking, telecom, and education sectors. While North America will retain leadership in absolute value, Asia-Pacific's scale and pace of adoption make it the primary engine of global market expansion over the next decade.

Generative AI Market Analysis by Component

In 2024, software is the dominant segment, accounting for 62.4% of the total market. This early lead reflects enterprise spending on foundational model APIs, developer platforms, and vertical-specific applications. Vendors like OpenAI, Anthropic, and Cohere continue to gain traction through commercial licensing, prompting strong adoption in financial services, media, and retail sectors. However, services will become the primary growth engine, expanding at a CAGR of 41.1% between 2024 and 2034. This surge is fueled by growing enterprise demand for consulting, fine-tuning, integration, prompt engineering, risk audits, and compliance enablement. The shift reflects a broader maturity trend, as organizations increasingly seek outcome-based implementations and managed services to scale generative AI across business functions. While software will remain substantial, services are expected to narrow the gap, positioning services-led models as the backbone of enterprise generative AI transformation.

Generative AI Market Analysis by Technology

As of 2024, Transformers are the largest technology segment, generating approximately 43.8% of the global Generative AI market. Their dominance is anchored in widespread use across LLMs and APIs from providers like OpenAI, Google, and Anthropic. Generative Adversarial Networks (GANs) follow closely with a US$5.3 billion market, especially prevalent in synthetic media, image generation, and digital content creation. Looking ahead, Diffusion Networks are expected to be the fastest-growing segment, expanding at a CAGR of 41% between 2024 and 2034. Adoption is accelerating due to their superior performance in generating high-resolution, photorealistic images and video, a key driver for applications in creative design, entertainment, and marketing automation. Advances by players like Stability AI and Open-source communities have also accelerated enterprise experimentation. By 2034, Transformers will still lead in absolute terms, followed by GANs. However, the rapid rise of Diffusion and hybrid models suggests a more diversified future, with enterprises adopting combinations of architectures based on use case requirements, performance goals, and regulatory needs.

Generative AI Market Analysis by Model

Large Language Models (LLMs) account for the largest share of the market, generating approximately 41.2% of global revenue in 2024. Their lead is driven by widespread enterprise deployment for tasks like content generation, summarization, customer support automation, and knowledge retrieval. Vendors such as OpenAI, Anthropic, and Google continue to dominate this space. Multi-modal generative models are projected to be the fastest-growing segment, expanding at a CAGR of 41.1% to reach nearly US$119.2 billion by 2034. This surge is fueled by growing enterprise and consumer demand for AI systems that can process and generate across multiple modalities - text, image, video, and audio - enabling rich applications in design, e-commerce, healthcare, and media. The rise of multimodal LLMs like GPT-4o and Gemini is accelerating this trend.

Generative AI Market Analysis by Application

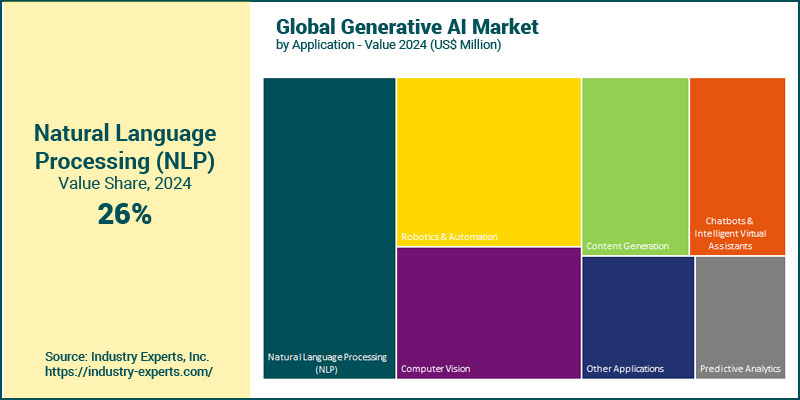

In 2024, Natural Language Processing (NLP) is the largest application segment, generating approximately US$4.7 billion, or 25.5% of the global market. This leadership is fueled by widespread enterprise use in summarization, question-answering, document parsing, and customer service automation. Adoption is especially strong in finance, legal, and healthcare, where structured-to-unstructured data processing is mission-critical. Computer Vision emerges as the fastest-growing segment, projected to expand at a CAGR of 42.9%. Growth is driven by explosive demand in automated video analytics, digital twins, generative design, and augmented reality. From industrial inspections to creative media and smart retail, vision-based generative AI is becoming integral to high-value applications across industries.

Generative AI Market Analysis by Industry Sector

Media & Entertainment is the largest end-use industry, contributing around 32.2% of the global Generative AI market in 2024. Adoption is being driven by demand for AI-powered content creation, animation, text-to-video synthesis, and personalization at scale, especially in streaming, gaming, and digital marketing. The sector continues to benefit from early experimentation and high creative demand. However, Banking, Financial Services, and Insurance (BFSI) is expected to be the fastest-growing vertical, registering a CAGR of 43.7% between 2024 and 2034 to reach US$99 billion. This momentum is being fueled by the integration of Generative AI into document processing, fraud detection, customer onboarding, synthetic data generation, and personalized advisory services. Strong ROI use cases and regulatory readiness are accelerating enterprise-scale deployments.

Generative AI Market Report Scope

This global report on Generative AI market analyzes the global and regional market based on Component, Technology, Model, Application, and Industry Sector for the period 2024-2034 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Base Year: | 2024 | |

| Forecast Period: | 2024-2034 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 40+ |

Generative AI Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Generative AI Market by Component

- Software

- Services

Generative AI Market by Technology

- Transformers

- Generative Adversarial Networks (GANs)

- Variational Auto-encoders

- Diffusion Networks

Generative AI Market by Model

- Large Language Models

- Image & Video Generative Models

- Multi-modal Generative Models

- Other Models

Generative AI Market by Application

- Natural Language Processing (NLP)

- Robotics & Automation

- Computer Vision

- Content Generation

- Chatbots & Intelligent Virtual Assistants

- Predictive Analytics

- Other Applications

Generative AI Market by Industry Sector

- Media & Entertainment

- Automotive & Transportation

- Banking, Financial Services, and Insurance (BFSI)

- Healthcare

- IT & Telecom

- Education

- Other Sectors

Generative AI Market Frequently Asked Questions (FAQs)

The global Generative AI market is valued at approximately US$18.5 billion in 2024 and is expected to surpass US$445 billion by 2034, growing at a CAGR of 37.4% over the forecast period. This growth is driven by rapid enterprise adoption across sectors including finance, healthcare, retail, and media.

The strongest adoption is seen in media & entertainment, BFSI (banking, financial services, and insurance), and healthcare. These sectors use generative AI for content creation, document processing, customer service, diagnostics, and risk modeling. BFSI is the fastest-growing vertical, with a CAGR of 43.7% through 2034.

Major technologies include Transformers, Diffusion Networks, Generative Adversarial Networks (GANs), and Variational Autoencoders. While Transformers dominate in value due to their role in large language models, Diffusion Networks are the fastest-growing, driven by their capabilities in image and video synthesis.

Leading players include OpenAI, Google DeepMind, Anthropic, Microsoft, Amazon Web Services, Meta AI, NVIDIA, and Stability AI. The market is also being reshaped by emerging open-source players and enterprise-focused startups offering fine-tuned or domain-specific generative solutions.

Key trends include the rise of multimodal models, open-weight alternatives, cloud-native generative services, GPU and accelerator advancements, and increasing focus on model explainability and regulatory compliance. Enterprises are shifting toward integrated solutions that align with business goals, not just general-purpose generation.

The market faces hurdles around regulatory fragmentation, IP rights, data privacy, algorithmic bias, and talent shortages. Compliance with frameworks like the EU AI Act and China's AI guidelines adds complexity, particularly for mid-sized firms without mature governance capabilities.

As of 2024, Software is the largest component segment, generating over US$11.5 billion, or around 62% of total market revenue. This includes foundation model APIs, development platforms, and custom applications adopted across industries. However, Services are catching up fast and expected to surpass software in the longer term due to rising demand for integration, fine-tuning, and compliance support.

Diffusion Networks are the fastest-growing technology, expanding at a CAGR of 41% through 2034. Their ability to generate high-resolution, photorealistic content is driving demand in sectors like media, advertising, design, and digital twins. This makes them especially attractive for companies seeking creative automation at scale.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Generative AI

- Market Segmentation for Generative AI

- Components

- Technologies

- Models

- Applications

- Industry Sectors

- Key Trends in Generative AI Market

2. INDUSTRY LANDSCAPE

- Global Generative AI Market Outlook

- Comprehensive Generative AI Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Generative AI Industry

- Startup Strategies for Generative AI Industry

- SWOT Analysis of Generative AI Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Generative AI Companies

- Market Share Analysis of Generative AI Companies

- SWOT Analysis of Key Players in the Generative AI Industry

- Key Market Players

- Adobe

- Amazon Web Services, Inc.

- Anthropic

- Atos SE

- AWS

- Baidu Inc.

- Capgemini SE

- Databricks

- DeepMind Technologies Limited

- De-Identification Ltd

- D-ID

- Fujitsu Limited

- Genie AI Ltd.

- Google LLC

- Graphcore Ltd.

- Hugging Face Inc.

- IBM

- Infosys Ltd.

- Jasper

- Microsoft Corporation

- Midjourney

- Mistral AI

- MOSTLY AI Inc.

- NTT Data Corporation

- NVIDIA

- OpenAI

- Oracle

- Rephrase.ai

- SAP SE

- Scale AI

- SenseTime Group Ltd.

- Stability AI

- Synthesia

- Synthesia Limited

- Tata Consultancy Services Ltd.

- Tencent Holdings Ltd.

- TietoEVRY Corporation

- Together AI

- xAI

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Generative AI Market Overview by Component

- Generative AI Component Market Overview by Global Region

- Software

- Services

- Global Generative AI Market Overview by Technology

- Generative AI Technology Market Overview by Global Region

- Transformers

- Generative Adversarial Networks (GANs)

- Variational Auto-encoders

- Diffusion Networks

- Global Generative AI Market Overview by Model

- Generative AI Model Market Overview by Global Region

- Large Language Models

- Image & Video Generative Models

- Multi-modal Generative Models

- Other Models

- Global Generative AI Market Overview by Application

- Generative AI Application Market Overview by Global Region

- Natural Language Processing (NLP)

- Robotics & Automation

- Computer Vision

- Content Generation

- Chatbots & Intelligent Virtual Assistants

- Predictive Analytics

- Other Applications

- Global Generative AI Market Overview by Industry Sector

- Generative AI Industry Sector Market Overview by Global Region

- Media & Entertainment

- Automotive & Transportation

- Banking, Financial Services, and Insurance (BFSI)

- Healthcare

- IT & Telecom

- Education

- Other Industry Sectors

PART B: REGIONAL MARKET PERSPECTIVE

- Global Generative AI Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Generative AI Market Overview by Geographic Region

- North American Generative AI Market Overview by Component

- North American Generative AI Market Overview by Technology

- North American Generative AI Market Overview by Model

- North American Generative AI Market Overview by Application

- North American Generative AI Market Overview by Industry Sector

- Country-wise Analysis of North American Generative AI Market

- THE UNITED STATES

- United States Generative AI Market Overview by Component

- United States Generative AI Market Overview by Technology

- United States Generative AI Market Overview by Model

- United States Generative AI Market Overview by Application

- United States Generative AI Market Overview by Industry Sector

- CANADA

- Canadian Generative AI Market Overview by Component

- Canadian Generative AI Market Overview by Technology

- Canadian Generative AI Market Overview by Model

- Canadian Generative AI Market Overview by Application

- Canadian Generative AI Market Overview by Industry Sector

- MEXICO

- Mexican Generative AI Market Overview by Component

- Mexican Generative AI Market Overview by Technology

- Mexican Generative AI Market Overview by Model

- Mexican Generative AI Market Overview by Application

- Mexican Generative AI Market Overview by Industry Sector

7. EUROPE

- European Generative AI Market Overview by Geographic Region

- European Generative AI Market Overview by Component

- European Generative AI Market Overview by Technology

- European Generative AI Market Overview by Model

- European Generative AI Market Overview by Application

- European Generative AI Market Overview by Industry Sector

- Country-wise Analysis of European Generative AI Market

- GERMANY

- German Generative AI Market Overview by Component

- German Generative AI Market Overview by Technology

- German Generative AI Market Overview by Model

- German Generative AI Market Overview by Application

- German Generative AI Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Generative AI Market Overview by Component

- United Kingdom Generative AI Market Overview by Technology

- United Kingdom Generative AI Market Overview by Model

- United Kingdom Generative AI Market Overview by Application

- United Kingdom Generative AI Market Overview by Industry Sector

- FRANCE

- French Generative AI Market Overview by Component

- French Generative AI Market Overview by Technology

- French Generative AI Market Overview by Model

- French Generative AI Market Overview by Application

- French Generative AI Market Overview by Industry Sector

- ITALY

- Italian Generative AI Market Overview by Component

- Italian Generative AI Market Overview by Technology

- Italian Generative AI Market Overview by Model

- Italian Generative AI Market Overview by Application

- Italian Generative AI Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Generative AI Market Overview by Component

- Dutch Generative AI Market Overview by Technology

- Dutch Generative AI Market Overview by Model

- Dutch Generative AI Market Overview by Application

- Dutch Generative AI Market Overview by Industry Sector

- SPAIN

- Spanish Generative AI Market Overview by Component

- Spanish Generative AI Market Overview by Technology

- Spanish Generative AI Market Overview by Model

- Spanish Generative AI Market Overview by Application

- Spanish Generative AI Market Overview by Industry Sector

- RUSSIA

- Russian Generative AI Market Overview by Component

- Russian Generative AI Market Overview by Technology

- Russian Generative AI Market Overview by Model

- Russian Generative AI Market Overview by Application

- Russian Generative AI Market Overview by Industry Sector

- SWITZERLAND

- Swiss Generative AI Market Overview by Component

- Swiss Generative AI Market Overview by Technology

- Swiss Generative AI Market Overview by Model

- Swiss Generative AI Market Overview by Application

- Swiss Generative AI Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Generative AI Market Overview by Component

- Rest of Europe Generative AI Market Overview by Technology

- Rest of Europe Generative AI Market Overview by Model

- Rest of Europe Generative AI Market Overview by Application

- Rest of Europe Generative AI Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Generative AI Market Overview by Geographic Region

- Asia-Pacific Generative AI Market Overview by Component

- Asia-Pacific Generative AI Market Overview by Technology

- Asia-Pacific Generative AI Market Overview by Model

- Asia-Pacific Generative AI Market Overview by Application

- Asia-Pacific Generative AI Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Generative AI Market

- CHINA

- Chinese Generative AI Market Overview by Component

- Chinese Generative AI Market Overview by Technology

- Chinese Generative AI Market Overview by Model

- Chinese Generative AI Market Overview by Application

- Chinese Generative AI Market Overview by Industry Sector

- JAPAN

- Japanese Generative AI Market Overview by Component

- Japanese Generative AI Market Overview by Technology

- Japanese Generative AI Market Overview by Model

- Japanese Generative AI Market Overview by Application

- Japanese Generative AI Market Overview by Industry Sector

- INDIA

- Indian Generative AI Market Overview by Component

- Indian Generative AI Market Overview by Technology

- Indian Generative AI Market Overview by Model

- Indian Generative AI Market Overview by Application

- Indian Generative AI Market Overview by Industry Sector

- AUSTRALIA

- Australia Generative AI Market Overview by Component

- Australia Generative AI Market Overview by Technology

- Australia Generative AI Market Overview by Model

- Australia Generative AI Market Overview by Application

- Australia Generative AI Market Overview by Industry Sector

- SINGAPORE

- Singaporean Generative AI Market Overview by Component

- Singaporean Generative AI Market Overview by Technology

- Singaporean Generative AI Market Overview by Model

- Singaporean Generative AI Market Overview by Application

- Singaporean Generative AI Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Generative AI Market Overview by Component

- South Korean Generative AI Market Overview by Technology

- South Korean Generative AI Market Overview by Model

- South Korean Generative AI Market Overview by Application

- South Korean Generative AI Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Generative AI Market Overview by Component

- Rest of Asia-Pacific Generative AI Market Overview by Technology

- Rest of Asia-Pacific Generative AI Market Overview by Model

- Rest of Asia-Pacific Generative AI Market Overview by Application

- Rest of Asia-Pacific Generative AI Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Generative AI Market Overview by Geographic Region

- South American Generative AI Market Overview by Component

- South American Generative AI Market Overview by Technology

- South American Generative AI Market Overview by Model

- South American Generative AI Market Overview by Application

- South American Generative AI Market Overview by Industry Sector

- Country-wise Analysis of South American Generative AI Market

- BRAZIL

- Brazilian Generative AI Market Overview by Component

- Brazilian Generative AI Market Overview by Technology

- Brazilian Generative AI Market Overview by Model

- Brazilian Generative AI Market Overview by Application

- Brazilian Generative AI Market Overview by Industry Sector

- ARGENTINA

- Argentine Generative AI Market Overview by Component

- Argentine Generative AI Market Overview by Technology

- Argentine Generative AI Market Overview by Model

- Argentine Generative AI Market Overview by Application

- Argentine Generative AI Market Overview by Industry Sector

- COLOMBIA

- Colombian Generative AI Market Overview by Component

- Colombian Generative AI Market Overview by Technology

- Colombian Generative AI Market Overview by Model

- Colombian Generative AI Market Overview by Application

- Colombian Generative AI Market Overview by Industry Sector

- CHILE

- Chilean Generative AI Market Overview by Component

- Chilean Generative AI Market Overview by Technology

- Chilean Generative AI Market Overview by Model

- Chilean Generative AI Market Overview by Application

- Chilean Generative AI Market Overview by Industry Sector

- PERU

- Peruvian Generative AI Market Overview by Component

- Peruvian Generative AI Market Overview by Technology

- Peruvian Generative AI Market Overview by Model

- Peruvian Generative AI Market Overview by Application

- Peruvian Generative AI Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Generative AI Market Overview by Component

- Rest of South America Generative AI Market Overview by Technology

- Rest of South America Generative AI Market Overview by Model

- Rest of South America Generative AI Market Overview by Application

- Rest of South America Generative AI Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Generative AI Market Overview by Geographic Region

- Middle East & Africa Generative AI Market Overview by Component

- Middle East & Africa Generative AI Market Overview by Technology

- Middle East & Africa Generative AI Market Overview by Model

- Middle East & Africa Generative AI Market Overview by Application

- Middle East & Africa Generative AI Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Generative AI Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Generative AI Market Overview by Component

- United Arab Emirates Generative AI Market Overview by Technology

- United Arab Emirates Generative AI Market Overview by Model

- United Arab Emirates Generative AI Market Overview by Application

- United Arab Emirates Generative AI Market Overview by Industry Sector

- SOUTH AFRICA

- South African Generative AI Market Overview by Component

- South African Generative AI Market Overview by Technology

- South African Generative AI Market Overview by Model

- South African Generative AI Market Overview by Application

- South African Generative AI Market Overview by Industry Sector

- EGYPT

- Egyptian Generative AI Market Overview by Component

- Egyptian Generative AI Market Overview by Technology

- Egyptian Generative AI Market Overview by Model

- Egyptian Generative AI Market Overview by Application

- Egyptian Generative AI Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Generative AI Market Overview by Component

- Saudi Arabian Generative AI Market Overview by Technology

- Saudi Arabian Generative AI Market Overview by Model

- Saudi Arabian Generative AI Market Overview by Application

- Saudi Arabian Generative AI Market Overview by Industry Sector

- MOROCCO

- Moroccan Generative AI Market Overview by Component

- Moroccan Generative AI Market Overview by Technology

- Moroccan Generative AI Market Overview by Model

- Moroccan Generative AI Market Overview by Application

- Moroccan Generative AI Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Generative AI Market Overview by Component

- Kuwaiti Generative AI Market Overview by Technology

- Kuwaiti Generative AI Market Overview by Model

- Kuwaiti Generative AI Market Overview by Application

- Kuwaiti Generative AI Market Overview by Industry Sector

- QATAR

- Qatari Generative AI Market Overview by Component

- Qatari Generative AI Market Overview by Technology

- Qatari Generative AI Market Overview by Model

- Qatari Generative AI Market Overview by Application

- Qatari Generative AI Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Generative AI Market Overview by Component

- Rest of Middle East & Africa Generative AI Market Overview by Technology

- Rest of Middle East & Africa Generative AI Market Overview by Model

- Rest of Middle East & Africa Generative AI Market Overview by Application

- Rest of Middle East & Africa Generative AI Market Overview by Industry Sector

PART C: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

Adobe

Amazon Web Services, Inc.

Anthropic

Atos SE

Baidu Inc.

Capgemini SE

Databricks

DeepMind Technologies Limited

De-Identification Ltd

D-ID

Fujitsu Limited

Genie AI Ltd.

Google LLC

Graphcore Ltd.

Hugging Face Inc.

IBM

Infosys Ltd.

Jasper

Microsoft Corporation

Midjourney

Mistral AI

MOSTLY AI Inc.

NTT Data Corporation

NVIDIA

OpenAI

Oracle

Rephrase.ai

SAP SE

Scale AI

SenseTime Group Ltd.

Stability AI

Synthesia

Tata Consultancy Services (TCS) Ltd.

Tencent Holdings Ltd.

TietoEVRY Corporation

Together AI

xAI

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |