Global Function-as-a-Service (FaaS) Market - Deployment Types, User Types, Company Types and Industry Sectors

- Published: Aug 2025

- Pages: 468 | Charts: 403

- Report Code: ITM135

SHARE THIS REPORT:

Global Function-as-a-Service (FaaS) Market Trends and Outlook

The global Function-as-a-Service (FaaS) market is undergoing a paradigm shift as enterprises accelerate the adoption of cloud-native architectures to support agile, event-driven applications. Valued at approximately US$16.2 billion in 2024, the market is poised for explosive growth, projected to exceed US$68.4 billion by 2030, expanding at a CAGR of 27.1%. This momentum is fueled by the increasing need for scalable, modular compute models that eliminate infrastructure management burdens while enabling faster innovation cycles. FaaS allows developers to run discrete functions in response to events, supporting real-time responsiveness and operational efficiency at a fraction of the cost of traditional architectures.

Core to this growth is the widespread adoption of microservices, Kubernetes-based orchestration, and DevOps practices that prioritize modular, stateless execution. Major cloud providers such as AWS, Microsoft Azure, and Google Cloud continue to invest in enhancing their serverless platforms, while open-source frameworks like Knative and OpenFaaS offer flexible alternatives, particularly for hybrid and private cloud environments. In parallel, the rise of multi-cloud strategies and API-first ecosystems has intensified enterprise interest in FaaS, especially for workloads requiring interoperability and elasticity across cloud boundaries.

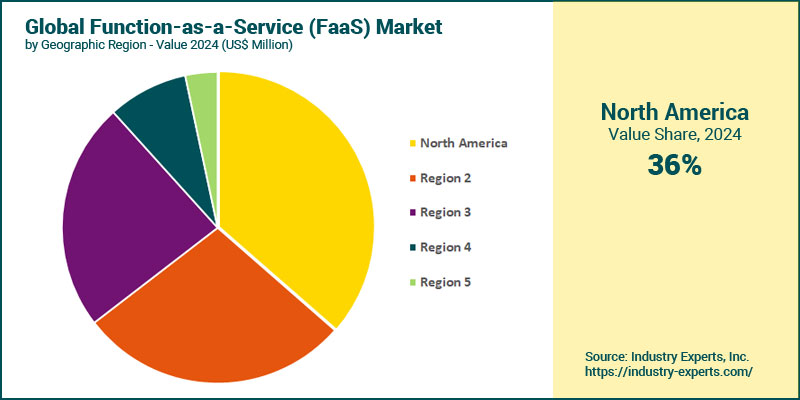

Function-as-a-Service (FaaS) Regional Market Analysis

In 2024, North America leads the FaaS market with an estimated share of 36.4%. The region's dominance is underpinned by early adoption of serverless platforms such as AWS Lambda, Azure Functions, and Google Cloud Functions, along with mature DevOps cultures and enterprise cloud strategies. Europe follows closely, driven by increasing demand for event-driven architectures and growing enterprise cloud-native adoption across industries such as finance and telecommunications. Asia-Pacific, however, is the fastest-growing regional market, expanding at a CAGR of 33.9% through 2030. This surge is fueled by rapid digital transformation across China, India, and Southeast Asia, along with strong momentum in e-commerce, fintech, and IoT-heavy applications that benefit from serverless compute scalability.

Function-as-a-Service (FaaS) Market Analysis by Deployment Type

As of 2024, public cloud remains the dominant deployment segment in the FaaS market, accounting for just over 50% of total market value. This is largely attributed to widespread availability and enterprise adoption of serverless services on platforms such as AWS, Azure, and Google Cloud, where scalability and pay-per-use economics are critical. However, the fastest growth is expected from hybrid cloud deployments, which are projected to grow at a CAGR of 30.9%. This rapid expansion reflects a surge in demand for flexible computing environments that can bridge public and on-premise infrastructure, particularly among highly regulated industries such as healthcare, finance, and government.

Function-as-a-Service (FaaS) Market Analysis by User Type

In 2024, developer-centric FaaS accounts for the largest market share at US$10.2 billion, capturing around 63% of global revenue. Its dominance stems from the rapid uptake of event-driven microservices and DevOps workflows in software development teams, who value the ability to deploy functions independently and scale modular components seamlessly. This model thrives in environments demanding agility, real-time responsiveness, and high iteration speed. On the other hand, operator-centric FaaS is the fastest-growing segment, with a projected CAGR of 30.1% through 2030. This accelerated growth reflects the increasing involvement of IT operations teams in managing infrastructure automation, security, and compliance within serverless environments. Operator-centric adoption is particularly prominent in large enterprises and regulated sectors deploying FaaS within hybrid or private clouds, where governance and observability are key priorities.

Function-as-a-Service (FaaS) Market Analysis by Company Type

Large enterprises dominate the FaaS market in 2024, cornering around 59% of global value. Their leadership is driven by aggressive modernization strategies, adoption of event-driven and microservices-based architectures, and the deployment of FaaS for critical functions such as fraud detection, real-time analytics, and customer engagement in sectors like finance, telecom, and healthcare. These organizations also benefit from well-resourced DevOps teams and integrated CI/CD pipelines that favor serverless compute models. However, the SME segment is expanding at a faster pace, with a projected CAGR of 29.4% through 2030. By 2030, SMEs are expected to reach US$31.2 billion in FaaS spending, narrowing the gap significantly. This rapid growth is propelled by the appeal of FaaS's low barrier to entry, cost-efficiency through pay-per-use models, and reduced infrastructure overhead-making it an ideal solution for startups and digitally native firms with variable workloads. Additionally, the increasing availability of low-code/no-code integrations and open-source frameworks has further lowered adoption hurdles for SMEs across regions.

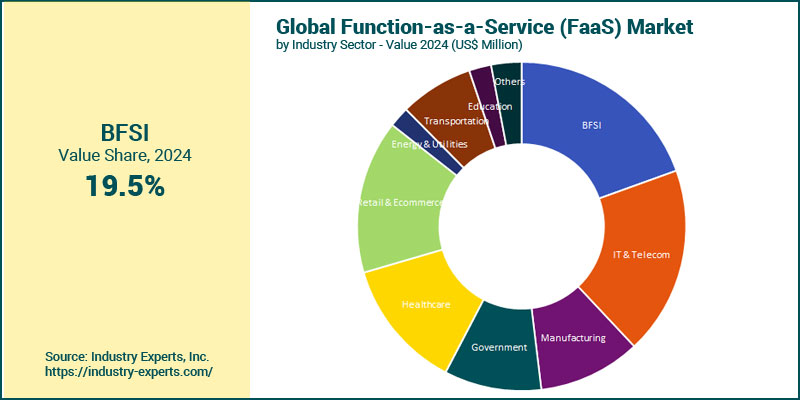

Function-as-a-Service (FaaS) Market Analysis by Industry Sector

The Banking, Financial Services, and Insurance (BFSI) sector leads the global Function-as-a-Service (FaaS) market, which represents 19.5% of global revenue in 2024. The sector's dominance is driven by heavy reliance on real-time processing for payment authentication, fraud detection, compliance automation, and digital banking services, all of which align well with FaaS's event-driven and scalable architecture. IT & Telecom emerges as the second-largest vertical. This sector is a natural fit for FaaS adoption due to its deep involvement in cloud-native application delivery, infrastructure monitoring, CI/CD workflows, and API-driven services. Telecom providers are also leveraging serverless to support 5G edge workloads and dynamic provisioning. From a growth standpoint, Retail & eCommerce is the fastest-growing Industry Sector, expanding at a 32.8% CAGR. The model's inherent elasticity and real-time responsiveness support use cases such as dynamic pricing, personalized recommendations, flash sales, and cart recovery, making it an ideal fit for modern retail.

Function-as-a-Service (FaaS) Market Report Scope

This global report on Function-as-a-Service (FaaS) market analyzes the global and regional market based on Deployment Type, User Type, Company Type, and Industry Sector for the period 2021-2030 with projection from 2024 to 2030 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Historical Period: | 2021-2024 | |

| Base Year: | 2024 | |

| Forecast Period: | 2024-2030 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 20+ |

Function-as-a-Service (FaaS) Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Function-as-a-Service (FaaS) Market by Deployment Type

- Public Cloud

- Private Cloud

- Hybrid Cloud

Function-as-a-Service (FaaS) Market by User Type

- Developer-Centric FaaS

- Operator-Centric FaaS

Function-as-a-Service (FaaS) Market by Company Type

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

Function-as-a-Service (FaaS) Market by Industry Sector

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

Function-as-a-Service (FaaS) Market Frequently Asked Questions (FAQs)

The global Function-as-a-Service (FaaS) market size is estimated at approximately US$16.2 billion in 2024.

Global FaaS market is projected to exceed US$68.4 billion by 2030, expanding at a CAGR of 27.1%.

In 2024, North America leads the FaaS market, representing 36.4% of global revenues.

Asia-Pacific, however, is the fastest-growing regional market, expanding at a CAGR of 33.9% through 2030 and projected to reach US$22.2 billion by the end of the forecast period.

As of 2024, public cloud remains the dominant deployment segment in the FaaS market, accounting for just over 50% of total market value.

Operator-centric FaaS is the fastest-growing segment, with a projected CAGR of 30.1% through 2030.

Banking, Financial Services, and Insurance (BFSI) sector leads the global Function-as-a-Service (FaaS) market, followed by IT & Telecom.

The top players in the Function-as-a-Service (FaaS) industry include Amazon Web Services (AWS Lambda), Microsoft (Azure Functions), and Google Cloud (Cloud Functions), which collectively dominate the market with robust serverless platforms and deep integration across their cloud ecosystems. Other notable providers include IBM Cloud Functions, Oracle Cloud Functions, and open-source leaders like OpenFaaS and Knative, which are gaining traction among enterprises seeking hybrid and multi-cloud flexibility.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Function-as-a-Service (FaaS)

- Market Segmentation for Function-as-a-Service (FaaS)

- Deployment Types

- User Types

- Company Types

- Industry Sectors

- Key Trends in Function-as-a-Service (FaaS) Market

2. INDUSTRY LANDSCAPE

- Global Function-as-a-Service (FaaS) Market Outlook

- Comprehensive Function-as-a-Service (FaaS) Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Function-as-a-Service (FaaS) Industry

- Startup Strategies for Function-as-a-Service (FaaS) Industry

- SWOT Analysis of Function-as-a-Service (FaaS) Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Function-as-a-Service (FaaS) Companies

- Market Share Analysis of Function-as-a-Service (FaaS) Companies

- SWOT Analysis of Key Players in the Function-as-a-Service (FaaS) Industry

- Key Market Players

- Alibaba Cloud

- Amazon Web Services, Inc.

- Cloudflare, Inc.

- Dynatrace LLC

- F5, Inc.

- Google LLC

- IBM Corporation

- Infosys Limited

- Knative

- Manjrasoft Pty Ltd.

- Microsoft Corporation

- Netlify

- OpenFaaS

- Oracle Corporation

- Perforce Software Inc.

- Platform9 Systems, Inc.

- Red Hat

- SAP SE

- TIBCO Software Inc.

- VMware Inc.

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Function-as-a-Service (FaaS) Deployment Type Market Overview by Global Region

- Public Cloud

- Private Cloud

- Hybrid Cloud

- Global Function-as-a-Service (FaaS) Market Overview by User Type

- Function-as-a-Service (FaaS) User Type Market Overview by Global Region

- Developer-Centric FaaS

- Operator-Centric FaaS

- Global Function-as-a-Service (FaaS) Market Overview by Company Type

- Function-as-a-Service (FaaS) Company Type Market Overview by Global Region

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

- Global Function-as-a-Service (FaaS) Market Overview by Industry Sector

- Function-as-a-Service (FaaS) Industry Sector Market Overview by Global Region

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

PART B: REGIONAL MARKET PERSPECTIVE

- Global Function-as-a-Service (FaaS) Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Function-as-a-Service (FaaS) Market Overview by Geographic Region

- North American Function-as-a-Service (FaaS) Market Overview by Deployment Type

- North American Function-as-a-Service (FaaS) Market Overview by User Type

- North American Function-as-a-Service (FaaS) Market Overview by Company Type

- North American Function-as-a-Service (FaaS) Market Overview by Industry Sector

- Country-wise Analysis of North American Function-as-a-Service (FaaS) Market

- THE UNITED STATES

- United States Function-as-a-Service (FaaS) Market Overview by Deployment Type

- United States Function-as-a-Service (FaaS) Market Overview by User Type

- United States Function-as-a-Service (FaaS) Market Overview by Company Type

- United States Function-as-a-Service (FaaS) Market Overview by Industry Sector

- CANADA

- Canadian Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Canadian Function-as-a-Service (FaaS) Market Overview by User Type

- Canadian Function-as-a-Service (FaaS) Market Overview by Company Type

- Canadian Function-as-a-Service (FaaS) Market Overview by Industry Sector

- MEXICO

- Mexican Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Mexican Function-as-a-Service (FaaS) Market Overview by User Type

- Mexican Function-as-a-Service (FaaS) Market Overview by Company Type

- Mexican Function-as-a-Service (FaaS) Market Overview by Industry Sector

7. EUROPE

- European Function-as-a-Service (FaaS) Market Overview by Geographic Region

- European Function-as-a-Service (FaaS) Market Overview by Deployment Type

- European Function-as-a-Service (FaaS) Market Overview by User Type

- European Function-as-a-Service (FaaS) Market Overview by Company Type

- European Function-as-a-Service (FaaS) Market Overview by Industry Sector

- Country-wise Analysis of European Function-as-a-Service (FaaS) Market

- GERMANY

- German Function-as-a-Service (FaaS) Market Overview by Deployment Type

- German Function-as-a-Service (FaaS) Market Overview by User Type

- German Function-as-a-Service (FaaS) Market Overview by Company Type

- German Function-as-a-Service (FaaS) Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Function-as-a-Service (FaaS) Market Overview by Deployment Type

- United Kingdom Function-as-a-Service (FaaS) Market Overview by User Type

- United Kingdom Function-as-a-Service (FaaS) Market Overview by Company Type

- United Kingdom Function-as-a-Service (FaaS) Market Overview by Industry Sector

- FRANCE

- French Function-as-a-Service (FaaS) Market Overview by Deployment Type

- French Function-as-a-Service (FaaS) Market Overview by User Type

- French Function-as-a-Service (FaaS) Market Overview by Company Type

- French Function-as-a-Service (FaaS) Market Overview by Industry Sector

- ITALY

- Italian Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Italian Function-as-a-Service (FaaS) Market Overview by User Type

- Italian Function-as-a-Service (FaaS) Market Overview by Company Type

- Italian Function-as-a-Service (FaaS) Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Dutch Function-as-a-Service (FaaS) Market Overview by User Type

- Dutch Function-as-a-Service (FaaS) Market Overview by Company Type

- Dutch Function-as-a-Service (FaaS) Market Overview by Industry Sector

- SPAIN

- Spanish Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Spanish Function-as-a-Service (FaaS) Market Overview by User Type

- Spanish Function-as-a-Service (FaaS) Market Overview by Company Type

- Spanish Function-as-a-Service (FaaS) Market Overview by Industry Sector

- RUSSIA

- Russian Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Russian Function-as-a-Service (FaaS) Market Overview by User Type

- Russian Function-as-a-Service (FaaS) Market Overview by Company Type

- Russian Function-as-a-Service (FaaS) Market Overview by Industry Sector

- SWITZERLAND

- Swiss Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Swiss Function-as-a-Service (FaaS) Market Overview by User Type

- Swiss Function-as-a-Service (FaaS) Market Overview by Company Type

- Swiss Function-as-a-Service (FaaS) Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Rest of Europe Function-as-a-Service (FaaS) Market Overview by User Type

- Rest of Europe Function-as-a-Service (FaaS) Market Overview by Company Type

- Rest of Europe Function-as-a-Service (FaaS) Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Function-as-a-Service (FaaS) Market Overview by Geographic Region

- Asia-Pacific Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Asia-Pacific Function-as-a-Service (FaaS) Market Overview by User Type

- Asia-Pacific Function-as-a-Service (FaaS) Market Overview by Company Type

- Asia-Pacific Function-as-a-Service (FaaS) Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Function-as-a-Service (FaaS) Market

- CHINA

- Chinese Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Chinese Function-as-a-Service (FaaS) Market Overview by User Type

- Chinese Function-as-a-Service (FaaS) Market Overview by Company Type

- Chinese Function-as-a-Service (FaaS) Market Overview by Industry Sector

- JAPAN

- Japanese Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Japanese Function-as-a-Service (FaaS) Market Overview by User Type

- Japanese Function-as-a-Service (FaaS) Market Overview by Company Type

- Japanese Function-as-a-Service (FaaS) Market Overview by Industry Sector

- INDIA

- Indian Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Indian Function-as-a-Service (FaaS) Market Overview by User Type

- Indian Function-as-a-Service (FaaS) Market Overview by Company Type

- Indian Function-as-a-Service (FaaS) Market Overview by Industry Sector

- AUSTRALIA

- Australia Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Australia Function-as-a-Service (FaaS) Market Overview by User Type

- Australia Function-as-a-Service (FaaS) Market Overview by Company Type

- Australia Function-as-a-Service (FaaS) Market Overview by Industry Sector

- SINGAPORE

- Singaporean Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Singaporean Function-as-a-Service (FaaS) Market Overview by User Type

- Singaporean Function-as-a-Service (FaaS) Market Overview by Company Type

- Singaporean Function-as-a-Service (FaaS) Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Function-as-a-Service (FaaS) Market Overview by Deployment Type

- South Korean Function-as-a-Service (FaaS) Market Overview by User Type

- South Korean Function-as-a-Service (FaaS) Market Overview by Company Type

- South Korean Function-as-a-Service (FaaS) Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Rest of Asia-Pacific Function-as-a-Service (FaaS) Market Overview by User Type

- Rest of Asia-Pacific Function-as-a-Service (FaaS) Market Overview by Company Type

- Rest of Asia-Pacific Function-as-a-Service (FaaS) Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Function-as-a-Service (FaaS) Market Overview by Geographic Region

- South American Function-as-a-Service (FaaS) Market Overview by Deployment Type

- South American Function-as-a-Service (FaaS) Market Overview by User Type

- South American Function-as-a-Service (FaaS) Market Overview by Company Type

- South American Function-as-a-Service (FaaS) Market Overview by Industry Sector

- Country-wise Analysis of South American Function-as-a-Service (FaaS) Market

- BRAZIL

- Brazilian Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Brazilian Function-as-a-Service (FaaS) Market Overview by User Type

- Brazilian Function-as-a-Service (FaaS) Market Overview by Company Type

- Brazilian Function-as-a-Service (FaaS) Market Overview by Industry Sector

- ARGENTINA

- Argentine Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Argentine Function-as-a-Service (FaaS) Market Overview by User Type

- Argentine Function-as-a-Service (FaaS) Market Overview by Company Type

- Argentine Function-as-a-Service (FaaS) Market Overview by Industry Sector

- COLOMBIA

- Colombian Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Colombian Function-as-a-Service (FaaS) Market Overview by User Type

- Colombian Function-as-a-Service (FaaS) Market Overview by Company Type

- Colombian Function-as-a-Service (FaaS) Market Overview by Industry Sector

- CHILE

- Chilean Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Chilean Function-as-a-Service (FaaS) Market Overview by User Type

- Chilean Function-as-a-Service (FaaS) Market Overview by Company Type

- Chilean Function-as-a-Service (FaaS) Market Overview by Industry Sector

- PERU

- Peruvian Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Peruvian Function-as-a-Service (FaaS) Market Overview by User Type

- Peruvian Function-as-a-Service (FaaS) Market Overview by Company Type

- Peruvian Function-as-a-Service (FaaS) Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Rest of South America Function-as-a-Service (FaaS) Market Overview by User Type

- Rest of South America Function-as-a-Service (FaaS) Market Overview by Company Type

- Rest of South America Function-as-a-Service (FaaS) Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Function-as-a-Service (FaaS) Market Overview by Geographic Region

- Middle East & Africa Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Middle East & Africa Function-as-a-Service (FaaS) Market Overview by User Type

- Middle East & Africa Function-as-a-Service (FaaS) Market Overview by Company Type

- Middle East & Africa Function-as-a-Service (FaaS) Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Function-as-a-Service (FaaS) Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Function-as-a-Service (FaaS) Market Overview by Deployment Type

- United Arab Emirates Function-as-a-Service (FaaS) Market Overview by User Type

- United Arab Emirates Function-as-a-Service (FaaS) Market Overview by Company Type

- United Arab Emirates Function-as-a-Service (FaaS) Market Overview by Industry Sector

- SOUTH AFRICA

- South African Function-as-a-Service (FaaS) Market Overview by Deployment Type

- South African Function-as-a-Service (FaaS) Market Overview by User Type

- South African Function-as-a-Service (FaaS) Market Overview by Company Type

- South African Function-as-a-Service (FaaS) Market Overview by Industry Sector

- EGYPT

- Egyptian Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Egyptian Function-as-a-Service (FaaS) Market Overview by User Type

- Egyptian Function-as-a-Service (FaaS) Market Overview by Company Type

- Egyptian Function-as-a-Service (FaaS) Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Saudi Arabian Function-as-a-Service (FaaS) Market Overview by User Type

- Saudi Arabian Function-as-a-Service (FaaS) Market Overview by Company Type

- Saudi Arabian Function-as-a-Service (FaaS) Market Overview by Industry Sector

- MOROCCO

- Moroccan Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Moroccan Function-as-a-Service (FaaS) Market Overview by User Type

- Moroccan Function-as-a-Service (FaaS) Market Overview by Company Type

- Moroccan Function-as-a-Service (FaaS) Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Kuwaiti Function-as-a-Service (FaaS) Market Overview by User Type

- Kuwaiti Function-as-a-Service (FaaS) Market Overview by Company Type

- Kuwaiti Function-as-a-Service (FaaS) Market Overview by Industry Sector

- QATAR

- Qatari Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Qatari Function-as-a-Service (FaaS) Market Overview by User Type

- Qatari Function-as-a-Service (FaaS) Market Overview by Company Type

- Qatari Function-as-a-Service (FaaS) Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Function-as-a-Service (FaaS) Market Overview by Deployment Type

- Rest of Middle East & Africa Function-as-a-Service (FaaS) Market Overview by User Type

- Rest of Middle East & Africa Function-as-a-Service (FaaS) Market Overview by Company Type

- Rest of Middle East & Africa Function-as-a-Service (FaaS) Market Overview by Industry Sector

PART C: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

Alibaba Cloud

Amazon Web Services, Inc.

Cloudflare, Inc.

Dynatrace LLC

F5, Inc.

Google LLC

IBM Corporation

Infosys Limited

Knative

Manjrasoft Pty Ltd.

Microsoft Corporation

Netlify

OpenFaaS

Oracle Corporation

Perforce Software Inc.

Platform9 Systems, Inc.

Red Hat

SAP SE

TIBCO Software Inc.

VMware Inc.

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |