Global Edge Integration Services Market - Service Types, Deployment Types, Company Types and Industry Sectors

- Published: Aug 2025

- Pages: 470 | Charts: 405

- Report Code: ITM059

SHARE THIS REPORT:

Global Edge Integration Services Market Trends and Outlook

The global Edge Integration Services market is experiencing explosive growth, rising from an estimated US$2.1 billion in 2024 to a projected US$6.4 billion by 2030, reflecting a CAGR of 20.9%. This surge is driven by enterprises embracing distributed computing models, fueled by widespread 5G adoption, rapid industrial IoT expansion, and growing hybrid cloud-edge deployments. As organizations seek to bridge the gap between localized edge environments and centralized cloud ecosystems, the demand for end-to-end integration services has intensified. From consulting and capability assessment to post-deployment optimization, vendors are being tasked with delivering low-latency, cloud-orchestrated, and compliance-ready solutions across diverse sectors.

Key market trends include the convergence of edge computing with hybrid cloud architectures, containerized edge deployments using lightweight Kubernetes frameworks (like K3s and MicroK8s), and the embedding of AI inference capabilities closer to data sources. Additionally, regulatory frameworks such as GDPR and APAC data residency mandates are influencing integration roadmaps-pushing service providers to embed encryption, access controls, and auditing capabilities directly into deployment blueprints. Vertically, industrial manufacturing leads demand due to deterministic performance needs, while IT & telecom is the fastest-growing, propelled by MEC rollouts and hyperscaler-telco collaboration.

Leading players in the Edge Integration Services market include Accenture, IBM Consulting, Capgemini, HCLTech, Infosys, Cisco Services, and Wipro, all of which are expanding edge-specific practices and forming strategic alliances with cloud providers. These vendors compete with domain-specialized players such as EdgeConneX, Siemens Digital Industries Services, and Rakuten Symphony that focus on sector-specific integration models.

Edge Integration Services Regional Market Analysis

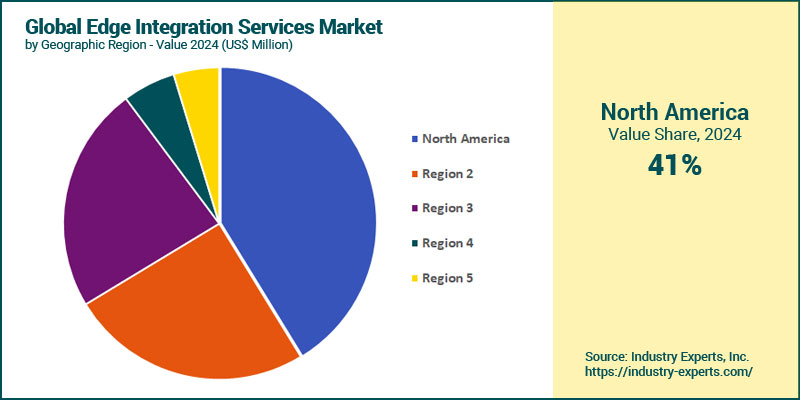

North America led the global Edge Integration Services market in 2024, accounting for 41.3% of total global revenue. This dominance is largely attributed to the region's mature hyperscaler presence, aggressive 5G rollouts, and early industrial edge adoption, particularly in manufacturing, telecom, and energy verticals. Europe followed with an estimated market size of US$518 million (25.1%), driven by Industry 4.0 initiatives, smart grid deployments, and smart city infrastructure programs across Germany, France, and the Nordics. The Asia-Pacific region is poised to register the fastest growth during 2024-2030, expanding at a CAGR of 26.8% to reach US$2 billion by 2030. Growth is especially strong in China, Japan, South Korea, and India, where robust investments in smart manufacturing, 5G-enabled IoT, and government-supported edge infrastructure rollouts are accelerating demand for integration services.

Edge Integration Services Market Analysis by Service Type

In 2024, deployment and integration support was the largest service segment, accounted for 42.1% of the global Edge Integration Services market. This dominance is driven by the complexity of initial edge infrastructure rollouts, particularly in industrial automation, smart city, and telco edge environments where real-time performance and hardware-software orchestration are critical. Consulting services followed closely with US$680 million, supported by strong demand for architecture planning, vendor selection, and regulatory readiness, especially in regions with complex data sovereignty mandates. Consulting services are projected to be the fastest-growing segment during 2024-2030, expanding at a CAGR of 22.9%. This growth is fueled by enterprises increasingly seeking advisory expertise to navigate hybrid cloud-edge convergence, container-based orchestration, and compliance-centric edge strategies. Meanwhile, post-deployment optimization services, including performance tuning, observability integration, and lifecycle management, are also growing steadily.

Edge Integration Services Market Analysis by Deployment Type

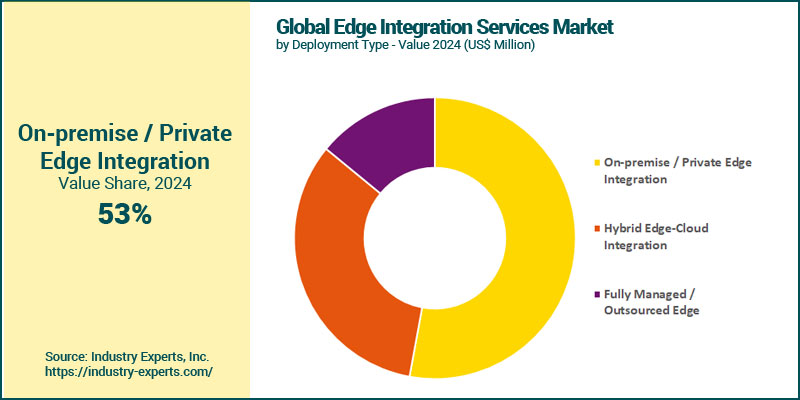

As of 2024, on-premise edge deployments hold the largest share in the Edge Integration Services market, contributing 52.9% of the global market. This leadership is driven by enterprises in regulated sectors like manufacturing, energy, and healthcare that prioritize local data processing, low-latency performance, and strict control over infrastructure due to compliance or security concerns. Looking ahead, hybrid edge deployments are set to expand at the fastest pace, growing at a CAGR of 24.2%. This rapid growth is propelled by enterprise shifts toward multi-cloud strategies, the rise of distributed applications, and the adoption of platforms like AWS Outposts, Azure Stack Edge, and Google Distributed Cloud.

Edge Integration Services Market Analysis by Company Type

Large enterprises dominated the Edge Integration Services market in 2024, accounting for approximately 65.2% of total global spending. This is largely due to their complex edge infrastructure needs spanning multiple sites, strict security and compliance mandates, and demand for lifecycle support, from consulting and deployment to post-deployment optimization. These enterprises often pursue vendor partnerships to integrate edge solutions within broader hybrid cloud ecosystems. However, small and mid-sized enterprises (SMEs) are projected to be the fastest-growing customer group during 2024-2030, expanding at a CAGR of 21.9%. Their growth is driven by increasing interest in modular edge solutions, cost-effective integration services, and consumption-based models that allow gradual scaling. SMEs are particularly active in manufacturing, retail, and smart building applications, where proof-of-concept deployments are quickly transitioning into broader rollouts.

Edge Integration Services Market Analysis by Industry Sector

In 2024, the industrial sector emerged as the largest adopter of Edge Integration Services, contributing 26.5% of the global market. This dominance is fueled by the sector's need for ultra-reliable edge infrastructure to support smart factory initiatives, SCADA integration, predictive maintenance, and latency-sensitive automation workloads. The IT & telecom segment followed closely, driven by telecom operators' deployment of multi-access edge computing (MEC), dynamic network slicing, and content distribution infrastructure. IT & telecom is also expected to be the fastest-growing vertical through 2030, registering a CAGR of 24.3% and reaching US$1.6 billion by the end of the forecast period. This surge is powered by expanding 5G networks, increased demand for distributed edge data centers, and rapid onboarding of edge-native platforms by telecom and cloud providers.

Edge Integration Services Market Report Scope

This global report on Edge Integration Services market analyzes the global and regional market based on Service Type, Company Type, Company Type and Industry Sector for the period 2021-2030 with forecasts from 2024 to 2030 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Historical Period: | 2021-2024 | |

| Base Year: | 2024 | |

| Forecast Period: | 2024-2030 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 20+ |

Edge Integration Services Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Edge Integration Services Market by Service Type

- Deployment & Integration Support

- Consulting & Advisory

- Post-deployment Support & Optimization

Edge Integration Services Market by Deployment Type

- On-premise / Private Edge Integration

- Hybrid Edge-Cloud Integration

- Fully Managed / Outsourced Edge

Edge Integration Services Market by Company Type

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

Edge Integration Services Market by Industry Sector

- Industrial Manufacturing / IIoT

- IT & Telecom

- Retail & Ecommerce

- Energy & Utilities

- Media & Entertainment

- Healthcare

- Government

- BFSI

- Education

- Other Industry Sectors

Edge Integration Services Market Frequently Asked Questions (FAQs)

As of 2024, the global Edge Integration Services market is valued at US$2.1 billion and is expected to reach US$6.4 billion by 2030, growing at a CAGR of 20.9%.

North America holds the largest regional share at 41.3% in 2024, supported by mature hyperscaler ecosystems, dense 5G coverage, and robust industrial edge adoption.

Asia-Pacific is the fastest-growing region, expanding at a CAGR of 26.8%, driven by edge initiatives in China, Japan, South Korea, and India focused on smart manufacturing and telco edge deployments.

Deployment and integration services lead the market with a 42.1% share in 2024, though consulting services are growing the fastest at 22.9% CAGR, reaching over US$2.2 billion by 2030.

Hybrid edge is the fastest-growing deployment type, projected to expand at 24.2% CAGR due to increasing enterprise demand for integrated on-prem and cloud-native edge infrastructure.

The industrial sector is the largest with 26.5% share in 2024, while IT & telecom is the fastest-growing vertical at 24.3% CAGR, benefiting from MEC, 5G, and distributed cloud infrastructure rollouts.

Top players include Accenture, IBM Consulting, Capgemini, HCLTech, Infosys, Cisco Services, and Wipro, along with domain-focused providers like EdgeConneX, Siemens Digital Industries Services, and Rakuten Symphony.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Edge Integration Services

- Market Segmentation for Edge Integration Services

- Service Types

- Deployment Types

- Company Types

- Industry Sectors

- Key Trends in Edge Integration Services Market

2. INDUSTRY LANDSCAPE

- Global Edge Integration Services Market Outlook

- Comprehensive Edge Integration Services Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Edge Integration Services Industry

- Startup Strategies for Edge Integration Services Industry

- SWOT Analysis of Edge Integration Services Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Edge Integration Services Companies

- Market Share Analysis of Edge Integration Services Companies

- SWOT Analysis of Key Players in the Edge Integration Services Industry

- Key Market Players

- Accenture

- Capgemini

- Cisco Services

- Cognizant

- Dell Technologies Services

- EdgeConneX

- Fujitsu

- HCLTech

- HPE Pointnext Services

- IBM Consulting

- Infosys

- Lumen Technologies

- MobiledgeX

- Rakuten Symphony

- Schneider Electric

- Siemens Digital Industries Services

- Supermicro Professional Services

- Tata Consultancy Services (TCS)

- Tech Mahindra

- Wipro

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Edge Integration Services Market Overview by Service Type

- Edge Integration Services Service Type Market Overview by Global Region

- Deployment & Integration Support

- Consulting & Advisory

- Post-deployment Support & Optimization

- Global Edge Integration Services Market Overview by Deployment Type

- Edge Integration Services Deployment Type Market Overview by Global Region

- On-premise / Private Edge Integration

- Hybrid Edge-Cloud Integration

- Fully Managed / Outsourced Edge

- Global Edge Integration Services Market Overview by Company Type

- Edge Integration Services Company Type Market Overview by Global Region

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

- Global Edge Integration Services Market Overview by Industry Sector

- Edge Integration Services Industry Sector Market Overview by Global Region

- Industrial Manufacturing / IIoT

- IT & Telecom

- Retail & Ecommerce

- Energy & Utilities

- Media & Entertainment

- Healthcare

- Government

- BFSI

- Education

- Other Industry Sectors

PART B: REGIONAL MARKET PERSPECTIVE

- Global Edge Integration Services Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Edge Integration Services Market Overview by Geographic Region

- North American Edge Integration Services Market Overview by Service Type

- North American Edge Integration Services Market Overview by Deployment Type

- North American Edge Integration Services Market Overview by Company Type

- North American Edge Integration Services Market Overview by Industry Sector

- Country-wise Analysis of North American Edge Integration Services Market

- THE UNITED STATES

- United States Edge Integration Services Market Overview by Service Type

- United States Edge Integration Services Market Overview by Deployment Type

- United States Edge Integration Services Market Overview by Company Type

- United States Edge Integration Services Market Overview by Industry Sector

- CANADA

- Canadian Edge Integration Services Market Overview by Service Type

- Canadian Edge Integration Services Market Overview by Deployment Type

- Canadian Edge Integration Services Market Overview by Company Type

- Canadian Edge Integration Services Market Overview by Industry Sector

- MEXICO

- Mexican Edge Integration Services Market Overview by Service Type

- Mexican Edge Integration Services Market Overview by Deployment Type

- Mexican Edge Integration Services Market Overview by Company Type

- Mexican Edge Integration Services Market Overview by Industry Sector

7. EUROPE

- European Edge Integration Services Market Overview by Geographic Region

- European Edge Integration Services Market Overview by Service Type

- European Edge Integration Services Market Overview by Deployment Type

- European Edge Integration Services Market Overview by Company Type

- European Edge Integration Services Market Overview by Industry Sector

- Country-wise Analysis of European Edge Integration Services Market

- GERMANY

- German Edge Integration Services Market Overview by Service Type

- German Edge Integration Services Market Overview by Deployment Type

- German Edge Integration Services Market Overview by Company Type

- German Edge Integration Services Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Edge Integration Services Market Overview by Service Type

- United Kingdom Edge Integration Services Market Overview by Deployment Type

- United Kingdom Edge Integration Services Market Overview by Company Type

- United Kingdom Edge Integration Services Market Overview by Industry Sector

- FRANCE

- French Edge Integration Services Market Overview by Service Type

- French Edge Integration Services Market Overview by Deployment Type

- French Edge Integration Services Market Overview by Company Type

- French Edge Integration Services Market Overview by Industry Sector

- ITALY

- Italian Edge Integration Services Market Overview by Service Type

- Italian Edge Integration Services Market Overview by Deployment Type

- Italian Edge Integration Services Market Overview by Company Type

- Italian Edge Integration Services Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Edge Integration Services Market Overview by Service Type

- Dutch Edge Integration Services Market Overview by Deployment Type

- Dutch Edge Integration Services Market Overview by Company Type

- Dutch Edge Integration Services Market Overview by Industry Sector

- SPAIN

- Spanish Edge Integration Services Market Overview by Service Type

- Spanish Edge Integration Services Market Overview by Deployment Type

- Spanish Edge Integration Services Market Overview by Company Type

- Spanish Edge Integration Services Market Overview by Industry Sector

- RUSSIA

- Russian Edge Integration Services Market Overview by Service Type

- Russian Edge Integration Services Market Overview by Deployment Type

- Russian Edge Integration Services Market Overview by Company Type

- Russian Edge Integration Services Market Overview by Industry Sector

- SWITZERLAND

- Swiss Edge Integration Services Market Overview by Service Type

- Swiss Edge Integration Services Market Overview by Deployment Type

- Swiss Edge Integration Services Market Overview by Company Type

- Swiss Edge Integration Services Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Edge Integration Services Market Overview by Service Type

- Rest of Europe Edge Integration Services Market Overview by Deployment Type

- Rest of Europe Edge Integration Services Market Overview by Company Type

- Rest of Europe Edge Integration Services Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Edge Integration Services Market Overview by Geographic Region

- Asia-Pacific Edge Integration Services Market Overview by Service Type

- Asia-Pacific Edge Integration Services Market Overview by Deployment Type

- Asia-Pacific Edge Integration Services Market Overview by Company Type

- Asia-Pacific Edge Integration Services Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Edge Integration Services Market

- CHINA

- Chinese Edge Integration Services Market Overview by Service Type

- Chinese Edge Integration Services Market Overview by Deployment Type

- Chinese Edge Integration Services Market Overview by Company Type

- Chinese Edge Integration Services Market Overview by Industry Sector

- JAPAN

- Japanese Edge Integration Services Market Overview by Service Type

- Japanese Edge Integration Services Market Overview by Deployment Type

- Japanese Edge Integration Services Market Overview by Company Type

- Japanese Edge Integration Services Market Overview by Industry Sector

- INDIA

- Indian Edge Integration Services Market Overview by Service Type

- Indian Edge Integration Services Market Overview by Deployment Type

- Indian Edge Integration Services Market Overview by Company Type

- Indian Edge Integration Services Market Overview by Industry Sector

- AUSTRALIA

- Australia Edge Integration Services Market Overview by Service Type

- Australia Edge Integration Services Market Overview by Deployment Type

- Australia Edge Integration Services Market Overview by Company Type

- Australia Edge Integration Services Market Overview by Industry Sector

- SINGAPORE

- Singaporean Edge Integration Services Market Overview by Service Type

- Singaporean Edge Integration Services Market Overview by Deployment Type

- Singaporean Edge Integration Services Market Overview by Company Type

- Singaporean Edge Integration Services Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Edge Integration Services Market Overview by Service Type

- South Korean Edge Integration Services Market Overview by Deployment Type

- South Korean Edge Integration Services Market Overview by Company Type

- South Korean Edge Integration Services Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Edge Integration Services Market Overview by Service Type

- Rest of Asia-Pacific Edge Integration Services Market Overview by Deployment Type

- Rest of Asia-Pacific Edge Integration Services Market Overview by Company Type

- Rest of Asia-Pacific Edge Integration Services Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Edge Integration Services Market Overview by Geographic Region

- South American Edge Integration Services Market Overview by Service Type

- South American Edge Integration Services Market Overview by Deployment Type

- South American Edge Integration Services Market Overview by Company Type

- South American Edge Integration Services Market Overview by Industry Sector

- Country-wise Analysis of South American Edge Integration Services Market

- BRAZIL

- Brazilian Edge Integration Services Market Overview by Service Type

- Brazilian Edge Integration Services Market Overview by Deployment Type

- Brazilian Edge Integration Services Market Overview by Company Type

- Brazilian Edge Integration Services Market Overview by Industry Sector

- ARGENTINA

- Argentine Edge Integration Services Market Overview by Service Type

- Argentine Edge Integration Services Market Overview by Deployment Type

- Argentine Edge Integration Services Market Overview by Company Type

- Argentine Edge Integration Services Market Overview by Industry Sector

- COLOMBIA

- Colombian Edge Integration Services Market Overview by Service Type

- Colombian Edge Integration Services Market Overview by Deployment Type

- Colombian Edge Integration Services Market Overview by Company Type

- Colombian Edge Integration Services Market Overview by Industry Sector

- CHILE

- Chilean Edge Integration Services Market Overview by Service Type

- Chilean Edge Integration Services Market Overview by Deployment Type

- Chilean Edge Integration Services Market Overview by Company Type

- Chilean Edge Integration Services Market Overview by Industry Sector

- PERU

- Peruvian Edge Integration Services Market Overview by Service Type

- Peruvian Edge Integration Services Market Overview by Deployment Type

- Peruvian Edge Integration Services Market Overview by Company Type

- Peruvian Edge Integration Services Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Edge Integration Services Market Overview by Service Type

- Rest of South America Edge Integration Services Market Overview by Deployment Type

- Rest of South America Edge Integration Services Market Overview by Company Type

- Rest of South America Edge Integration Services Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Edge Integration Services Market Overview by Geographic Region

- Middle East & Africa Edge Integration Services Market Overview by Service Type

- Middle East & Africa Edge Integration Services Market Overview by Deployment Type

- Middle East & Africa Edge Integration Services Market Overview by Company Type

- Middle East & Africa Edge Integration Services Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Edge Integration Services Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Edge Integration Services Market Overview by Service Type

- United Arab Emirates Edge Integration Services Market Overview by Deployment Type

- United Arab Emirates Edge Integration Services Market Overview by Company Type

- United Arab Emirates Edge Integration Services Market Overview by Industry Sector

- SOUTH AFRICA

- South African Edge Integration Services Market Overview by Service Type

- South African Edge Integration Services Market Overview by Deployment Type

- South African Edge Integration Services Market Overview by Company Type

- South African Edge Integration Services Market Overview by Industry Sector

- EGYPT

- Egyptian Edge Integration Services Market Overview by Service Type

- Egyptian Edge Integration Services Market Overview by Deployment Type

- Egyptian Edge Integration Services Market Overview by Company Type

- Egyptian Edge Integration Services Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Edge Integration Services Market Overview by Service Type

- Saudi Arabian Edge Integration Services Market Overview by Deployment Type

- Saudi Arabian Edge Integration Services Market Overview by Company Type

- Saudi Arabian Edge Integration Services Market Overview by Industry Sector

- MOROCCO

- Moroccan Edge Integration Services Market Overview by Service Type

- Moroccan Edge Integration Services Market Overview by Deployment Type

- Moroccan Edge Integration Services Market Overview by Company Type

- Moroccan Edge Integration Services Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Edge Integration Services Market Overview by Service Type

- Kuwaiti Edge Integration Services Market Overview by Deployment Type

- Kuwaiti Edge Integration Services Market Overview by Company Type

- Kuwaiti Edge Integration Services Market Overview by Industry Sector

- QATAR

- Qatari Edge Integration Services Market Overview by Service Type

- Qatari Edge Integration Services Market Overview by Deployment Type

- Qatari Edge Integration Services Market Overview by Company Type

- Qatari Edge Integration Services Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Edge Integration Services Market Overview by Service Type

- Rest of Middle East & Africa Edge Integration Services Market Overview by Deployment Type

- Rest of Middle East & Africa Edge Integration Services Market Overview by Company Type

- Rest of Middle East & Africa Edge Integration Services Market Overview by Industry Sector

PART C: INDUSTRY GUIDE

PART D: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

Accenture

Capgemini

Cisco Services

Cognizant

Dell Technologies Services

EdgeConneX

Fujitsu

HCLTech

HPE Pointnext Services

IBM Consulting

Infosys

Lumen Technologies

MobiledgeX

Rakuten Symphony

Schneider Electric

Siemens Digital Industries Services

Supermicro Professional Services

Tata Consultancy Services (TCS)

Tech Mahindra

Wipro

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |