Cloud Management Platform - A Global Market Overview

- Published: Aug 2025

- Pages: 586 | Charts: 492

- Report Code: ITM003

SHARE THIS REPORT:

Global Cloud Management Platform Market Trends and Outlook

The global Cloud Management Platform (CMP) market is undergoing rapid transformation as enterprises increasingly adopt hybrid and multi-cloud strategies to enhance operational agility, scalability, and cost control. CMPs offer centralized control, visibility, and automation across diverse cloud environments, spanning public, private, and on-premises systems, enabling organizations to orchestrate workloads, optimize resource utilization, and ensure compliance. With nearly 90% of businesses now using multi-cloud approaches, the demand for robust management platforms has surged. These platforms support a wide array of functions, including provisioning, cost optimization, security governance, and performance monitoring, making them essential tools in navigating the complexities of modern IT infrastructure.

The market is projected to grow from US$21 billion in 2024 to US$54.8 billion by 2030, registering a CAGR of 17.3%, driven by increased digital transformation efforts, AI-powered automation (AIOps), and the proliferation of cloud-native applications. Large enterprises continue to lead CMP adoption due to their extensive infrastructure needs, while small and medium-sized enterprises (SMEs) are emerging as a high-growth segment, leveraging cost-effective, cloud-first solutions. Critical sectors such as BFSI, healthcare, retail, and telecom are turning to CMPs to support scalable, secure, and efficient digital operations. As cloud environments become more distributed and data-intensive, the role of cloud management platforms will be increasingly pivotal in enabling business continuity, innovation, and sustainable IT modernization.

Cloud Management Platform Regional Market Analysis

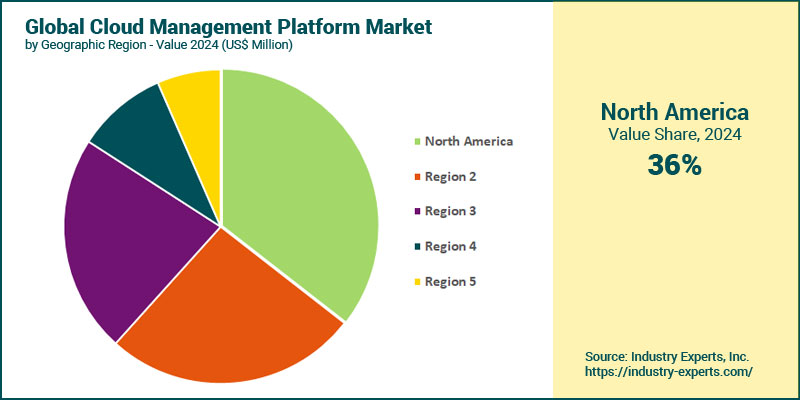

North America leads the global demand for Cloud Management Platform with a share estimated at 35.5% in 2024 due to a number of factors. The region has a leadership position in adopting technologies such as artificial intelligence (AI), machine learning (ML), big data and IoT, all of which require scalable cloud infrastructure. Hence, North America's dominant position can be attributed to early adoption by of CMPs by organizations, especially in the United States, which is the base of some leading cloud service providers, including Amazon Web Services (AWS), Microsoft Azure and Google Cloud Platform (GCP). The market for Cloud Management Platform in Asia-Pacific, however, is primed to post the fastest CAGR of 21.4% during 2024-2030, owing to a surge in digital transformation, driven by rapid economic growth, increasing internet penetration and a tech-savvy population. Adoption of cloud solutions in the region has proven to enhance business efficiency, with China, India and Southeast Asian countries being at the forefront of this advancement. Government initiatives and investments, such as China's US$1.4 trillion tech investment plan and India's Meghraj initiative, are stimulating cloud adoption for enhancing digital economies and e-governance. Asia-Pacific, especially its Southeast region, is home to a large number of small and medium enterprises (SMEs) that have taken to adopting cloud solutions for cost-effectiveness and scalability.

Cloud Management Platform Market Analysis by Component Type

With an estimated share of 64.4% in 2024, the worldwide market for Cloud Management Platform by component type is dominated by Software/Platform owing to several factors. The growing need among businesses for comprehensive and integrated solutions that can manage complex, multi-cloud and hybrid cloud environments increases demand for software solutions that can provide centralized control. Because of this, resources are managed efficiently, costs are optimized and security is ensured, all of which are crucial for handling diverse cloud infrastructures. Widespread utilization of multi-cloud and hybrid cloud strategies is further boosting the need for software platforms that offer unified management, visibility and governance across different cloud providers, such as AWS, Azure & GCP, and on-premises systems for simplifying operations and minimizing complexity. On the other hand, the Services component of the global Cloud Management Platform market is likely to post a faster 2024-2030 CAGR of 17.8%, a key reason for which is growing demand for managed services. Enterprises, especially SMEs, are preferring to outsource cloud management for reducing complexity and operating costs, thereby increasing demand for managed services, such as consulting, implementation and support.

Cloud Management Platform Market Analysis by Deployment Type

The worldwide market for Cloud Management Platform by deployment is the largest for Public Cloud, estimated to account for 50% of the overall market in 2024. The extremely high level of scalability offered by public clouds helps enterprises to dynamically adjust resources based on demand. Due to this flexibility, it becomes easier to handle fluctuating workloads, such as seasonal spikes, without overprovisioning. As managing the underlying infrastructure, including hardware, software updates and maintenance, is taken care of by public cloud providers, the burden on internal IT teams is reduced to a great extent. As a result, organizations are free to focus on application development and business operations, instead of expending valuable time on infrastructure management. The global demand for Other Deployment Types, including hybrid and multi-cloud, though, is anticipated to maintain the fastest CAGR of 19.5% between 2024 and 2030. Hybrid clouds combine the cost-effectiveness and scalability of public clouds with the control and security of private clouds. This allows businesses to employ hybrid clouds for balancing sensitive workloads, such as compliance-driven data on private clouds and less-critical workloads on public clouds, which facilitates flexibility and "cloud bursting" for peak demand. In the same manner, multi-cloud allows leveraging multiple public cloud providers for optimizing performance, reducing vendor lock-in and opting for the best services for specific workloads. Data from one 2023 study reveals that almost 90% of enterprises are using multi-cloud solutions, underscoring its rapid and widespread adoption.

Cloud Management Platform Market Analysis by Company Type

Estimated to corner a share of 70.7% in 2024, Large Enterprises form the largest company type deploying CMPs due to their extensive IT infrastructure requirements. Large companies typically manage complex, large-scale IT environments with diverse workloads across multiple regions. The orchestration, monitoring and optimization of such expansive infrastructures can be enabled by cloud management platforms with centralized tools offered by them. Moreover, big organizations usually do not have budgetary limitations and can invest in comprehensive cloud solutions, including public, private and hybrid cloud deployments. Although large enterprises dominate the CMPs market in scale, Small & Medium-sized Enterprises (SMEs) will likely post a faster 2024-2030 CAGR of 18.3%. The rapid adoption of cloud solutions by SMEs is aimed at being competitive with large companies without substantial initial outlays. To this end, SMEs are gaining advantage from the pay-as-you-go pricing of public clouds that fits into their limited budgets. Benefits of CMPs for SMEs include optimization of cloud spending, monitoring usage and avoiding cost overruns. The greater agility of SMEs compared to large businesses makes rapid adoption of cloud management platforms easier to support digital transformation, AI and IoT initiatives. Owing to this, SMEs can deploy modern applications with a reasonable IT infrastructure.

Cloud Management Platform Market Analysis by Application

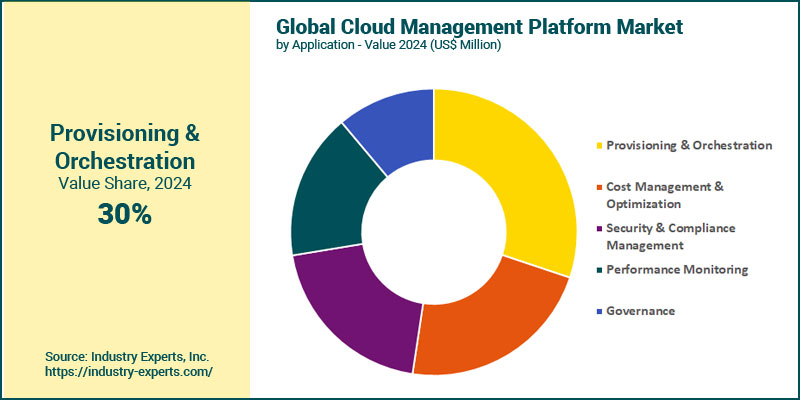

The global market for Provisioning & Orchestration applications, other than being the largest for CMPs with an estimated share of 30.1% in 2024, are also expected to clock the fastest 2024-2030 CAGR of 20.5% because of the vital role they play in managing cloud environments efficiently. Provisioning, involving allocation of resources, such as compute, storage & networking, and orchestration that automates & coordinates workflows across these resources, are the fundamental processes of cloud management. Using these functions, organizations can seamlessly deploy, manage and scale cloud resources, rendering them to be the most widely used application. As a major proportion of enterprises are using public cloud and multi-cloud strategies, managing resources across diverse platforms, such as AWS, Azure and GCP requires provisioning & orchestration tools for obtaining centralized control to minimize complexity in heterogeneous environments. Large, medium and small enterprises are all in the same boat as far as reliance on automation to reduce manual effort and errors in resource allocation and workflow management are concerned. Cloud management platforms with robust provisioning and orchestration capabilities enable automating tasks, such as virtual machine deployment, container orchestration and load balancing, driving their widespread adoption. Provisioning and orchestration further allow for rapid scaling of resources to address fluctuating workloads, such as during peak traffic periods.

Cloud Management Platform Market Analysis by Industry Sector

The BFSI sector leads the global demand for Cloud Management Platforms with an estimated share of 21.6% in 2024, owing to its extensive reliance on technology to manage complex, high-stakes operations. Companies in this sector typically handle massive volumes of transactions and sensitive data, such as customer accounts and payment processing. CMPs provide the scalability and orchestration required for the efficient management of these workloads across public, private or hybrid clouds. The BFSI sector has to operate under a range of stringent regulations across regions, including GDPR, PCI-DSS and Basel III. Addressing these regulatory requirements, even while leveraging cloud scalability. Is being facilitated by cloud management platforms in terms of robust governance, compliance monitoring and security features. The legacy systems using which many BFSI organizations function require integration with modern cloud infrastructure. However, reflecting a forecast CAGR of 21.9% over 2024-2030, Retail & Ecommerce are poised to be the fastest growing sectors for Cloud Management Platforms due to their rapid digital transformation and dynamic business needs. The ecommerce boom, accelerated by shifts in consumer behavior, is driving demand for scalable cloud infrastructure, with retailers leveraging cloud management platforms for handling peak traffic and deploying new services quickly. Elastic cloud resources are essential for businesses in the retail & ecommerce areas due to variable demand.

Cloud Management Platform Market Report Scope

This global report on Cloud Management Platform analyzes the market based on Component Type, Deployment Type, Company Type, Application Type and Industry Sector for the period 2021-2030 with projections from 2024 to 2030 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Historical Period: | 2021-2024 | |

| Base Year: | 2024 | |

| Forecast Period: | 2024-2030 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 35+ |

Cloud Management Platform Market by Geographic Region

- North America (United States, Canada and Mexico)

- Europe (Germany, United Kingdom, France, Italy, Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Cloud Management Platform Market by Component Type

- Software/Platform

- Services

Cloud Management Platform Market by Deployment Type

- Public Cloud

- Private Cloud

- Other Deployment Types

Cloud Management Platform Market by Company Type

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

Cloud Management Platform Market by Application

- Provisioning & Orchestration

- Cost Management & Optimization

- Security & Compliance Management

- Performance Monitoring

- Governance

Cloud Management Platform Market by Industry Sector

- BFSI (Banking, Financial Services, Insurance)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Verticals

Cloud Management Platform Market Frequently Asked Questions (FAQs)

The global market for Cloud Management Platform is likely to register a CAGR of 17.3% over the 2024-2030 analysis period.

North America is the largest global market for Cloud Management Platform, estimated to account for a share of 35.5% in 2024.

Asia-Pacific is likely to be the fastest growing region for Cloud Management Platform, with a forecast CAGR of 21.4% between 2024 and 2030.

Software/Platform corners the largest share of the global Cloud Management Platform market, estimated at 64.4% in 2024.

With a forecast 2024-2030 CAGR of 21.9%, Retail & Ecommerce is anticipated to be the fastest growing industry sector for Cloud Management Platform.

The demand for Cloud Management Platform is being driven by a number of factors, including rising adoption of multi-cloud & hybrid cloud, increasing complexity of cloud environments, greater need for automation & AIOps, wider adoption by SMEs, digital transformation initiatives and growth in data center & cloud video streaming.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Cloud Management Platform

- Cloud Management Platform Based on Component Type

- Cloud Management Platform Based on Deployment Type

- Cloud Management Platform Based on Company Type

- Cloud Management Platform Based on Application

- Cloud Management Platform Based on Industry Sector

2. INDUSTRY LANDSCAPE

- Global Cloud Management Platform Market Outlook

- Growth Drivers of Cloud Management Platform Market

- Challenges Inhibiting Cloud Management Platform Market Growth and Mitigating Strategies

- How Cloud Management Platform are Being Adopted by Industry

- Cloud Management Platform Industry – SWOT Analysis

- Strengths

- Weaknesses

- Opportunities

- Threats

- Strategic Cloud Management Platform Industry Analysis

- Porter's Five Forces Analysis

- PESTEL Analysis

- Market Entry & Startup Strategies for Cloud Management Platform Market

- Market Entry Strategies

- Startup Trends

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Cloud Management Platform Companies

- Market Share Analysis of Cloud Management Platform

- Pricing Analysis of Cloud Management Platform

- An Exhaustive Analysis of Cloud Management Platform in Untapped Markets

- Key Market Players

- Amazon Web Services Inc.

- Apptio Inc.

- BMC Software Inc.

- Cisco Systems Inc.

- Citrix Systems Inc.

- CloudBolt Software Inc.

- CloudCheckr Inc.

- CloudHealth Technologies Inc.

- Cognizant (US)

- Cohesity Inc.

- CoreStack

- Datadog(US)

- Dell Technologies Inc.

- Flexera Software LLC

- Fugue Inc.

- Google LLC

- Hashi Corp (North America)

- Hewlett Packard Enterprise Company

- International Business Machines Corporation

- LogicMonitor Inc.

- MicroFocus (UK)

- Microsoft Corporation

- Morpheus Data

- NetApp Inc.

- New Relic Inc.

- Nutanix Inc.

- OpsRamp Inc.

- ParkMyCloud Inc.

- Platform9

- Rapid7 LLC

- Red Hat Inc.

- Scality Inc.

- ServiceNow Inc.

- Snow Software (Sweden)

- Splunk Inc.

- Stratodesk Corporation

- Turbonomic Inc.

- VMware Inc.

- Zenoss Inc.

4. KEY BUSINESS & PRODUCT TRENDS

- Important Recent Industry Activity

- Recent Major Product Launches by the Market Leaders

5. GLOBAL MARKET OVERVIEW

- Global Cloud Management Platform Market Overview by Component Type

- Cloud Management Platform Component Type Market Overview by Global Region

- Software/Platform

- Services

- Global Cloud Management Platform Market Overview by Deployment Type

- Cloud Management Platform Deployment Type Market Overview by Global Region

- Public Cloud

- Private Cloud

- Other Deployment Types

- Global Cloud Management Platform Market Overview by Company Type

- Cloud Management Platform Company Type Market Overview by Global Region

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

- Global Cloud Management Platform Market Overview by Application

- Cloud Management Platform Application Market Overview by Global Region

- Provisioning & Orchestration

- Cost Management & Optimization

- Security & Compliance Management

- Performance Monitoring

- Governance

- Global Cloud Management Platform Market Overview by Industry Sector

- Cloud Management Platform Industry Sector Market Overview by Global Region

- BFSI (Banking, Financial Services, Insurance)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Verticals

PART B: REGIONAL MARKET PERSPECTIVE

REGIONAL MARKET OVERVIEW

- Global Cloud Management Platform Market Overview by Geographic Region

6. NORTH AMERICA

- North American Cloud Management Platform Market Overview by Geographic Region

- North American Cloud Management Platform Market Overview by Component Type

- North American Cloud Management Platform Market Overview by Deployment Type

- North American Cloud Management Platform Market Overview by Company Type

- North American Cloud Management Platform Market Overview by Application

- North American Cloud Management Platform Market Overview by Industry Sector

- Country-wise Analysis of North American Cloud Management Platform Market

- THE UNITED STATES

- United States Cloud Management Platform Market Overview by Component Type

- United States Cloud Management Platform Market Overview by Deployment Type

- United States Cloud Management Platform Market Overview by Company Type

- United States Cloud Management Platform Market Overview by Application

- United States Cloud Management Platform Market Overview by Industry Sector

- CANADA

- Canadian Cloud Management Platform Market Overview by Component Type

- Canadian Cloud Management Platform Market Overview by Deployment Type

- Canadian Cloud Management Platform Market Overview by Company Type

- Canadian Cloud Management Platform Market Overview by Application

- Canadian Cloud Management Platform Market Overview by Industry Sector

- MEXICO

- Mexican Cloud Management Platform Market Overview by Component Type

- Mexican Cloud Management Platform Market Overview by Deployment Type

- Mexican Cloud Management Platform Market Overview by Company Type

- Mexican Cloud Management Platform Market Overview by Application

- Mexican Cloud Management Platform Market Overview by Industry Sector

7. EUROPE

- European Cloud Management Platform Market Overview by Geographic Region

- European Cloud Management Platform Market Overview by Component Type

- European Cloud Management Platform Market Overview by Deployment Type

- European Cloud Management Platform Market Overview by Company Type

- European Cloud Management Platform Market Overview by Application

- European Cloud Management Platform Market Overview by Industry Sector

- Country-wise Analysis of European Cloud Management Platform Market

- GERMANY

- German Cloud Management Platform Market Overview by Component Type

- German Cloud Management Platform Market Overview by Deployment Type

- German Cloud Management Platform Market Overview by Company Type

- German Cloud Management Platform Market Overview by Application

- German Cloud Management Platform Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Cloud Management Platform Market Overview by Component Type

- United Kingdom Cloud Management Platform Market Overview by Deployment Type

- United Kingdom Cloud Management Platform Market Overview by Company Type

- United Kingdom Cloud Management Platform Market Overview by Application

- United Kingdom Cloud Management Platform Market Overview by Industry Sector

- FRANCE

- French Cloud Management Platform Market Overview by Component Type

- French Cloud Management Platform Market Overview by Deployment Type

- French Cloud Management Platform Market Overview by Company Type

- French Cloud Management Platform Market Overview by Application

- French Cloud Management Platform Market Overview by Industry Sector

- ITALY

- Italian Cloud Management Platform Market Overview by Component Type

- Italian Cloud Management Platform Market Overview by Deployment Type

- Italian Cloud Management Platform Market Overview by Company Type

- Italian Cloud Management Platform Market Overview by Application

- Italian Cloud Management Platform Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Cloud Management Platform Market Overview by Component Type

- Dutch Cloud Management Platform Market Overview by Deployment Type

- Dutch Cloud Management Platform Market Overview by Company Type

- Dutch Cloud Management Platform Market Overview by Application

- Dutch Cloud Management Platform Market Overview by Industry Sector

- SPAIN

- Spanish Cloud Management Platform Market Overview by Component Type

- Spanish Cloud Management Platform Market Overview by Deployment Type

- Spanish Cloud Management Platform Market Overview by Company Type

- Spanish Cloud Management Platform Market Overview by Application

- Spanish Cloud Management Platform Market Overview by Industry Sector

- RUSSIA

- Russian Cloud Management Platform Market Overview by Component Type

- Russian Cloud Management Platform Market Overview by Deployment Type

- Russian Cloud Management Platform Market Overview by Company Type

- Russian Cloud Management Platform Market Overview by Application

- Russian Cloud Management Platform Market Overview by Industry Sector

- SWITZERLAND

- Swiss Cloud Management Platform Market Overview by Component Type

- Swiss Cloud Management Platform Market Overview by Deployment Type

- Swiss Cloud Management Platform Market Overview by Company Type

- Swiss Cloud Management Platform Market Overview by Application

- Swiss Cloud Management Platform Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Cloud Management Platform Market Overview by Component Type

- Rest of Europe Cloud Management Platform Market Overview by Deployment Type

- Rest of Europe Cloud Management Platform Market Overview by Company Type

- Rest of Europe Cloud Management Platform Market Overview by Application

- Rest of Europe Cloud Management Platform Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Cloud Management Platform Market Overview by Geographic Region

- Asia-Pacific Cloud Management Platform Market Overview by Component Type

- Asia-Pacific Cloud Management Platform Market Overview by Deployment Type

- Asia-Pacific Cloud Management Platform Market Overview by Company Type

- Asia-Pacific Cloud Management Platform Market Overview by Application

- Asia-Pacific Cloud Management Platform Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Cloud Management Platform Market

- CHINA

- Chinese Cloud Management Platform Market Overview by Component Type

- Chinese Cloud Management Platform Market Overview by Deployment Type

- Chinese Cloud Management Platform Market Overview by Company Type

- Chinese Cloud Management Platform Market Overview by Application

- Chinese Cloud Management Platform Market Overview by Industry Sector

- JAPAN

- Japanese Cloud Management Platform Market Overview by Component Type

- Japanese Cloud Management Platform Market Overview by Deployment Type

- Japanese Cloud Management Platform Market Overview by Company Type

- Japanese Cloud Management Platform Market Overview by Application

- Japanese Cloud Management Platform Market Overview by Industry Sector

- INDIA

- Indian Cloud Management Platform Market Overview by Component Type

- Indian Cloud Management Platform Market Overview by Deployment Type

- Indian Cloud Management Platform Market Overview by Company Type

- Indian Cloud Management Platform Market Overview by Application

- Indian Cloud Management Platform Market Overview by Industry Sector

- AUSTRALIA

- Australian Cloud Management Platform Market Overview by Component Type

- Australian Cloud Management Platform Market Overview by Deployment Type

- Australian Cloud Management Platform Market Overview by Company Type

- Australian Cloud Management Platform Market Overview by Application

- Australian Cloud Management Platform Market Overview by Industry Sector

- SINGAPORE

- Singaporean Cloud Management Platform Market Overview by Component Type

- Singaporean Cloud Management Platform Market Overview by Deployment Type

- Singaporean Cloud Management Platform Market Overview by Company Type

- Singaporean Cloud Management Platform Market Overview by Application

- Singaporean Cloud Management Platform Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Cloud Management Platform Market Overview by Component Type

- South Korean Cloud Management Platform Market Overview by Deployment Type

- South Korean Cloud Management Platform Market Overview by Company Type

- South Korean Cloud Management Platform Market Overview by Application

- South Korean Cloud Management Platform Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Cloud Management Platform Market Overview by Component Type

- Rest of Asia-Pacific Cloud Management Platform Market Overview by Deployment Type

- Rest of Asia-Pacific Cloud Management Platform Market Overview by Company Type

- Rest of Asia-Pacific Cloud Management Platform Market Overview by Application

- Rest of Asia-Pacific Cloud Management Platform Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Cloud Management Platform Market Overview by Geographic Region

- South American Cloud Management Platform Market Overview by Component Type

- South American Cloud Management Platform Market Overview by Deployment Type

- South American Cloud Management Platform Market Overview by Company Type

- South American Cloud Management Platform Market Overview by Application

- South American Cloud Management Platform Market Overview by Industry Sector

- Country-wise Analysis of South American Cloud Management Platform Market

- BRAZIL

- Brazilian Cloud Management Platform Market Overview by Component Type

- Brazilian Cloud Management Platform Market Overview by Deployment Type

- Brazilian Cloud Management Platform Market Overview by Company Type

- Brazilian Cloud Management Platform Market Overview by Application

- Brazilian Cloud Management Platform Market Overview by Industry Sector

- ARGENTINA

- Argentine Cloud Management Platform Market Overview by Component Type

- Argentine Cloud Management Platform Market Overview by Deployment Type

- Argentine Cloud Management Platform Market Overview by Company Type

- Argentine Cloud Management Platform Market Overview by Application

- Argentine Cloud Management Platform Market Overview by Industry Sector

- COLOMBIA

- Colombian Cloud Management Platform Market Overview by Component Type

- Colombian Cloud Management Platform Market Overview by Deployment Type

- Colombian Cloud Management Platform Market Overview by Company Type

- Colombian Cloud Management Platform Market Overview by Application

- Colombian Cloud Management Platform Market Overview by Industry Sector

- CHILE

- Chilean Cloud Management Platform Market Overview by Component Type

- Chilean Cloud Management Platform Market Overview by Deployment Type

- Chilean Cloud Management Platform Market Overview by Company Type

- Chilean Cloud Management Platform Market Overview by Application

- Chilean Cloud Management Platform Market Overview by Industry Sector

- PERU

- Peruvian Cloud Management Platform Market Overview by Component Type

- Peruvian Cloud Management Platform Market Overview by Deployment Type

- Peruvian Cloud Management Platform Market Overview by Company Type

- Peruvian Cloud Management Platform Market Overview by Application

- Peruvian Cloud Management Platform Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Cloud Management Platform Market Overview by Component Type

- Rest of South America Cloud Management Platform Market Overview by Deployment Type

- Rest of South America Cloud Management Platform Market Overview by Company Type

- Rest of South America Cloud Management Platform Market Overview by Application

- Rest of South America Cloud Management Platform Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Cloud Management Platform Market Overview by Geographic Region

- Middle East & Africa Cloud Management Platform Market Overview by Component Type

- Middle East & Africa Cloud Management Platform Market Overview by Deployment Type

- Middle East & Africa Cloud Management Platform Market Overview by Company Type

- Middle East & Africa Cloud Management Platform Market Overview by Application

- Middle East & Africa Cloud Management Platform Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Cloud Management Platform Market

- UNITED ARAB EMIRATES

- United Arab Emirates Cloud Management Platform Market Overview by Component Type

- United Arab Emirates Cloud Management Platform Market Overview by Deployment Type

- United Arab Emirates Cloud Management Platform Market Overview by Company Type

- United Arab Emirates Cloud Management Platform Market Overview by Application

- United Arab Emirates Cloud Management Platform Market Overview by Industry Sector

- SOUTH AFRICA

- South African Cloud Management Platform Market Overview by Component Type

- South African Cloud Management Platform Market Overview by Deployment Type

- South African Cloud Management Platform Market Overview by Company Type

- South African Cloud Management Platform Market Overview by Application

- South African Cloud Management Platform Market Overview by Industry Sector

- EGYPT

- Egyptian Cloud Management Platform Market Overview by Component Type

- Egyptian Cloud Management Platform Market Overview by Deployment Type

- Egyptian Cloud Management Platform Market Overview by Company Type

- Egyptian Cloud Management Platform Market Overview by Application

- Egyptian Cloud Management Platform Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Cloud Management Platform Market Overview by Component Type

- Saudi Arabian Cloud Management Platform Market Overview by Deployment Type

- Saudi Arabian Cloud Management Platform Market Overview by Company Type

- Saudi Arabian Cloud Management Platform Market Overview by Application

- Saudi Arabian Cloud Management Platform Market Overview by Industry Sector

- MOROCCO

- Moroccan Cloud Management Platform Market Overview by Component Type

- Moroccan Cloud Management Platform Market Overview by Deployment Type

- Moroccan Cloud Management Platform Market Overview by Company Type

- Moroccan Cloud Management Platform Market Overview by Application

- Moroccan Cloud Management Platform Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Cloud Management Platform Market Overview by Component Type

- Kuwaiti Cloud Management Platform Market Overview by Deployment Type

- Kuwaiti Cloud Management Platform Market Overview by Company Type

- Kuwaiti Cloud Management Platform Market Overview by Application

- Kuwaiti Cloud Management Platform Market Overview by Industry Sector

- QATAR

- Qatari Cloud Management Platform Market Overview by Component Type

- Qatari Cloud Management Platform Market Overview by Deployment Type

- Qatari Cloud Management Platform Market Overview by Company Type

- Qatari Cloud Management Platform Market Overview by Application

- Qatari Cloud Management Platform Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Cloud Management Platform Market Overview by Component Type

- Rest of Middle East & Africa Cloud Management Platform Market Overview by Deployment Type

- Rest of Middle East & Africa Cloud Management Platform Market Overview by Company Type

- Rest of Middle East & Africa Cloud Management Platform Market Overview by Application

- Rest of Middle East & Africa Cloud Management Platform Market Overview by Industry Sector

PART C: GUIDE TO THE INDUSTRY

- NORTH AMERICA

- EUROPE

- ASIA-PACIFIC

- REST OF WORLD

PART D: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

Amazon Web Services Inc.

Apptio Inc.

BMC Software Inc.

Cisco Systems Inc.

Citrix Systems Inc.

CloudBolt Software Inc.

CloudCheckr Inc.

CloudHealth Technologies Inc.

Cognizant (US)

Cohesity Inc.

CoreStack

Datadog(US)

Dell Technologies Inc.

Flexera Software LLC

Fugue Inc.

Google LLC

Hashi Corp

Hewlett Packard Enterprise Company

International Business Machines Corporation

LogicMonitor Inc.

MicroFocus (UK)

Microsoft Corporation

Morpheus Data

NetApp Inc.

New Relic Inc.

Nutanix Inc.

OpsRamp Inc.

ParkMyCloud Inc.

Platform9

Rapid7 LLC

Red Hat Inc.

Scality Inc.

ServiceNow Inc.

Snow Software (Sweden)

Splunk Inc.

Stratodesk Corporation

Turbonomic Inc.

VMware Inc.

Zenoss Inc.

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |