Finance and Accounting BPO Services - A Global Market Overview

- Published: Aug 2025

- Pages: 392 | Charts: 324

- Report Code: ITM133

SHARE THIS REPORT:

Global Finance and Accounting (F&A) BPO Services Market Trends and Outlook

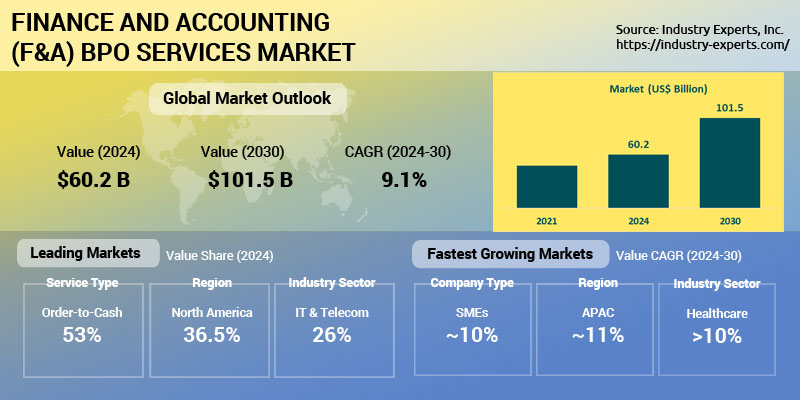

The global Finance and Accounting (F&A) BPO Services market is undergoing a significant transformation, marked by strong growth momentum and strategic reinvention. Valued at US$60.2 billion in 2024, the market is projected to reach US$101.5 billion by 2030, expanding at a CAGR of 9.1%. This expansion is fueled by intensifying cost pressures, acute finance talent shortages, and the urgent need for enterprises to digitally overhaul finance operations. Organizations are increasingly outsourcing transactional and compliance-intensive functions, such as accounts payable, record-to-report, and tax processing, to specialized BPO partners to boost efficiency, resilience, and agility.

The industry is rapidly shifting away from traditional labor arbitrage models toward outcome-based, digital-first engagements. Intelligent automation, AI-powered analytics, and predictive capabilities are now central to modern F&A BPO value propositions. Vendors are embedding technologies like intelligent document processing (IDP), anomaly detection, and real-time dashboards into their service offerings to deliver strategic insights rather than just operational support. Platform-based finance outsourcing models, which offer subscription-based, scalable, and integrated finance solutions, are becoming increasingly prevalent as enterprises demand end-to-end visibility, automation, and compliance assurance.

Finance and Accounting (F&A) BPO Services Regional Market Analysis

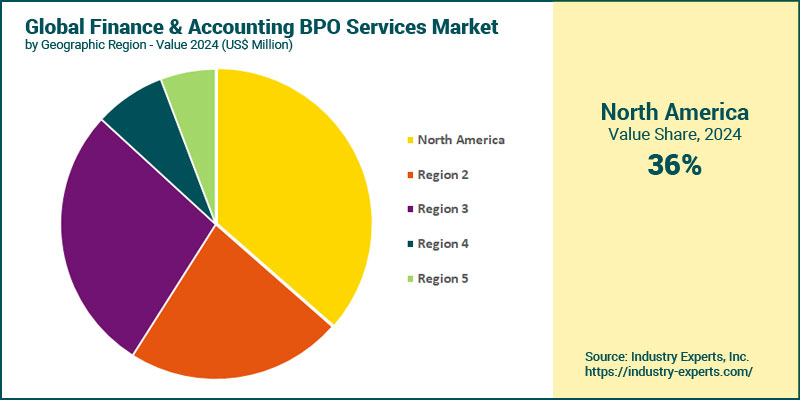

In 2024, North America holds the largest market share with an estimated 36.5% of global revenues. This dominance is attributed to early digital transformation, strong enterprise outsourcing maturity, and the concentration of leading vendors such as Genpact, Accenture, and Infosys BPM. Europe ranks second, supported by regulatory-driven finance modernization and cross-border compliance outsourcing. However, the fastest-growing regional market is Asia-Pacific, forecast to grow at a CAGR of 11.4%. This surge is driven by accelerated cloud ERP adoption, regional expansion of BPO delivery centers, and growing demand from mid-market enterprises and digital-native businesses. South America follows with a CAGR of 9.5%, supported by regulatory modernization, bilingual delivery capabilities, and rising finance talent shortages in developed economies.

Finance and Accounting (F&A) BPO Services Market Analysis by Service Type

Order-to-Cash (O2C) is the largest service segment, contributing around 53% of global market value. Its dominance is driven by enterprises' ongoing need to improve working capital, enhance collections, and automate receivables. The segment benefits from increasing adoption of AI-driven invoice processing, credit risk scoring, and customer experience tools. Source-to-Pay (S2P), which includes procurement and supplier management, is the fastest-growing segment, projected to expand at a CAGR of 11.8%. This growth is fueled by mounting supply chain risks, cost optimization needs, and the increasing use of platforms for spend visibility, contract analytics, and ESG-linked supplier compliance.

Finance and Accounting (F&A) BPO Services Market Analysis by Company Type

Large enterprises remain the dominant customer segment, which accounts for over 60% of total market value. Their sustained reliance on BPO stems from ongoing needs to streamline complex global operations, ensure regulatory compliance, and gain strategic visibility into finance performance. These firms are also leading adopters of platform-based outsourcing and end-to-end transformation engagements. However, small and medium-sized enterprises (SMEs) represent the fastest-growing segment, with a projected CAGR of 10.2%, reflecting broader access to automation tools, digital onboarding, and flexible service models. As vendors tailor verticalized and modular BPO offerings for mid-market customers, demand from this segment is expanding rapidly, especially in high-growth regions.

Finance and Accounting (F&A) BPO Services Market Analysis Industry Sector

In 2024, the IT & Telecom sector emerges as the largest vertical in the global Finance and Accounting BPO Services market, cornering 26.2% of total market value. Its dominance stems from the sector's high level of digital maturity, global operational complexity, and strong appetite for scalable, cloud-integrated finance platforms. The BFSI sector follows closely, supported by rising compliance burdens, risk management needs, and a high degree of outsourcing maturity. Meanwhile, Healthcare is the fastest-growing Industry Sector, projected to expand at a CAGR of 10.5% between 2024 and 2030, reaching US$10 billion by the end of the forecast period. Growth is propelled by increasing demand for revenue cycle management, claims processing automation, and regulatory reporting services-particularly in the wake of digitization efforts and talent shortages in finance roles across the healthcare ecosystem.

Finance and Accounting (F&A) BPO Services Market Report Scope

This global report on Finance and Accounting BPO Services market analyzes the global and regional market based on Service Type, Company Type, and Industry Sector for the period 2021-2030 with projection from 2024 to 2030 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Historical Period: | 2021-2024 | |

| Base Year: | 2024 | |

| Forecast Period: | 2024-2030 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 20+ |

Finance and Accounting BPO Services Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Finance and Accounting BPO Services Market by Service Type

- Order-to-Cash

- Source-to-Pay

- Procure-to-Pay

- Multi Processed

- Record-to-Report

Finance and Accounting BPO Services Market by Company Type

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

Finance and Accounting BPO Services Market Industry Sector

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

Finance and Accounting (F&A) BPO Services Market Frequently Asked Questions (FAQs)

The global Finance and Accounting (F&A) BPO Services market size is estimated at US$60.2 billion in 2024.

Global Finance and Accounting (F&A) BPO Services market is projected to reach US$101.5 billion by 2030, expanding at a CAGR of 9.1%.

In 2024, North America holds the largest market share with an estimated value of US$22 billion, representing roughly 36.5% of global revenues.

The fastest-growing regional market is Asia-Pacific, forecast to grow at a CAGR of 11.4% and reach US$32 billion by 2030.

Order-to-Cash (O2C) is the largest service segment, contributing around 53% of global market value.

Healthcare is the fastest-growing Industry Sector, projected to expand at a CAGR of 10.5% between 2024 and 2030, reaching US$10 billion by the end of the forecast period.

Leading players in the Finance and Accounting BPO Services industry include Accenture, Genpact, WNS, Capgemini, Infosys BPM, IBM, and TCS, known for their global delivery models, digital finance platforms, and deep domain expertise. These firms are at the forefront of integrating AI, automation, and analytics to deliver high-value, outcome-driven finance transformation services.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Finance and Accounting BPO Services

- Market Segmentation for Finance and Accounting BPO Services

- Service Types

- Company Types

- Applications

- Key Trends in Finance and Accounting BPO Services Market

2. INDUSTRY LANDSCAPE

- Global Finance and Accounting BPO Services Market Outlook

- Comprehensive Finance and Accounting BPO Services Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Finance and Accounting BPO Services Industry

- Startup Strategies for Finance and Accounting BPO Services Industry

- SWOT Analysis of Finance and Accounting BPO Services Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Finance and Accounting BPO Services Companies

- Market Share Analysis of Finance and Accounting BPO Services Companies

- SWOT Analysis of Key Players in the Finance and Accounting BPO Services Industry

- Key Market Players

- Accenture plc

- Capgemini

- CKH Group

- Cognizant

- Concentrix Corp.

- Deloitte Touche Tohmatsu Ltd.

- ExlService Holdings Inc.

- Fiserv, Inc.

- Genpact

- HCL Technologies Limited

- Infosys Limited

- International Business Machines (IBM) Corporation

- Invensis Technologies Pvt Ltd

- NTT DATA Corp.

- Oracle Corp.

- Outsourced Bookkeeping

- Sutherland

- Tata Consultancy Services (TCS) Limited

- Tech Mahindra Ltd.

- Teleperformance SE

- Wipro Limited

- WNS Holdings Ltd.

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Finance and Accounting BPO Services Market Overview by Service Type

- Finance and Accounting BPO Services Type Market Overview by Global Region

- Order-to-Cash

- Source-to-Pay

- Procure-to-Pay

- Multi Processed

- Record-to-Report

- Global Finance and Accounting BPO Services Market Overview by Company Type

- Finance and Accounting BPO Services Company Type Market Overview by Global Region

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

- Global Finance and Accounting BPO Services Market Overview Industry Sector

- Finance and Accounting BPO Services Application Market Overview by Global Region

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

PART B: REGIONAL MARKET PERSPECTIVE

- Global Finance and Accounting BPO Services Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Finance and Accounting BPO Services Market Overview by Geographic Region

- North American Finance and Accounting BPO Services Market Overview by Service Type

- North American Finance and Accounting BPO Services Market Overview by Company Type

- North American Finance and Accounting BPO Services Market Overview Industry Sector

- Country-wise Analysis of North American Finance and Accounting BPO Services Market

- THE UNITED STATES

- United States Finance and Accounting BPO Services Market Overview by Service Type

- United States Finance and Accounting BPO Services Market Overview by Company Type

- United States Finance and Accounting BPO Services Market Overview Industry Sector

- CANADA

- Canadian Finance and Accounting BPO Services Market Overview by Service Type

- Canadian Finance and Accounting BPO Services Market Overview by Company Type

- Canadian Finance and Accounting BPO Services Market Overview Industry Sector

- MEXICO

- Mexican Finance and Accounting BPO Services Market Overview by Service Type

- Mexican Finance and Accounting BPO Services Market Overview by Company Type

- Mexican Finance and Accounting BPO Services Market Overview Industry Sector

7. EUROPE

- European Finance and Accounting BPO Services Market Overview by Geographic Region

- European Finance and Accounting BPO Services Market Overview by Service Type

- European Finance and Accounting BPO Services Market Overview by Company Type

- European Finance and Accounting BPO Services Market Overview Industry Sector

- Country-wise Analysis of European Finance and Accounting BPO Services Market

- GERMANY

- German Finance and Accounting BPO Services Market Overview by Service Type

- German Finance and Accounting BPO Services Market Overview by Company Type

- German Finance and Accounting BPO Services Market Overview Industry Sector

- THE UNITED KINGDOM

- United Kingdom Finance and Accounting BPO Services Market Overview by Service Type

- United Kingdom Finance and Accounting BPO Services Market Overview by Company Type

- United Kingdom Finance and Accounting BPO Services Market Overview Industry Sector

- FRANCE

- French Finance and Accounting BPO Services Market Overview by Service Type

- French Finance and Accounting BPO Services Market Overview by Company Type

- French Finance and Accounting BPO Services Market Overview Industry Sector

- ITALY

- Italian Finance and Accounting BPO Services Market Overview by Service Type

- Italian Finance and Accounting BPO Services Market Overview by Company Type

- Italian Finance and Accounting BPO Services Market Overview Industry Sector

- THE NETHERLANDS

- Dutch Finance and Accounting BPO Services Market Overview by Service Type

- Dutch Finance and Accounting BPO Services Market Overview by Company Type

- Dutch Finance and Accounting BPO Services Market Overview Industry Sector

- SPAIN

- Spanish Finance and Accounting BPO Services Market Overview by Service Type

- Spanish Finance and Accounting BPO Services Market Overview by Company Type

- Spanish Finance and Accounting BPO Services Market Overview Industry Sector

- RUSSIA

- Russian Finance and Accounting BPO Services Market Overview by Service Type

- Russian Finance and Accounting BPO Services Market Overview by Company Type

- Russian Finance and Accounting BPO Services Market Overview Industry Sector

- SWITZERLAND

- Swiss Finance and Accounting BPO Services Market Overview by Service Type

- Swiss Finance and Accounting BPO Services Market Overview by Company Type

- Swiss Finance and Accounting BPO Services Market Overview Industry Sector

- REST OF EUROPE

- Rest of Europe Finance and Accounting BPO Services Market Overview by Service Type

- Rest of Europe Finance and Accounting BPO Services Market Overview by Company Type

- Rest of Europe Finance and Accounting BPO Services Market Overview Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Finance and Accounting BPO Services Market Overview by Geographic Region

- Asia-Pacific Finance and Accounting BPO Services Market Overview by Service Type

- Asia-Pacific Finance and Accounting BPO Services Market Overview by Company Type

- Asia-Pacific Finance and Accounting BPO Services Market Overview Industry Sector

- Country-wise Analysis of Asia-Pacific Finance and Accounting BPO Services Market

- CHINA

- Chinese Finance and Accounting BPO Services Market Overview by Service Type

- Chinese Finance and Accounting BPO Services Market Overview by Company Type

- Chinese Finance and Accounting BPO Services Market Overview Industry Sector

- JAPAN

- Japanese Finance and Accounting BPO Services Market Overview by Service Type

- Japanese Finance and Accounting BPO Services Market Overview by Company Type

- Japanese Finance and Accounting BPO Services Market Overview Industry Sector

- INDIA

- Indian Finance and Accounting BPO Services Market Overview by Service Type

- Indian Finance and Accounting BPO Services Market Overview by Company Type

- Indian Finance and Accounting BPO Services Market Overview Industry Sector

- AUSTRALIA

- Australia Finance and Accounting BPO Services Market Overview by Service Type

- Australia Finance and Accounting BPO Services Market Overview by Company Type

- Australia Finance and Accounting BPO Services Market Overview Industry Sector

- SINGAPORE

- Singaporean Finance and Accounting BPO Services Market Overview by Service Type

- Singaporean Finance and Accounting BPO Services Market Overview by Company Type

- Singaporean Finance and Accounting BPO Services Market Overview Industry Sector

- SOUTH KOREA

- South Korean Finance and Accounting BPO Services Market Overview by Service Type

- South Korean Finance and Accounting BPO Services Market Overview by Company Type

- South Korean Finance and Accounting BPO Services Market Overview Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Finance and Accounting BPO Services Market Overview by Service Type

- Rest of Asia-Pacific Finance and Accounting BPO Services Market Overview by Company Type

- Rest of Asia-Pacific Finance and Accounting BPO Services Market Overview Industry Sector

9. SOUTH AMERICA

- South American Finance and Accounting BPO Services Market Overview by Geographic Region

- South American Finance and Accounting BPO Services Market Overview by Service Type

- South American Finance and Accounting BPO Services Market Overview by Company Type

- South American Finance and Accounting BPO Services Market Overview Industry Sector

- Country-wise Analysis of South American Finance and Accounting BPO Services Market

- BRAZIL

- Brazilian Finance and Accounting BPO Services Market Overview by Service Type

- Brazilian Finance and Accounting BPO Services Market Overview by Company Type

- Brazilian Finance and Accounting BPO Services Market Overview Industry Sector

- ARGENTINA

- Argentine Finance and Accounting BPO Services Market Overview by Service Type

- Argentine Finance and Accounting BPO Services Market Overview by Company Type

- Argentine Finance and Accounting BPO Services Market Overview Industry Sector

- COLOMBIA

- Colombian Finance and Accounting BPO Services Market Overview by Service Type

- Colombian Finance and Accounting BPO Services Market Overview by Company Type

- Colombian Finance and Accounting BPO Services Market Overview Industry Sector

- CHILE

- Chilean Finance and Accounting BPO Services Market Overview by Service Type

- Chilean Finance and Accounting BPO Services Market Overview by Company Type

- Chilean Finance and Accounting BPO Services Market Overview Industry Sector

- PERU

- Peruvian Finance and Accounting BPO Services Market Overview by Service Type

- Peruvian Finance and Accounting BPO Services Market Overview by Company Type

- Peruvian Finance and Accounting BPO Services Market Overview Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Finance and Accounting BPO Services Market Overview by Service Type

- Rest of South America Finance and Accounting BPO Services Market Overview by Company Type

- Rest of South America Finance and Accounting BPO Services Market Overview Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Finance and Accounting BPO Services Market Overview by Geographic Region

- Middle East & Africa Finance and Accounting BPO Services Market Overview by Service Type

- Middle East & Africa Finance and Accounting BPO Services Market Overview by Company Type

- Middle East & Africa Finance and Accounting BPO Services Market Overview Industry Sector

- Country-wise Analysis of Middle East & Africa Finance and Accounting BPO Services Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Finance and Accounting BPO Services Market Overview by Service Type

- United Arab Emirates Finance and Accounting BPO Services Market Overview by Company Type

- United Arab Emirates Finance and Accounting BPO Services Market Overview Industry Sector

- SOUTH AFRICA

- South African Finance and Accounting BPO Services Market Overview by Service Type

- South African Finance and Accounting BPO Services Market Overview by Company Type

- South African Finance and Accounting BPO Services Market Overview Industry Sector

- EGYPT

- Egyptian Finance and Accounting BPO Services Market Overview by Service Type

- Egyptian Finance and Accounting BPO Services Market Overview by Company Type

- Egyptian Finance and Accounting BPO Services Market Overview Industry Sector

- SAUDI ARABIA

- Saudi Arabian Finance and Accounting BPO Services Market Overview by Service Type

- Saudi Arabian Finance and Accounting BPO Services Market Overview by Company Type

- Saudi Arabian Finance and Accounting BPO Services Market Overview Industry Sector

- MOROCCO

- Moroccan Finance and Accounting BPO Services Market Overview by Service Type

- Moroccan Finance and Accounting BPO Services Market Overview by Company Type

- Moroccan Finance and Accounting BPO Services Market Overview Industry Sector

- KUWAIT

- Kuwaiti Finance and Accounting BPO Services Market Overview by Service Type

- Kuwaiti Finance and Accounting BPO Services Market Overview by Company Type

- Kuwaiti Finance and Accounting BPO Services Market Overview Industry Sector

- QATAR

- Qatari Finance and Accounting BPO Services Market Overview by Service Type

- Qatari Finance and Accounting BPO Services Market Overview by Company Type

- Qatari Finance and Accounting BPO Services Market Overview Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Finance and Accounting BPO Services Market Overview by Service Type

- Rest of Middle East & Africa Finance and Accounting BPO Services Market Overview by Company Type

- Rest of Middle East & Africa Finance and Accounting BPO Services Market Overview Industry Sector

PART C: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

Accenture plc

Capgemini

CKH Group

Cognizant

Concentrix Corp.

Deloitte Touche Tohmatsu Ltd.

ExlService Holdings Inc.

Fiserv, Inc.

Genpact

HCL Technologies Limited

Infosys Limited

International Business Machines (IBM) Corporation

Invensis Technologies Pvt Ltd

NTT DATA Corp.

Oracle Corp.

Outsourced Bookkeeping

Sutherland

Tata Consultancy Services (TCS) Limited

Tech Mahindra Ltd.

Teleperformance SE

Wipro Limited

WNS Holdings Ltd.

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |