Endpoint Security Platforms - A Global Market Overview

- Published: Aug 2025

- Pages: 493 | Charts: 407

- Report Code: ITM011

SHARE THIS REPORT:

Global Endpoint Security Platforms Market Trends and Outlook

The global Endpoint Security Platforms market is undergoing a strategic transformation, with total revenues expected to rise from US$15.8 billion in 2024 to US$23.9 billion by 2030, registering a robust CAGR of 7.2% during the forecast period. This growth reflects the escalating urgency among enterprises to defend against increasingly complex and persistent cyber threats in an era of distributed workforces, expanded digital footprints, and growing regulatory demands. No longer limited to antivirus or traditional protection, endpoint security is now at the core of enterprise cyber defence strategies, driven by unified platforms that blend prevention, detection, and automated response across all device types.

Key trends shaping the market include the rapid adoption of cloud-native architectures, AI-powered threat detection, and the rise of extended detection and response (XDR) capabilities that integrate endpoint data with telemetry from networks, cloud workloads, and identity platforms. As ransomware, credential abuse, and supply chain attacks intensify, organisations are moving away from siloed tools toward integrated security ecosystems. The convergence of endpoint protection with identity access control, patch management, and device posture assessment is creating new benchmarks for endpoint visibility and resilience. Meanwhile, the demand for simplified management, modular pricing, and zero-touch deployments is influencing product design, especially among mid-sized enterprises and resource-constrained IT teams. As a result, endpoint security is no longer a tactical investment but a foundational pillar in enterprise risk and compliance frameworks.

Leading players in the Endpoint Security Platforms market include Microsoft, CrowdStrike, Broadcom (Symantec), SentinelOne, and Trend Micro, all of whom offer AI-driven, cloud-native, and XDR-integrated solutions. Other notable vendors such as Sophos, Bitdefender, and ESET are gaining traction in the mid-market through modular offerings and managed detection services.

Endpoint Security Platforms Regional Market Analysis

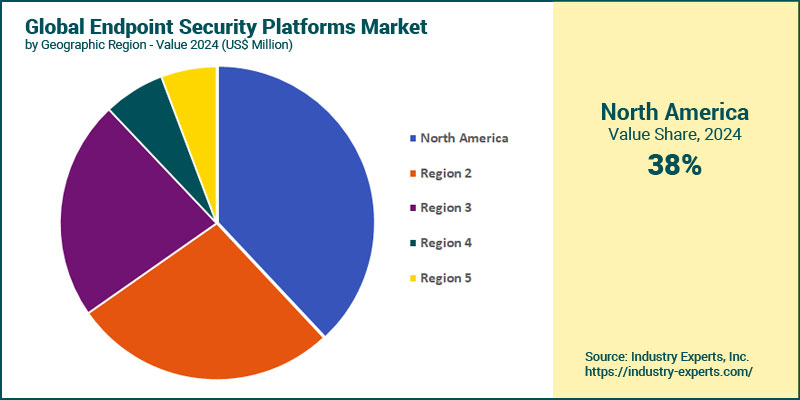

North America remains the largest regional market for endpoint security platforms, contributing approximately 38% of global revenues in 2024. By 2030, the region is expected to reach US$8.6 billion. This dominance is primarily driven by mature cybersecurity frameworks, a high density of hybrid and remote work environments, and strict regulatory mandates such as HIPAA, CCPA, and emerging federal zero-trust architecture requirements. The presence of leading vendors like Microsoft, CrowdStrike, and SentinelOne also reinforces strong enterprise adoption in sectors like healthcare, financial services, and government. Asia-Pacific emerges as the fastest-growing region, projected to expand at a CAGR of 9.2% during 2024-2030, attributed to escalating ransomware incidents, especially in industrial sectors, and growing cybersecurity investments across China, India, and Southeast Asia. As digitisation accelerates and critical infrastructure becomes more connected, demand for integrated endpoint detection, response, and management solutions is rising sharply. Vendors offering modular, cloud-native, and AI-integrated platforms are especially well-positioned to capture this demand in cost-sensitive but high-growth economies.

Endpoint Security Platforms Market Analysis by Endpoint Type

Mobile devices represent the largest endpoint type, accounting for roughly 28.2% of the total market in 2024. Their share is expected to climb further as the category grows to US$7.2 billion by 2030, registering a CAGR of 8.2% during 2024-2030. This leadership is fueled by the rise of remote work, BYOD policies, and the growing use of smartphones and tablets as enterprise productivity tools. The surge in mobile-targeted malware, SMS phishing, and application-level exploits has compelled organizations to prioritize mobile threat defense as a core part of endpoint security strategy. Point-of-sale (POS) terminals emerge as the second-fastest-growing endpoint type, with a CAGR of 7.7%, closely following mobile devices. Growth is being driven by the retail, hospitality, and foodservice sectors, where POS systems are increasingly cloud-connected and vulnerable to targeted intrusions, ransomware, and skimming attacks.

Endpoint Security Platforms Market Analysis by Deployment Type

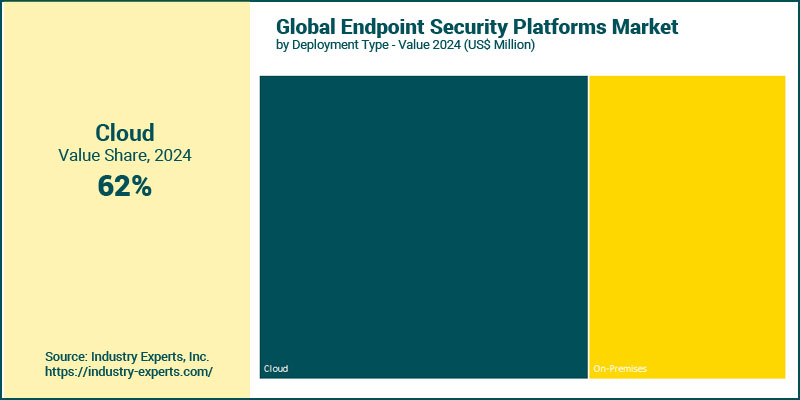

Cloud-based deployments account for the largest share of the endpoint security platforms market, contributing 62.5% share in 2024 and expected to grow to US$15.3 billion by 2030, registering a faster CAGR of 7.5% during 2024-2030. This dominant position is a direct result of the growing demand for agility, scalability, and remote manageability, especially in hybrid and remote-first work environments. Enterprises are favoring cloud-native endpoint protection and detection systems to enable seamless updates, real-time analytics, and centralized policy enforcement across globally dispersed users and devices. On-premises deployments, while growing at a slower CAGR of 6.6%, still constitute a significant market segment. This mode of deployment remains relevant in highly regulated sectors such as defense, healthcare, and finance, where data residency, internal compliance controls, and integration with legacy infrastructure continue to shape security architecture decisions.

Endpoint Security Platforms Market Analysis by Company Type

Large enterprises constitute the dominant customer segment, generating around 56.7% of revenues in 2024. These organizations typically operate complex IT environments with high-value assets and broad attack surfaces, necessitating advanced EDR/XDR capabilities, AI-powered analytics, and integrated identity protection. Regulatory compliance, incident response maturity, and proactive threat hunting further reinforce the need for enterprise-grade solutions, often within multi-vendor security ecosystems. Small and mid-sized enterprises (SMEs), while smaller in 2024, are expected to grow faster at a CAGR of 7.6%. This segment's accelerated growth is being fueled by rising awareness of cyber risks, increased targeting by ransomware groups, and the growing availability of simplified, cost-effective endpoint security offerings tailored to resource-constrained IT teams.

Endpoint Security Platforms Market Analysis by Industry Sector

BFSI (Banking, Financial Services, and Insurance) stands out as the largest industry segment, cornering around 21% share in 2024. With rising cyberattacks targeting financial data, digital banking platforms, and remote financial advisors, BFSI organizations are heavily investing in integrated endpoint protection and EDR/XDR solutions to secure distributed assets. Healthcare is the fastest-growing industry segment, expanding at a CAGR of 9% between 2024 and 2030. The surge in connected medical devices, telehealth services, and ransomware attacks targeting hospitals and clinical systems has pushed healthcare organizations to prioritize endpoint resilience. Solutions featuring zero-trust enforcement, device inventory visibility, and HIPAA-aligned audit capabilities are seeing rapid adoption, particularly in North America and Europe.

Endpoint Security Platforms Market Report Scope

This global report on Endpoint Security Platforms market analyzes the global and regional markets based on Endpoint Type, Deployment Type, Company Type, and Industry Sector for the period 2021-2030 with projections from 2024 to 2030 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Historical Period: | 2021-2024 | |

| Base Year: | 2024 | |

| Forecast Period: | 2024-2030 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 30+ |

Endpoint Security Platforms Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Endpoint Security Platforms Market by Endpoint Type

- Mobile Devices

- Workstations

- Servers

- Point of Sale Terminals

- Other Endpoint Types

Endpoint Security Platforms Market by Deployment Type

- Cloud

- On-Premises

Endpoint Security Platforms Market by Company Type

- Large Enterprises

- Small-to-medium Enterprises (SMEs)

Endpoint Security Platforms Market by Industry Sector

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

Endpoint Security Platforms Market Frequently Asked Questions (FAQs)

As of 2024, the global Endpoint Security Platforms market is valued at US$15.8 billion, driven by increasing cyber threats, hybrid workforce expansion, and regulatory mandates for endpoint protection.

The market is projected to grow at a CAGR of 7.2% between 2024 and 2030, reaching US$23.9 billion by 2030, supported by the convergence of EPP, EDR, and XDR technologies and the shift toward AI-driven, cloud-native security models.

North America is the largest regional market, accounting for nearly 38% of global revenues in 2024, fueled by strict compliance frameworks, a mature cybersecurity ecosystem, and high enterprise adoption rates.

Asia-Pacific is the fastest-growing region, expanding at a CAGR of 9.2% through 2030, due to rising ransomware threats, increasing digitization, and rapid adoption of cloud-based security in countries like China, India, and Southeast Asia.

Key technology trends include cloud-native architectures, AI/ML-powered threat detection, zero-trust integration, and extended detection and response (XDR) platforms that provide unified threat visibility across endpoints, cloud, and identity systems.

Top vendors include Microsoft, CrowdStrike, Broadcom (Symantec), SentinelOne, and Trend Micro, with others like Sophos, Bitdefender, and ESET gaining traction in mid-market and managed security services segments.

Major drivers include the surge in ransomware and supply chain attacks, workforce decentralization, regulatory compliance pressure, and the demand for unified, scalable platforms that reduce operational complexity for security teams.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Endpoint Security Platforms

- Market Segmentation for Endpoint Security Platforms

- Endpoint Types

- Deployment Types

- Company Types

- Industry Sectors

- Key Trends in Endpoint Security Platforms Market

2. INDUSTRY LANDSCAPE

- Global Endpoint Security Platforms Market Outlook

- Comprehensive Endpoint Security Platforms Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Endpoint Security Platforms Industry

- Startup Strategies for Endpoint Security Platforms Industry

- SWOT Analysis of Endpoint Security Platforms Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Endpoint Security Platforms Companies

- Market Share Analysis of Endpoint Security Platforms Companies

- SWOT Analysis of Key Players in the Endpoint Security Platforms Industry

- Key Market Players

- Acronis

- AO Kaspersky Lab

- Bitdefender

- BlackBerry Limited

- Check Point Software Technologies

- Cisco Systems Inc.

- Comodo Security Solutions Inc.

- Coro

- CrowdStrike

- Cybereason Inc.

- Cynet

- Deep Instinct

- Elastic Security

- ESET spol. s r.o.

- FireEye Inc.

- Forcepoint LLC

- Fortinet

- F-Secure

- IBM Corporation

- Malwarebytes

- McAfee LLC

- Microsoft Corporation

- Morphisec

- Palo Alto Networks

- Panda Security (WatchGuard)

- SentinelOne

- Seqrite (Quick Heal)

- Sophos Group plc

- Symantec Corporation (Broadcom)

- Trellix

- Trend Micro Incorporated

- Vipre Security

- VMware

- Xcitium (formerly Comodo)

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Endpoint Security Platforms Market Overview by Endpoint Type

- Endpoint Security Platforms Endpoint Type Market Overview by Global Region

- Mobile Devices

- Workstations

- Servers

- Point of Sale Terminals

- Other Endpoint Types

- Global Endpoint Security Platforms Market Overview by Deployment Type

- Endpoint Security Platforms Deployment Type Market Overview by Global Region

- Cloud

- On-Premises

- Global Endpoint Security Platforms Market Overview by Company Type

- Endpoint Security Platforms Company Type Market Overview by Global Region

- Large Enterprises

- Small-to-medium Enterprises (SMEs)

- Global Endpoint Security Platforms Market Overview by Industry Sector

- Endpoint Security Platforms Industry Sector Market Overview by Global Region

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

PART B: REGIONAL MARKET PERSPECTIVE

- Global Endpoint Security Platforms Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Endpoint Security Platforms Market Overview by Geographic Region

- North American Endpoint Security Platforms Market Overview by Endpoint Type

- North American Endpoint Security Platforms Market Overview by Deployment Type

- North American Endpoint Security Platforms Market Overview by Company Type

- North American Endpoint Security Platforms Market Overview by Industry Sector

- Country-wise Analysis of North American Endpoint Security Platforms Market

- THE UNITED STATES

- United States Endpoint Security Platforms Market Overview by Endpoint Type

- United States Endpoint Security Platforms Market Overview by Deployment Type

- United States Endpoint Security Platforms Market Overview by Company Type

- United States Endpoint Security Platforms Market Overview by Industry Sector

- CANADA

- Canadian Endpoint Security Platforms Market Overview by Endpoint Type

- Canadian Endpoint Security Platforms Market Overview by Deployment Type

- Canadian Endpoint Security Platforms Market Overview by Company Type

- Canadian Endpoint Security Platforms Market Overview by Industry Sector

- MEXICO

- Mexican Endpoint Security Platforms Market Overview by Endpoint Type

- Mexican Endpoint Security Platforms Market Overview by Deployment Type

- Mexican Endpoint Security Platforms Market Overview by Company Type

- Mexican Endpoint Security Platforms Market Overview by Industry Sector

7. EUROPE

- European Endpoint Security Platforms Market Overview by Geographic Region

- European Endpoint Security Platforms Market Overview by Endpoint Type

- European Endpoint Security Platforms Market Overview by Deployment Type

- European Endpoint Security Platforms Market Overview by Company Type

- European Endpoint Security Platforms Market Overview by Industry Sector

- Country-wise Analysis of European Endpoint Security Platforms Market

- GERMANY

- German Endpoint Security Platforms Market Overview by Endpoint Type

- German Endpoint Security Platforms Market Overview by Deployment Type

- German Endpoint Security Platforms Market Overview by Company Type

- German Endpoint Security Platforms Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Endpoint Security Platforms Market Overview by Endpoint Type

- United Kingdom Endpoint Security Platforms Market Overview by Deployment Type

- United Kingdom Endpoint Security Platforms Market Overview by Company Type

- United Kingdom Endpoint Security Platforms Market Overview by Industry Sector

- FRANCE

- French Endpoint Security Platforms Market Overview by Endpoint Type

- French Endpoint Security Platforms Market Overview by Deployment Type

- French Endpoint Security Platforms Market Overview by Company Type

- French Endpoint Security Platforms Market Overview by Industry Sector

- ITALY

- Italian Endpoint Security Platforms Market Overview by Endpoint Type

- Italian Endpoint Security Platforms Market Overview by Deployment Type

- Italian Endpoint Security Platforms Market Overview by Company Type

- Italian Endpoint Security Platforms Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Endpoint Security Platforms Market Overview by Endpoint Type

- Dutch Endpoint Security Platforms Market Overview by Deployment Type

- Dutch Endpoint Security Platforms Market Overview by Company Type

- Dutch Endpoint Security Platforms Market Overview by Industry Sector

- SPAIN

- Spanish Endpoint Security Platforms Market Overview by Endpoint Type

- Spanish Endpoint Security Platforms Market Overview by Deployment Type

- Spanish Endpoint Security Platforms Market Overview by Company Type

- Spanish Endpoint Security Platforms Market Overview by Industry Sector

- RUSSIA

- Russian Endpoint Security Platforms Market Overview by Endpoint Type

- Russian Endpoint Security Platforms Market Overview by Deployment Type

- Russian Endpoint Security Platforms Market Overview by Company Type

- Russian Endpoint Security Platforms Market Overview by Industry Sector

- SWITZERLAND

- Swiss Endpoint Security Platforms Market Overview by Endpoint Type

- Swiss Endpoint Security Platforms Market Overview by Deployment Type

- Swiss Endpoint Security Platforms Market Overview by Company Type

- Swiss Endpoint Security Platforms Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Endpoint Security Platforms Market Overview by Endpoint Type

- Rest of Europe Endpoint Security Platforms Market Overview by Deployment Type

- Rest of Europe Endpoint Security Platforms Market Overview by Company Type

- Rest of Europe Endpoint Security Platforms Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Endpoint Security Platforms Market Overview by Geographic Region

- Asia-Pacific Endpoint Security Platforms Market Overview by Endpoint Type

- Asia-Pacific Endpoint Security Platforms Market Overview by Deployment Type

- Asia-Pacific Endpoint Security Platforms Market Overview by Company Type

- Asia-Pacific Endpoint Security Platforms Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Endpoint Security Platforms Market

- CHINA

- Chinese Endpoint Security Platforms Market Overview by Endpoint Type

- Chinese Endpoint Security Platforms Market Overview by Deployment Type

- Chinese Endpoint Security Platforms Market Overview by Company Type

- Chinese Endpoint Security Platforms Market Overview by Industry Sector

- JAPAN

- Japanese Endpoint Security Platforms Market Overview by Endpoint Type

- Japanese Endpoint Security Platforms Market Overview by Deployment Type

- Japanese Endpoint Security Platforms Market Overview by Company Type

- Japanese Endpoint Security Platforms Market Overview by Industry Sector

- INDIA

- Indian Endpoint Security Platforms Market Overview by Endpoint Type

- Indian Endpoint Security Platforms Market Overview by Deployment Type

- Indian Endpoint Security Platforms Market Overview by Company Type

- Indian Endpoint Security Platforms Market Overview by Industry Sector

- AUSTRALIA

- Australia Endpoint Security Platforms Market Overview by Endpoint Type

- Australia Endpoint Security Platforms Market Overview by Deployment Type

- Australia Endpoint Security Platforms Market Overview by Company Type

- Australia Endpoint Security Platforms Market Overview by Industry Sector

- SINGAPORE

- Singaporean Endpoint Security Platforms Market Overview by Endpoint Type

- Singaporean Endpoint Security Platforms Market Overview by Deployment Type

- Singaporean Endpoint Security Platforms Market Overview by Company Type

- Singaporean Endpoint Security Platforms Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Endpoint Security Platforms Market Overview by Endpoint Type

- South Korean Endpoint Security Platforms Market Overview by Deployment Type

- South Korean Endpoint Security Platforms Market Overview by Company Type

- South Korean Endpoint Security Platforms Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Endpoint Security Platforms Market Overview by Endpoint Type

- Rest of Asia-Pacific Endpoint Security Platforms Market Overview by Deployment Type

- Rest of Asia-Pacific Endpoint Security Platforms Market Overview by Company Type

- Rest of Asia-Pacific Endpoint Security Platforms Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Endpoint Security Platforms Market Overview by Geographic Region

- South American Endpoint Security Platforms Market Overview by Endpoint Type

- South American Endpoint Security Platforms Market Overview by Deployment Type

- South American Endpoint Security Platforms Market Overview by Company Type

- South American Endpoint Security Platforms Market Overview by Industry Sector

- Country-wise Analysis of South American Endpoint Security Platforms Market

- BRAZIL

- Brazilian Endpoint Security Platforms Market Overview by Endpoint Type

- Brazilian Endpoint Security Platforms Market Overview by Deployment Type

- Brazilian Endpoint Security Platforms Market Overview by Company Type

- Brazilian Endpoint Security Platforms Market Overview by Industry Sector

- ARGENTINA

- Argentine Endpoint Security Platforms Market Overview by Endpoint Type

- Argentine Endpoint Security Platforms Market Overview by Deployment Type

- Argentine Endpoint Security Platforms Market Overview by Company Type

- Argentine Endpoint Security Platforms Market Overview by Industry Sector

- COLOMBIA

- Colombian Endpoint Security Platforms Market Overview by Endpoint Type

- Colombian Endpoint Security Platforms Market Overview by Deployment Type

- Colombian Endpoint Security Platforms Market Overview by Company Type

- Colombian Endpoint Security Platforms Market Overview by Industry Sector

- CHILE

- Chilean Endpoint Security Platforms Market Overview by Endpoint Type

- Chilean Endpoint Security Platforms Market Overview by Deployment Type

- Chilean Endpoint Security Platforms Market Overview by Company Type

- Chilean Endpoint Security Platforms Market Overview by Industry Sector

- PERU

- Peruvian Endpoint Security Platforms Market Overview by Endpoint Type

- Peruvian Endpoint Security Platforms Market Overview by Deployment Type

- Peruvian Endpoint Security Platforms Market Overview by Company Type

- Peruvian Endpoint Security Platforms Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Endpoint Security Platforms Market Overview by Endpoint Type

- Rest of South America Endpoint Security Platforms Market Overview by Deployment Type

- Rest of South America Endpoint Security Platforms Market Overview by Company Type

- Rest of South America Endpoint Security Platforms Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Endpoint Security Platforms Market Overview by Geographic Region

- Middle East & Africa Endpoint Security Platforms Market Overview by Endpoint Type

- Middle East & Africa Endpoint Security Platforms Market Overview by Deployment Type

- Middle East & Africa Endpoint Security Platforms Market Overview by Company Type

- Middle East & Africa Endpoint Security Platforms Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Endpoint Security Platforms Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Endpoint Security Platforms Market Overview by Endpoint Type

- United Arab Emirates Endpoint Security Platforms Market Overview by Deployment Type

- United Arab Emirates Endpoint Security Platforms Market Overview by Company Type

- United Arab Emirates Endpoint Security Platforms Market Overview by Industry Sector

- SOUTH AFRICA

- South African Endpoint Security Platforms Market Overview by Endpoint Type

- South African Endpoint Security Platforms Market Overview by Deployment Type

- South African Endpoint Security Platforms Market Overview by Company Type

- South African Endpoint Security Platforms Market Overview by Industry Sector

- EGYPT

- Egyptian Endpoint Security Platforms Market Overview by Endpoint Type

- Egyptian Endpoint Security Platforms Market Overview by Deployment Type

- Egyptian Endpoint Security Platforms Market Overview by Company Type

- Egyptian Endpoint Security Platforms Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Endpoint Security Platforms Market Overview by Endpoint Type

- Saudi Arabian Endpoint Security Platforms Market Overview by Deployment Type

- Saudi Arabian Endpoint Security Platforms Market Overview by Company Type

- Saudi Arabian Endpoint Security Platforms Market Overview by Industry Sector

- MOROCCO

- Moroccan Endpoint Security Platforms Market Overview by Endpoint Type

- Moroccan Endpoint Security Platforms Market Overview by Deployment Type

- Moroccan Endpoint Security Platforms Market Overview by Company Type

- Moroccan Endpoint Security Platforms Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Endpoint Security Platforms Market Overview by Endpoint Type

- Kuwaiti Endpoint Security Platforms Market Overview by Deployment Type

- Kuwaiti Endpoint Security Platforms Market Overview by Company Type

- Kuwaiti Endpoint Security Platforms Market Overview by Industry Sector

- QATAR

- Qatari Endpoint Security Platforms Market Overview by Endpoint Type

- Qatari Endpoint Security Platforms Market Overview by Deployment Type

- Qatari Endpoint Security Platforms Market Overview by Company Type

- Qatari Endpoint Security Platforms Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Endpoint Security Platforms Market Overview by Endpoint Type

- Rest of Middle East & Africa Endpoint Security Platforms Market Overview by Deployment Type

- Rest of Middle East & Africa Endpoint Security Platforms Market Overview by Company Type

- Rest of Middle East & Africa Endpoint Security Platforms Market Overview by Industry Sector

PART C: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

Acronis

AO Kaspersky Lab

Bitdefender

BlackBerry Limited

Check Point Software Technologies

Cisco Systems Inc.

Comodo Security Solutions Inc.

Coro

CrowdStrike

Cybereason Inc.

Cynet

Deep Instinct

Elastic Security

ESET spol. s r.o.

FireEye Inc.

Forcepoint LLC

Fortinet

F-Secure

IBM Corporation

Malwarebytes

McAfee LLC

Microsoft Corporation

Morphisec

Palo Alto Networks

Panda Security (WatchGuard)

SentinelOne

Seqrite (Quick Heal)

Sophos Group plc

Symantec Corporation (Broadcom)

Trellix

Trend Micro Incorporated

Vipre Security

VMware

Xcitium (formerly Comodo)

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |