Global Artificial Intelligence as a Service (AIaaS) Market - Components, Functional Offerings, Applications and Industry Sectors

- Published: Aug 2025

- Pages: 491 | Charts: 417

- Report Code: ITM138

SHARE THIS REPORT:

Global Artificial Intelligence as a Service (AIaaS) Market Trends and Outlook

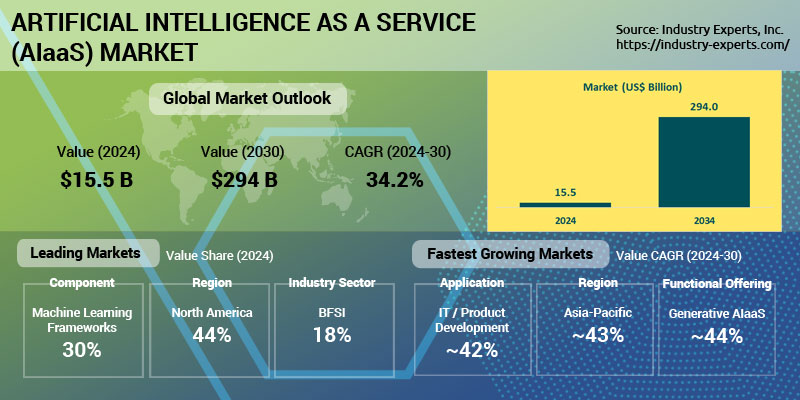

The global Artificial Intelligence as a Service (AIaaS) market is undergoing a transformative shift, fueled by rapid enterprise adoption, the proliferation of generative AI, and the convergence of cloud-native infrastructure with advanced machine learning capabilities. Valued at approximately US$15.5 billion in 2024, the market is projected to surpass US$294 billion by 2034, growing at a CAGR of 34.2%. This extraordinary expansion reflects rising demand for scalable, on-demand AI solutions that reduce time to value, lower implementation barriers, and empower organizations of all sizes to embed intelligence into operations, products, and customer experiences. AIaaS is evolving beyond isolated APIs toward integrated platforms offering end-to-end capabilities, from data prep and model training to deployment, monitoring, and governance.

One of the most disruptive forces shaping the market is generative AI, which is fundamentally redefining what AI-as-a-Service delivers. From marketing content generation and automated design to software development copilots and multimodal synthesis, generative AI is expanding AIaaS use cases across virtually every industry. Enterprises are increasingly embedding foundation models into workflows via APIs, accelerating adoption even among non-technical teams. This surge is accompanied by growing investment in vertical AI stacks tailored for regulated sectors such as healthcare and financial services, where explainability, compliance, and contextual accuracy are critical. Additionally, low-code/no-code AI platforms are democratizing access, empowering business users to deploy models without extensive coding expertise.

Artificial Intelligence as a Service (AIaaS) Regional Market Analysis

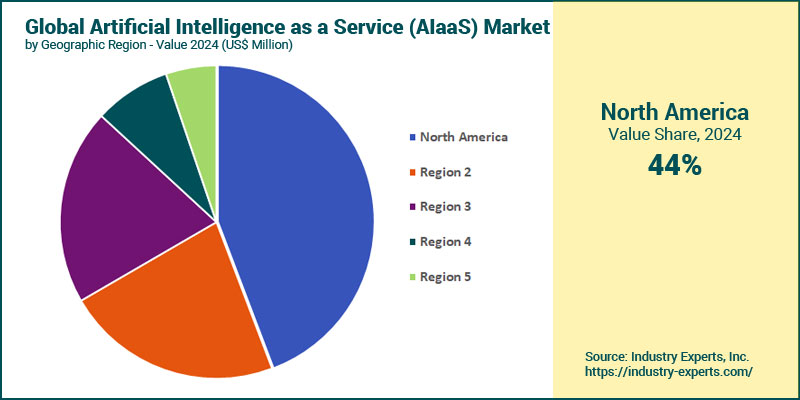

North America remains the largest regional market, contributing an estimated 44.2% of global AIaaS spending in 2024. This dominance is underpinned by early adoption of AI infrastructure, leadership in cloud services, and a strong presence of hyperscalers such as AWS, Microsoft Azure, Google Cloud, and IBM. North America is expected to grow at a CAGR of 28.7% between 2024 and 2034, driven by sustained enterprise demand for explainable AI, generative AI integration, and hybrid-cloud strategies. Asia-Pacific is the fastest-growing region, projected to register a CAGR of 43.1% over the outlook period. This exceptional pace is fueled by accelerating digitization across China, India, and Southeast Asia, government-led AI initiatives, and a booming ecosystem of regional cloud providers. High AIaaS adoption in sectors such as manufacturing, logistics, and public services, along with strong demand for low-code/no-code and vertical AI stacks, is reshaping the competitive dynamics in the region.

Artificial Intelligence as a Service (AIaaS) Market Analysis by Component

In 2024, Machine Learning Frameworks dominated the AIaaS market by component, contributing approximately 30% of total global revenue. Their prominence reflects their foundational role in enabling scalable model training, orchestration, and deployment across a variety of enterprise AI applications. These frameworks remain central to platform offerings from major cloud vendors and are heavily used in data science, finance, healthcare, and product development functions. However, a major shift is underway. By 2027, Chatbots & AI Agents are projected to overtake Machine Learning Frameworks to become the largest component segment, driven by rapid enterprise adoption of LLM-powered virtual assistants, AI copilots, and autonomous agents across marketing, customer service, HR, and internal productivity. The shift reflects the mainstreaming of conversational AI and the growing prioritization of user-facing, interactive AI capabilities within enterprise tech stacks. On the other side, the fastest growth is occurring in No-code/Low-code tools, which are democratizing AI access for non-technical users. This segment is expected to grow at a CAGR of 41.8%, as enterprises increasingly prioritize usability, speed to deployment, and integration flexibility across business units.

Artificial Intelligence as a Service (AIaaS) Market Analysis by Functional Offering

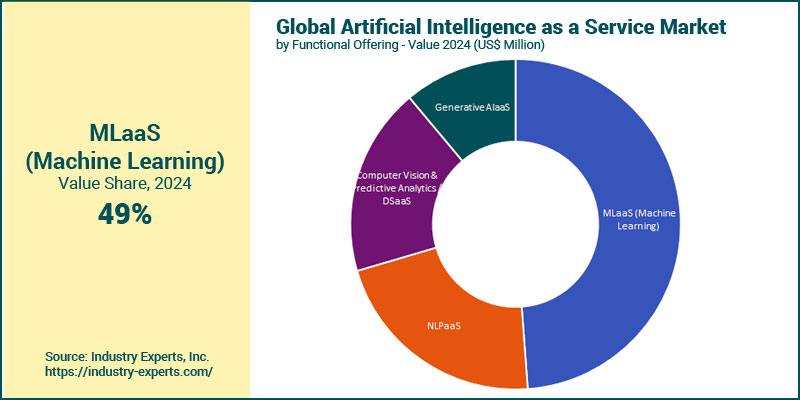

MLaaS (Machine Learning as a Service) is the largest functional segment, contributing roughly 48.8% of the global AIaaS market in 2024. MLaaS solutions - including model training, tuning, and monitoring - are widely adopted across finance, healthcare, and manufacturing, supported by mature platforms like AWS SageMaker, Azure ML, and Google Vertex AI. The segment is projected to grow at a CAGR of 29%, reaching US$96.2 billion by 2034, driven by enterprise-scale deployments and increasing reliance on real-time inference and autoML pipelines. Generative AIaaS is the fastest-growing functional offering, poised to post a CAGR of 43.8%. Fueled by APIs and services based on large foundation models (e.g., OpenAI, Gemini, Claude), this segment is transforming use cases in content creation, design, customer engagement, coding assistance, and knowledge automation. Enterprises are rapidly embedding generative AI into core workflows, while demand for customizable, explainable, and verticalized solutions is accelerating global adoption.

Artificial Intelligence as a Service (AIaaS) Market Analysis by Application

In 2024, Marketing & Sales held the largest share of the global AIaaS market by application, accounting for 20.9% of total revenue. Its lead reflects strong enterprise investment in AI-driven personalization, campaign optimization, lead scoring, and generative content creation. Close behind was IT/Product Development, with US$3 billion, driven by increasing use of AI in software delivery pipelines, infrastructure monitoring, and code generation. Looking ahead, IT/Product Development is expected to become the fastest-growing application area, registering a CAGR of 41.7% and reaching US$98 billion by 2034. This growth is powered by the widespread adoption of AI copilots, model lifecycle management tools, and integration of AI into DevOps workflows. Human Resources (HR) ranks as the second-fastest growing segment, expanding at a CAGR of 39.8%. Adoption is accelerating as enterprises deploy AI for recruitment, engagement analytics, workforce planning, and employee support, often through low-code interfaces and verticalized HR tech solutions.

Artificial Intelligence as a Service (AIaaS) Market Analysis by Industry Sector

BFSI (Banking, Financial Services, and Insurance) was the largest industry vertical in the global AIaaS market, contributing approximately 17.6% of total global revenue in 2024. This leadership stems from early AIaaS adoption in fraud detection, credit scoring, algorithmic trading, and regulatory compliance, with growing emphasis on explainability, auditability, and hybrid-cloud deployment in regulated environments. However, Healthcare is the fastest-growing sector, expanding at a CAGR of 41.1% over the outlook period. The surge is driven by demand for AI-powered diagnostics, clinical decision support, patient engagement tools, and privacy-preserving data analytics, alongside rising regulatory momentum for AI use in clinical workflows.

Artificial Intelligence as a Service (AIaaS) Market Report Scope

This global report on Artificial Intelligence as a Service (AIaaS) market analyzes the global and regional market based on Component, Functional Offering, Application, and Industry Sector for the period 2024-2034 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Base Year: | 2024 | |

| Forecast Period: | 2024-2034 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 25+ |

Artificial Intelligence as a Service (AIaaS) Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Artificial Intelligence as a Service (AIaaS) Market by Component

- Machine Learning Frameworks

- Chatbots & AI Agents

- APIs

- No?code / Low?code Tools

- Data Labeling & Pre?processing Tools

Artificial Intelligence as a Service (AIaaS) Market by Functional Offering

- MLaaS (Machine Learning)

- NLPaaS

- Computer Vision & Predictive Analytics / DSaaS

- Generative AIaaS

Artificial Intelligence as a Service (AIaaS) Market by Application

- Marketing & Sales

- IT / Product Development

- Customer Service

- Operations & Supply Chain

- Finance

- Human Resources (HR)

- Other Applications

Artificial Intelligence as a Service (AIaaS) Market by Industry Sector

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Retail

- Healthcare

- Manufacturing

- Public Sector

- Energy & Utilities

- Other End-Uses

Artificial Intelligence as a Service (AIaaS) Market Frequently Asked Questions (FAQs)

The global Artificial Intelligence as a Service (AIaaS) market is estimated at US$15.5 billion in 2024. The market has rebounded strongly following foundational model advancements and is gaining momentum as enterprises across industries adopt scalable AI solutions via cloud platforms.

Between 2024 and 2034, the AIaaS market is projected to grow at a CAGR of 34.2%, reaching over US$294 billion by 2034. This growth is driven by the convergence of generative AI, hybrid-cloud infrastructure, and increasing enterprise demand for cost-effective, low-barrier AI adoption.

In 2024, Machine Learning Frameworks hold the largest share, generating 30% of total market value. However, by 2027, Chatbots & AI Agents are expected to become the largest component segment as demand for LLM-powered virtual assistants and autonomous AI interfaces accelerates, particularly in customer engagement and productivity use cases.

Marketing & Sales is currently the largest application segment, followed closely by IT/Product Development (US$3 billion). However, IT/Product Development is the fastest-growing at a CAGR 41.7%, as enterprises increasingly deploy AI copilots, AutoML pipelines, and DevOps integration tools. HR is the second-fastest, growing at 39.8% CAGR.

BFSI is the leading vertical by revenue in 2024, reflecting advanced adoption of AI for fraud detection, compliance, and personalization. Meanwhile, Healthcare is the fastest-growing industry, with a CAGR of 41.1%, driven by the expansion of AI in diagnostics, patient care, and clinical decision-making.

Top trends include the rise of generative AI, expansion of low-code/no-code AI platforms, verticalized AI solutions for regulated industries, hybrid-cloud deployment, composable AI architectures, and increasing demand for explainable and ethical AI. Real-time inference, usage-based pricing, and privacy-preserving technologies are also reshaping vendor strategies.

The ecosystem is led by hyperscalers like AWS, Microsoft Azure, Google Cloud AI, and IBM Watson, alongside emerging players such as Hugging Face, Cohere, and Stability AI. These providers compete on platform breadth, domain-specific capabilities, pricing models, and trust features like bias mitigation and explainability.

Key barriers include integration with legacy systems, shortage of AI-literate talent, vendor lock-in, and compliance with evolving global regulations such as the EU AI Act. Organizations also face challenges around model transparency, security, and managing performance at scale-especially in mission-critical or regulated environments.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Artificial Intelligence as a Service (AIaaS)

- Market Segmentation for Artificial Intelligence as a Service (AIaaS)

- Components

- Functional Offerings

- Applications

- Industry Sectors

- Key Trends in Artificial Intelligence as a Service (AIaaS) Market

2. INDUSTRY LANDSCAPE

- Global Artificial Intelligence as a Service (AIaaS) Market Outlook

- Comprehensive Artificial Intelligence as a Service (AIaaS) Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Artificial Intelligence as a Service (AIaaS) Industry

- Startup Strategies for Artificial Intelligence as a Service (AIaaS) Industry

- SWOT Analysis of Artificial Intelligence as a Service (AIaaS) Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Artificial Intelligence as a Service (AIaaS) Companies

- Market Share Analysis of Artificial Intelligence as a Service (AIaaS) Companies

- SWOT Analysis of Key Players in the Artificial Intelligence as a Service (AIaaS) Industry

- Key Market Players

- Alibaba Cloud

- Altair

- Anyscale

- AWS

- BigML

- Cloudera

- Cohere

- Glean

- H20.ai

- HPE

- IBM

- Inflection Al

- Levity Al

- Microsoft

- Mistral Al

- NVIDIA

- OpenAl

- Oracle

- Salesforce

- SAP

- SAS Institute

- Scale Al

- ServiceNow

- Synthesia

- Yellow.ai

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Artificial Intelligence as a Service (AIaaS) Component Market Overview by Global Region

- Machine Learning Frameworks

- Chatbots & AI Agents

- APIs

- No?code / Low?code Tools

- Data Labeling & Pre?processing Tools

- Global Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Artificial Intelligence as a Service (AIaaS) Functional Offering Market Overview by Global Region

- MLaaS (Machine Learning)

- NLPaaS

- Computer Vision & Predictive Analytics / DSaaS

- Generative AIaaS

- Global Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Artificial Intelligence as a Service (AIaaS) Application Market Overview by Global Region

- Marketing & Sales

- IT / Product Development

- Customer Service

- Operations & Supply Chain

- Finance

- Human Resources (HR)

- Other Applications

- Global Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- Artificial Intelligence as a Service (AIaaS) Industry Sector Market Overview by Global Region

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Retail

- Healthcare

- Manufacturing

- Public Sector

- Energy & Utilities

- Other Industry Sectors

PART B: REGIONAL MARKET PERSPECTIVE

- Global Artificial Intelligence as a Service (AIaaS) Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Artificial Intelligence as a Service (AIaaS) Market Overview by Geographic Region

- North American Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- North American Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- North American Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- North American Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- Country-wise Analysis of North American Artificial Intelligence as a Service (AIaaS) Market

- THE UNITED STATES

- United States Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- United States Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- United States Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- United States Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- CANADA

- Canadian Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Canadian Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Canadian Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Canadian Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- MEXICO

- Mexican Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Mexican Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Mexican Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Mexican Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

7. EUROPE

- European Artificial Intelligence as a Service (AIaaS) Market Overview by Geographic Region

- European Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- European Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- European Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- European Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- Country-wise Analysis of European Artificial Intelligence as a Service (AIaaS) Market

- GERMANY

- German Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- German Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- German Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- German Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- United Kingdom Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- United Kingdom Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- United Kingdom Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- FRANCE

- French Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- French Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- French Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- French Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- ITALY

- Italian Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Italian Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Italian Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Italian Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Dutch Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Dutch Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Dutch Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- SPAIN

- Spanish Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Spanish Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Spanish Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Spanish Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- RUSSIA

- Russian Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Russian Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Russian Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Russian Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- SWITZERLAND

- Swiss Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Swiss Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Swiss Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Swiss Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Rest of Europe Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Rest of Europe Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Rest of Europe Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Artificial Intelligence as a Service (AIaaS) Market Overview by Geographic Region

- Asia-Pacific Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Asia-Pacific Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Asia-Pacific Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Asia-Pacific Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Artificial Intelligence as a Service (AIaaS) Market

- CHINA

- Chinese Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Chinese Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Chinese Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Chinese Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- JAPAN

- Japanese Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Japanese Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Japanese Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Japanese Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- INDIA

- Indian Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Indian Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Indian Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Indian Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- AUSTRALIA

- Australia Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Australia Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Australia Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Australia Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- SINGAPORE

- Singaporean Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Singaporean Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Singaporean Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Singaporean Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- South Korean Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- South Korean Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- South Korean Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Rest of Asia-Pacific Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Rest of Asia-Pacific Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Rest of Asia-Pacific Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Artificial Intelligence as a Service (AIaaS) Market Overview by Geographic Region

- South American Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- South American Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- South American Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- South American Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- Country-wise Analysis of South American Artificial Intelligence as a Service (AIaaS) Market

- BRAZIL

- Brazilian Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Brazilian Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Brazilian Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Brazilian Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- ARGENTINA

- Argentine Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Argentine Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Argentine Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Argentine Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- COLOMBIA

- Colombian Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Colombian Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Colombian Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Colombian Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- CHILE

- Chilean Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Chilean Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Chilean Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Chilean Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- PERU

- Peruvian Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Peruvian Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Peruvian Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Peruvian Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Rest of South America Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Rest of South America Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Rest of South America Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Artificial Intelligence as a Service (AIaaS) Market Overview by Geographic Region

- Middle East & Africa Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Middle East & Africa Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Middle East & Africa Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Middle East & Africa Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Artificial Intelligence as a Service (AIaaS) Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- United Arab Emirates Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- United Arab Emirates Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- United Arab Emirates Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- SOUTH AFRICA

- South African Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- South African Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- South African Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- South African Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- EGYPT

- Egyptian Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Egyptian Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Egyptian Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Egyptian Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Saudi Arabian Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Saudi Arabian Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Saudi Arabian Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- MOROCCO

- Moroccan Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Moroccan Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Moroccan Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Moroccan Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Kuwaiti Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Kuwaiti Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Kuwaiti Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- QATAR

- Qatari Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Qatari Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Qatari Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Qatari Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Artificial Intelligence as a Service (AIaaS) Market Overview by Component

- Rest of Middle East & Africa Artificial Intelligence as a Service (AIaaS) Market Overview by Functional Offering

- Rest of Middle East & Africa Artificial Intelligence as a Service (AIaaS) Market Overview by Application

- Rest of Middle East & Africa Artificial Intelligence as a Service (AIaaS) Market Overview by Industry Sector

PART C: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

Alibaba Cloud

Altair

Anyscale

AWS

BigML

Cloudera

Cohere

Glean

Google

H20.ai

HPE

IBM

Inflection Al

Levity Al

Microsoft

Mistral Al

NVIDIA

OpenAl

Oracle

Salesforce

SAP

SAS Institute

Scale Al

ServiceNow

Synthesia

Yellow.ai

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |