Global Application Delivery Controllers (ADCs) Market - Product Types, Company Types and Industry Sectors

- Published: Aug 2025

- Pages: 391 | Charts: 318

- Report Code: ITM070

SHARE THIS REPORT:

Global Application Delivery Controllers (ADCs) Market Trends and Outlook

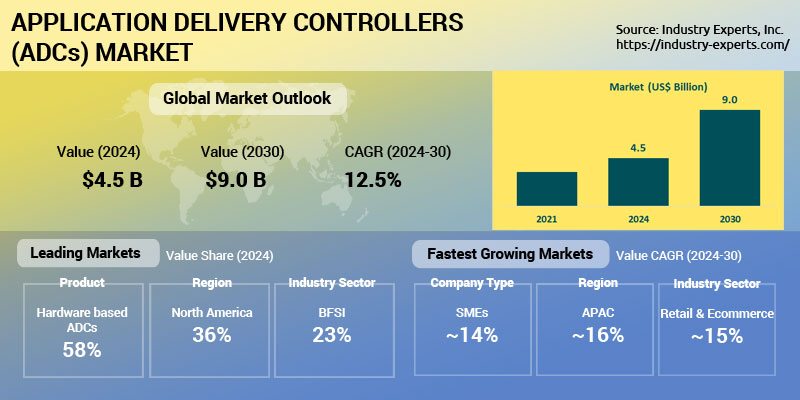

The global Application Delivery Controllers (ADCs) market is undergoing a rapid transformation, shaped by the convergence of digital acceleration, multi-cloud complexity, and heightened security demands. Valued at approximately US$4.5 billion in 2024, the market is projected to more than double by 2030, surpassing US$9 billion at a CAGR of 12.5%. Enterprises across sectors are prioritizing ADCs as strategic enablers for consistent, secure, and high-performance application delivery in hybrid and containerized environments. Increasing reliance on cloud-native architectures and the proliferation of API-driven ecosystems are fundamentally redefining the role of ADCs from traditional load balancers to intelligent, software-defined control points embedded in application infrastructure.

Security has emerged as a key growth catalyst, with integrated features such as Web Application Firewall (WAF), bot mitigation, API protection, and behavioral analytics becoming baseline expectations. This is further reinforced by regulatory frameworks like GDPR and industry-specific compliance mandates that require granular policy control and robust traffic visibility. Simultaneously, the shift toward automation and observability is reshaping operational expectations, as DevOps teams seek ADCs that offer declarative APIs, real-time telemetry, and seamless integration into monitoring and orchestration pipelines. Major players, including F5 Networks, Citrix Systems, Radware, Fortinet, and A10 Networks, are actively evolving their portfolios to address these new imperatives.

Application Delivery Controllers (ADCs) Regional Market Analysis

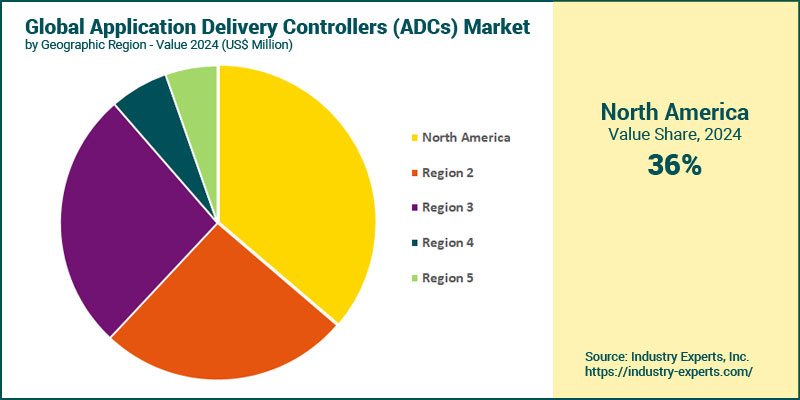

North America leads the global ADC market in 2024 with an estimated 36.3% share of total market revenue. The region benefits from early adoption of digital transformation strategies, a high concentration of cloud-native enterprises, and stringent data compliance mandates driving investment in advanced, security-integrated ADC platforms. Asia Pacific is the fastest-growing regional market, expanding at a CAGR of 15.7% to reach nearly US$2.8 billion by 2030. Growth is driven by hyperscale data center deployments, 5G and cloud expansion, and rising demand for scalable application infrastructure in countries like China, India, and Indonesia. The increasing need for cost-effective, virtualized ADC solutions among local enterprises is further fueling regional momentum.

Application Delivery Controllers (ADCs) Market Analysis by Product Type

In 2024, hardware-based ADCs hold the largest share at 58% of the global market. Their dominance is rooted in mission-critical use cases where performance, reliability, and compliance (e.g., FIPS 140-2) are non-negotiable, particularly in large enterprises, telecom, and financial services. However, virtual ADCs are the fastest-growing segment, projected to rise at a CAGR of 14.5%. Their ability to deliver elastic scalability, automation, and seamless integration with DevOps workflows is transforming ADC deployment from static appliances into agile, cloud-native platforms tailored for modern application delivery.

Application Delivery Controllers (ADCs) Market Analysis by Company Type

Large enterprises dominate the market in 2024 representing 62% of global ADC revenues. Their broad IT environments, complex application ecosystems, and demand for centralized policy enforcement make ADCs a critical component of their infrastructure modernization strategies. Conversely, small and medium-sized enterprises (SMEs) are emerging as the fastest-growing customer group, with a projected CAGR of 14.1% and market value expected to reach US$3.7 billion by 2030. The rise of simplified, SaaS-based ADC offerings and subscription licensing models is enabling SMEs to access enterprise-grade capabilities without the operational burden or capital expense traditionally associated with ADC deployments.

Application Delivery Controllers (ADCs) Market Analysis by Industry Sector

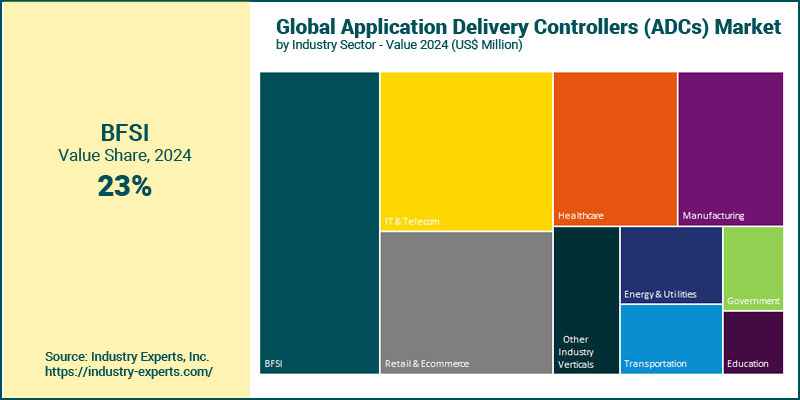

The Banking, Financial Services, and Insurance (BFSI) sector is the largest end-use industry for ADCs, accounting for 23% of total global market value. This dominance is maintained throughout the forecast period, with the segment projected to reach over US$2.0 billion by 2030. BFSI institutions rely heavily on ADCs for real-time application performance, encrypted transaction delivery, API gateway integration, and compliance with stringent cybersecurity frameworks such as PCI DSS and regional financial data protection laws. The fastest-growing vertical, however, is Retail & eCommerce, which is expected to expand at a CAGR of 15.3%. This growth is driven by the need to ensure always-on digital storefronts, secure checkout APIs, and frictionless omnichannel customer experiences, particularly during seasonal peaks and high-volume events. The rising use of WAF, bot mitigation, and application acceleration capabilities among digital retailers is accelerating ADC adoption in this sector. Other high-growth verticals include IT & Telecom (13.8% CAGR) and Healthcare (13.1% CAGR).

Application Delivery Controllers (ADCs) Market Report Scope

This global report on Application Delivery Controllers (ADCs) market analyzes the global and regional market based on Product Type, Company Type, and Industry Sector for the period 2021-2030 with projection from 2024 to 2030 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Key Metrics

| Historical Period: | 2021-2024 | |

| Base Year: | 2024 | |

| Forecast Period: | 2024-2030 | |

| Units: | Value market in US$ | |

| Companies Mentioned: | 25+ |

Application Delivery Controllers (ADCs) Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (the United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Application Delivery Controllers (ADCs) Market by Product Type

- Hardware based ADCs

- Virtual ADCs

Application Delivery Controllers (ADCs) Market by Company Type

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

Application Delivery Controllers (ADCs) Market by Industry Sector

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

Application Delivery Controllers (ADCs) Market Frequently Asked Questions (FAQs)

In 2024, the global Application Delivery Controllers (ADCs) market is valued at approximately US$4.5 billion.

Looking ahead to 2030, the ADCs market is expected to surpass US$9 billion, expanding at a healthy CAGR of 12.5% over the forecast period.

North America holds the largest share of the global ADC market, which accounts for 36.3% of total global revenue.

Asia Pacific is the fastest-growing regional market for Application Delivery Controllers, projected to expand at a CAGR of 15.7% from 2024 to 2030.

Hardware-based ADCs dominate the market in 2024 with an estimated 58% share of global revenue.

Banking, Financial Services, and Insurance (BFSI) sector is the largest end-use industry, accounting for 23% of total global ADC market value.

The top players in the Application Delivery Controllers (ADCs) market include F5, Inc., Citrix Systems, A10 Networks, Radware Ltd. and Fortinet, Inc.. Others leading players are Progress (Kemp), Array Networks, NGINX (open-source), and Barracuda serve SMEs and niche deployments.

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- A Roundup on Application Delivery Controllers (ADCs) Applications

- Market Segmentation for Application Delivery Controllers (ADCs)

- Product Types

- Company Types

- Industry Sectors

- Key Trends in Application Delivery Controllers (ADCs) Market

2. INDUSTRY LANDSCAPE

- Global Application Delivery Controllers (ADCs) Market Outlook

- Comprehensive Application Delivery Controllers (ADCs) Industry Analysis - Growth Drivers and Inhibitors

- Growth Drivers

- Growth Inhibitors

- Market Entry Strategies for Application Delivery Controllers (ADCs) Industry

- Startup Strategies for Application Delivery Controllers (ADCs) Industry

- SWOT Analysis of Application Delivery Controllers (ADCs) Industry

- Strengths

- Weaknesses

- Opportunities

- Threats

- Porter's Five Forces Analysis

- PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- Market Positioning of Key Application Delivery Controllers (ADCs) Companies

- Market Share Analysis of Application Delivery Controllers (ADCs) Companies

- SWOT Analysis of Key Players in the Application Delivery Controllers (ADCs) Industry

- Key Market Players

- A10 Networks

- Akamai Technologies Inc.

- Array Networks

- Barracuda Networks

- Broadcom Communication

- Cisco Systems

- Citrix Systems

- Cloudflare

- Dell Technologies

- EdgeNEXUS (JetNEXUS)

- Evanssion

- F5 Networks

- Fortinet

- HAProxy Technologies LLC

- Juniper Networks Inc.

- Kemp Technologies

- Loadbalancer.org Inc.

- NFWare

- Piolink Inc.

- Radware

- Riverbed

- Sangfor Technologies Inc.

- Snapt

- Total Uptime

- ZEVENET

4. KEY BUSINESS & PRODUCT TRENDS

5. GLOBAL MARKET OVERVIEW

- Global Application Delivery Controllers (ADCs) Market Overview by Product Type

- Application Delivery Controllers (ADCs) Product Type Market Overview by Global Region

- Offshore

- Onshore

- Nearshore

- Global Application Delivery Controllers (ADCs) Market Overview by Company Type

- Application Delivery Controllers (ADCs) Company Type Market Overview by Global Region

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

- Global Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- Application Delivery Controllers (ADCs) Industry Sector Market Overview by Global Region

- Banking, Financial Services, and Insurance (BFSI)

- IT & Telecom

- Manufacturing

- Government

- Healthcare

- Retail & Ecommerce

- Energy & Utilities

- Transportation

- Education

- Other Industry Sectors

PART B: REGIONAL MARKET PERSPECTIVE

- Global Application Delivery Controllers (ADCs) Market Overview by Geographic Region

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- North American Application Delivery Controllers (ADCs) Market Overview by Geographic Region

- North American Application Delivery Controllers (ADCs) Market Overview by Product Type

- North American Application Delivery Controllers (ADCs) Market Overview by Company Type

- North American Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- Country-wise Analysis of North American Application Delivery Controllers (ADCs) Market

- THE UNITED STATES

- United States Application Delivery Controllers (ADCs) Market Overview by Product Type

- United States Application Delivery Controllers (ADCs) Market Overview by Company Type

- United States Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- CANADA

- Canadian Application Delivery Controllers (ADCs) Market Overview by Product Type

- Canadian Application Delivery Controllers (ADCs) Market Overview by Company Type

- Canadian Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- MEXICO

- Mexican Application Delivery Controllers (ADCs) Market Overview by Product Type

- Mexican Application Delivery Controllers (ADCs) Market Overview by Company Type

- Mexican Application Delivery Controllers (ADCs) Market Overview by Industry Sector

7. EUROPE

- European Application Delivery Controllers (ADCs) Market Overview by Geographic Region

- European Application Delivery Controllers (ADCs) Market Overview by Product Type

- European Application Delivery Controllers (ADCs) Market Overview by Company Type

- European Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- Country-wise Analysis of European Application Delivery Controllers (ADCs) Market

- GERMANY

- German Application Delivery Controllers (ADCs) Market Overview by Product Type

- German Application Delivery Controllers (ADCs) Market Overview by Company Type

- German Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- THE UNITED KINGDOM

- United Kingdom Application Delivery Controllers (ADCs) Market Overview by Product Type

- United Kingdom Application Delivery Controllers (ADCs) Market Overview by Company Type

- United Kingdom Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- FRANCE

- French Application Delivery Controllers (ADCs) Market Overview by Product Type

- French Application Delivery Controllers (ADCs) Market Overview by Company Type

- French Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- ITALY

- Italian Application Delivery Controllers (ADCs) Market Overview by Product Type

- Italian Application Delivery Controllers (ADCs) Market Overview by Company Type

- Italian Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- THE NETHERLANDS

- Dutch Application Delivery Controllers (ADCs) Market Overview by Product Type

- Dutch Application Delivery Controllers (ADCs) Market Overview by Company Type

- Dutch Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- SPAIN

- Spanish Application Delivery Controllers (ADCs) Market Overview by Product Type

- Spanish Application Delivery Controllers (ADCs) Market Overview by Company Type

- Spanish Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- RUSSIA

- Russian Application Delivery Controllers (ADCs) Market Overview by Product Type

- Russian Application Delivery Controllers (ADCs) Market Overview by Company Type

- Russian Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- SWITZERLAND

- Swiss Application Delivery Controllers (ADCs) Market Overview by Product Type

- Swiss Application Delivery Controllers (ADCs) Market Overview by Company Type

- Swiss Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- REST OF EUROPE

- Rest of Europe Application Delivery Controllers (ADCs) Market Overview by Product Type

- Rest of Europe Application Delivery Controllers (ADCs) Market Overview by Company Type

- Rest of Europe Application Delivery Controllers (ADCs) Market Overview by Industry Sector

8. ASIA-PACIFIC

- Asia-Pacific Application Delivery Controllers (ADCs) Market Overview by Geographic Region

- Asia-Pacific Application Delivery Controllers (ADCs) Market Overview by Product Type

- Asia-Pacific Application Delivery Controllers (ADCs) Market Overview by Company Type

- Asia-Pacific Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- Country-wise Analysis of Asia-Pacific Application Delivery Controllers (ADCs) Market

- CHINA

- Chinese Application Delivery Controllers (ADCs) Market Overview by Product Type

- Chinese Application Delivery Controllers (ADCs) Market Overview by Company Type

- Chinese Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- JAPAN

- Japanese Application Delivery Controllers (ADCs) Market Overview by Product Type

- Japanese Application Delivery Controllers (ADCs) Market Overview by Company Type

- Japanese Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- INDIA

- Indian Application Delivery Controllers (ADCs) Market Overview by Product Type

- Indian Application Delivery Controllers (ADCs) Market Overview by Company Type

- Indian Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- AUSTRALIA

- Australia Application Delivery Controllers (ADCs) Market Overview by Product Type

- Australia Application Delivery Controllers (ADCs) Market Overview by Company Type

- Australia Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- SINGAPORE

- Singaporean Application Delivery Controllers (ADCs) Market Overview by Product Type

- Singaporean Application Delivery Controllers (ADCs) Market Overview by Company Type

- Singaporean Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- SOUTH KOREA

- South Korean Application Delivery Controllers (ADCs) Market Overview by Product Type

- South Korean Application Delivery Controllers (ADCs) Market Overview by Company Type

- South Korean Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- REST OF ASIA-PACIFIC

- Rest of Asia-Pacific Application Delivery Controllers (ADCs) Market Overview by Product Type

- Rest of Asia-Pacific Application Delivery Controllers (ADCs) Market Overview by Company Type

- Rest of Asia-Pacific Application Delivery Controllers (ADCs) Market Overview by Industry Sector

9. SOUTH AMERICA

- South American Application Delivery Controllers (ADCs) Market Overview by Geographic Region

- South American Application Delivery Controllers (ADCs) Market Overview by Product Type

- South American Application Delivery Controllers (ADCs) Market Overview by Company Type

- South American Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- Country-wise Analysis of South American Application Delivery Controllers (ADCs) Market

- BRAZIL

- Brazilian Application Delivery Controllers (ADCs) Market Overview by Product Type

- Brazilian Application Delivery Controllers (ADCs) Market Overview by Company Type

- Brazilian Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- ARGENTINA

- Argentine Application Delivery Controllers (ADCs) Market Overview by Product Type

- Argentine Application Delivery Controllers (ADCs) Market Overview by Company Type

- Argentine Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- COLOMBIA

- Colombian Application Delivery Controllers (ADCs) Market Overview by Product Type

- Colombian Application Delivery Controllers (ADCs) Market Overview by Company Type

- Colombian Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- CHILE

- Chilean Application Delivery Controllers (ADCs) Market Overview by Product Type

- Chilean Application Delivery Controllers (ADCs) Market Overview by Company Type

- Chilean Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- PERU

- Peruvian Application Delivery Controllers (ADCs) Market Overview by Product Type

- Peruvian Application Delivery Controllers (ADCs) Market Overview by Company Type

- Peruvian Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- REST OF SOUTH AMERICA

- Rest of South America Application Delivery Controllers (ADCs) Market Overview by Product Type

- Rest of South America Application Delivery Controllers (ADCs) Market Overview by Company Type

- Rest of South America Application Delivery Controllers (ADCs) Market Overview by Industry Sector

10. MIDDLE EAST & AFRICA

- Middle East & Africa Application Delivery Controllers (ADCs) Market Overview by Geographic Region

- Middle East & Africa Application Delivery Controllers (ADCs) Market Overview by Product Type

- Middle East & Africa Application Delivery Controllers (ADCs) Market Overview by Company Type

- Middle East & Africa Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- Country-wise Analysis of Middle East & Africa Application Delivery Controllers (ADCs) Market

- THE UNITED ARAB EMIRATES

- United Arab Emirates Application Delivery Controllers (ADCs) Market Overview by Product Type

- United Arab Emirates Application Delivery Controllers (ADCs) Market Overview by Company Type

- United Arab Emirates Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- SOUTH AFRICA

- South African Application Delivery Controllers (ADCs) Market Overview by Product Type

- South African Application Delivery Controllers (ADCs) Market Overview by Company Type

- South African Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- EGYPT

- Egyptian Application Delivery Controllers (ADCs) Market Overview by Product Type

- Egyptian Application Delivery Controllers (ADCs) Market Overview by Company Type

- Egyptian Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- SAUDI ARABIA

- Saudi Arabian Application Delivery Controllers (ADCs) Market Overview by Product Type

- Saudi Arabian Application Delivery Controllers (ADCs) Market Overview by Company Type

- Saudi Arabian Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- MOROCCO

- Moroccan Application Delivery Controllers (ADCs) Market Overview by Product Type

- Moroccan Application Delivery Controllers (ADCs) Market Overview by Company Type

- Moroccan Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- KUWAIT

- Kuwaiti Application Delivery Controllers (ADCs) Market Overview by Product Type

- Kuwaiti Application Delivery Controllers (ADCs) Market Overview by Company Type

- Kuwaiti Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- QATAR

- Qatari Application Delivery Controllers (ADCs) Market Overview by Product Type

- Qatari Application Delivery Controllers (ADCs) Market Overview by Company Type

- Qatari Application Delivery Controllers (ADCs) Market Overview by Industry Sector

- REST OF MIDDLE EAST & AFRICA

- Rest of Middle East & Africa Application Delivery Controllers (ADCs) Market Overview by Product Type

- Rest of Middle East & Africa Application Delivery Controllers (ADCs) Market Overview by Company Type

- Rest of Middle East & Africa Application Delivery Controllers (ADCs) Market Overview by Industry Sector

PART C: ANNEXURE

- RESEARCH METHODOLOGY

- FEEDBACK

A10 Networks

Akamai Technologies Inc.

Array Networks

Barracuda Networks

Broadcom Communication

Cisco Systems

Citrix Systems

Cloudflare

Dell Technologies

EdgeNEXUS (JetNEXUS)

Evanssion

F5 Networks

Fortinet

HAProxy Technologies LLC

Juniper Networks Inc.

Kemp Technologies

Loadbalancer.org Inc.

NFWare

Piolink Inc.

Radware

Riverbed

Sangfor Technologies Inc.

Snapt

Total Uptime

ZEVENET

Related Reports

| Report | Published | Price |

|---|---|---|

| Content Delivery Network (CDN) - A Global Market Overview | Sep 24, 2025 | $5490 |

| Global AI Consulting and Support Services Market - Service Types, Company Types and Industry Sectors | Sep 23, 2025 | $5490 |

| Application Life-Cycle Management (ALM) Software - A Global Market Overview | Sep 23, 2025 | $5490 |

| Managed Storage Services - A Global Market Overview | Aug 21, 2025 | $5490 |